Your Complete Guide to Life Insurance for Over 50s UK

Start saving money on Life insurance today

Reaching your 50s is a significant milestone. It's often a time for reflection, for planning the next chapter, and for making sure the people you care about will be financially secure, no matter what. Taking out life insurance for over 50s in the UK is a practical and powerful way to achieve that peace of mind. It provides a financial safety net for everything from funeral costs to clearing debts or simply leaving a legacy for your family.

Why Consider Life Insurance After 50?

For many people, the years after 50 are about cementing their financial security and ensuring their loved ones have a cushion. A life insurance policy pays out a tax-free lump sum to your beneficiaries when you pass away, giving them crucial support at a difficult time.

This isn't just a niche concern; it's a growing priority for people across the country. The over-50s life insurance market has seen significant growth, with flexible policies now making up over 63% of all offerings as insurers regulated by the Financial Conduct Authority (FCA) adapt to consumer needs.

What Can a Life Insurance Payout Be Used For?

A life insurance payout provides your family with options and financial breathing space. The money is theirs to use as they see fit, but common uses in the UK include:

- Covering Funeral Costs: The average funeral in the UK can be a significant and unexpected expense for a grieving family.

- Clearing Outstanding Debts: The policy can wipe out a remaining mortgage, credit card balances, or other loans, lifting a huge financial weight.

- Leaving a Financial Gift: It’s a way to leave a meaningful inheritance for children or grandchildren, perhaps to help with a house deposit, university fees, or other life goals.

- Replacing Lost Income: If your partner relies on your income or pension, a payout can provide the financial stability they need.

At its core, life insurance is about providing peace of mind. It’s a promise to your family that you’ve put plans in place to protect them financially, ensuring your legacy is one of security, not worry.

To get a clearer idea of the costs and cover you could get, it's worth using an over 50 life insurance calculator to see what fits your budget and goals.

Exploring Your Life Insurance Options Over 50

Understanding the different types of life insurance can feel overwhelming, but it's really about finding the right policy for your goals. By your 50s, your financial priorities may have shifted. Perhaps you want to clear the last of the mortgage, cover funeral costs, or leave a financial gift for your grandchildren. Whatever your aim, there’s a policy designed to help.

Let’s break down the three main choices for life insurance for over 50s UK residents, explaining how each one works in plain English.

Term Life Insurance: Protection for a Fixed Period

Term Life Insurance provides a financial safety net for a specific amount of time. You choose the amount of cover (the sum assured) and how long you need it for (the term) – for example, for the next 20 years until your mortgage is paid off. If you were to pass away within that period, your family receives a tax-free lump sum.

If you outlive the term, the policy expires and there’s no payout. Because it only covers you for a defined period, it's often the most affordable way to secure a large amount of cover. This makes it ideal for protecting against specific debts like a mortgage.

- Who is it for? Homeowners with an outstanding mortgage, parents with financially dependent children, or anyone needing a large amount of cover for a fixed number of years.

- Example: A 55-year-old with ten years left on their mortgage could take out a 10-year term policy. This would ensure their partner wouldn't have to worry about the repayments if they were to pass away before the mortgage is cleared.

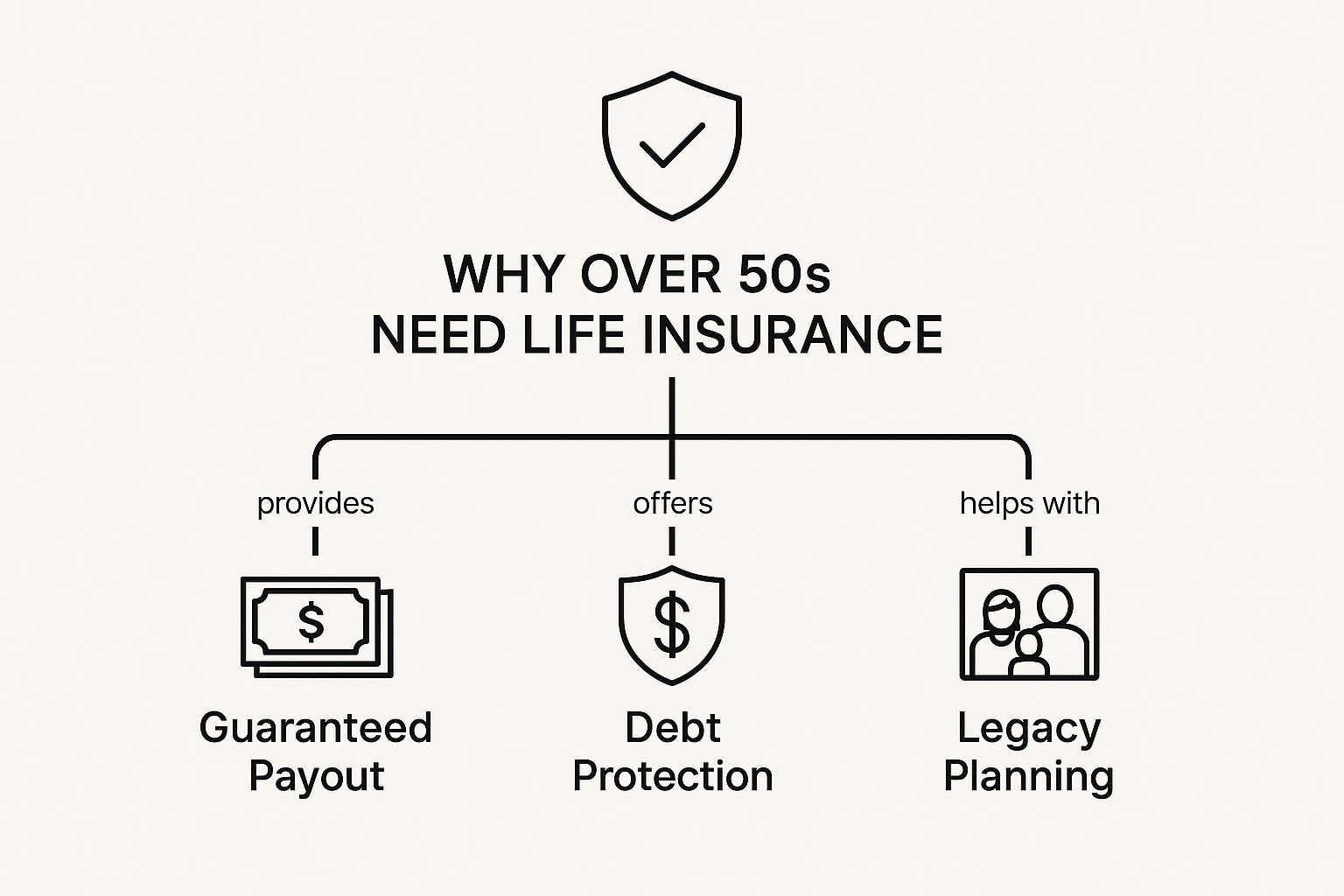

This infographic highlights the primary reasons people over 50 choose to arrange life insurance.

As you can see, the core motivations are providing a guaranteed payout for loved ones, protecting them from debt, and leaving a financial legacy.

Whole of Life Insurance: Lifelong Protection

As the name suggests, Whole of Life Insurance covers you for your entire life. As long as you keep up with the premiums, the policy is guaranteed to pay out a lump sum when you pass away, whenever that may be.

This type of cover is often used for estate planning, such as helping beneficiaries cover a potential Inheritance Tax bill, or for leaving a definite financial legacy. Because the payout is guaranteed, the premiums are typically higher than for term insurance.

Whole of Life policies act as a permanent financial promise to your loved ones. Unlike term cover, there’s no "if" – the payout is a certainty, providing solid peace of mind.

You will almost always have to answer health and lifestyle questions for these policies, as the insurer is taking on a risk that lasts a lifetime. The level of cover can be substantial, making it a powerful tool for legacy planning.

Guaranteed Over 50s Plans: Simple and Accessible

A Guaranteed Over 50s Plan is a specific type of whole of life policy designed for UK residents aged between 50 and 80 (sometimes up to 85). Its main benefit is guaranteed acceptance. You will not be asked any medical questions or need a health check to be approved.

This makes it an excellent option if you have pre-existing health conditions that might make it difficult or expensive to get other types of cover. The trade-off for this guaranteed acceptance is that the payout is usually smaller, typically up to around £20,000. It's primarily designed to cover funeral expenses or leave a small cash gift.

A key feature is the waiting period, usually the first 12 or 24 months. If you pass away from natural causes during this time, the insurer will typically refund the premiums you've paid instead of the full cash sum. However, accidental death is usually covered in full from day one.

Comparing Policy Types for Over 50s

Choosing the right policy depends on your personal circumstances, your budget, and what you want the money to achieve for your family. This table compares the key differences to help you decide.

| Feature | Term Life Insurance | Whole of Life Insurance | Over-50s Guaranteed Plan |

|---|---|---|---|

| Coverage Period | A fixed term (e.g., 10, 20 years). | Your entire life. | Your entire life. |

| Guaranteed Payout? | Only if death occurs within the policy term. | Yes, a payout is guaranteed. | Yes, a payout is guaranteed (after the initial waiting period). |

| Medical Questions? | Yes, full health and lifestyle questions are asked. | Yes, full health and lifestyle questions are asked. | No, acceptance is guaranteed for eligible ages. |

| Level of Cover | Usually provides the highest amount of cover for your money. | Can provide a very high level of cover. | Smaller sums, typically for funeral costs and small gifts. |

| Best For | Covering large, specific debts like a mortgage. | Inheritance Tax planning and leaving a definite legacy. | Covering final expenses, especially for those with health issues. |

By comparing these features, you can identify which policy type best aligns with your family's needs.

How Guaranteed Over 50s Plans Work

Guaranteed Over 50s plans are a straightforward, no-fuss type of life cover designed to be as accessible as possible. Their purpose is simple: to provide a fixed, guaranteed payout to cover funeral costs or leave a final gift.

Their standout feature is guaranteed acceptance. If you're a UK resident between 50 and 85, you are eligible. There are no medical questions to answer, no nurse visits, and no need to provide your health records. This is a game-changer for anyone who has been declined for traditional life insurance in the past due to their health history.

Understanding the Key Features

The appeal of these plans lies in their simplicity. They are not overly complicated and have a clear purpose.

Here’s a breakdown of what you get:

- A Fixed Payout: The amount of cover (the 'sum assured') is agreed from the start. You know exactly what will be paid out, making it easy to plan for specific expenses.

- Fixed Premiums: Your monthly payments are fixed for life and will never increase, allowing you to budget with certainty.

- Lifelong Cover: As long as you maintain payments, you’re covered for the rest of your life. The policy pays out regardless of when you pass away.

Because there is no medical underwriting, the amount of cover is generally smaller than with a fully underwritten policy. The payout is designed to cover final expenses, pay off small debts, or leave a modest inheritance.

The Waiting Period Explained

It's crucial to understand the waiting period (also known as a moratorium period).

The waiting period is usually the first 12 to 24 months of the policy. If you die from natural causes during this initial period, the insurer will not pay the full cash sum. Instead, they will refund all the premiums you’ve paid.

It’s important to note, however, that if death is accidental during this period, most plans will pay out the full sum assured from day one. Once the waiting period is over, you have full cover for death by any cause, for life. This is a standard feature that protects the insurer, given that they haven't asked for any health details.

Payouts and Premiums in Practice

Let’s talk about the numbers. What kind of cover can you get for your money? Well-known UK providers in this market, like SunLife and Royal London, typically offer maximum payouts in the range of £10,000 to £20,000.

For example, a 60-year-old non-smoker paying around £20 a month could secure a payout of between £4,500 and £5,200. A common feature of these plans is that you often stop paying premiums at age 90 or 95, but your cover continues for the rest of your life. You can learn more about how different providers structure their over 50s plans to compare what might work for you.

Ultimately, these plans offer a reliable solution for those who prioritise guaranteed acceptance. They have their own rules and limitations, but as long as you understand them, they can be an incredibly useful financial tool.

What Determines Your Life Insurance Premiums?

Ever wondered why life insurance quotes vary so much? Insurers use a detailed risk assessment process called underwriting to calculate your monthly premiums. For policies like term or whole of life insurance, this involves asking questions about your health and lifestyle. Guaranteed acceptance over 50s plans skip this step, which is why they are priced and structured differently. Understanding these factors is key for anyone considering their options.

Your Age and Health Profile

Age is one of the most significant factors. Statistically, the older you are when you apply, the higher the risk for the insurer, which usually means higher premiums. A 55-year-old will almost certainly pay less for the same amount of cover than a 65-year-old.

Your overall health also plays a massive part. Insurers will want a clear picture of your medical history, any long-term conditions, your height and weight (BMI), and any serious hereditary conditions in your family.

Think of it like this: an insurer is building a picture of your long-term health. A clean bill of health indicates a lower risk, which usually means more affordable premiums. Conversely, existing health issues can increase the cost.

Having a medical condition doesn't automatically prevent you from getting cover. Many people secure affordable policies despite their health history, but it is vital to be completely honest during the application. You can learn more about how different medical conditions affect life insurance applications in our detailed guide.

Lifestyle Choices Matter

Your day-to-day lifestyle choices have a direct impact on your premiums, as they are strong indicators of future health risks. The biggest factor is your smoking status.

- Smoking or Vaping: If you've used any nicotine products in the last 12 months, you will be classed as a smoker. Premiums for smokers can be up to double what a non-smoker would pay.

- Alcohol Consumption: You will be asked about your weekly alcohol consumption. Moderate drinking is generally not an issue, but heavy consumption can lead to higher premiums or even an application being declined.

- Occupation and Hobbies: A high-risk job (like working at heights) or dangerous hobbies (such as mountaineering) may lead to adjusted premiums to reflect the increased risk.

The Policy Details You Choose

Finally, the specifics of the policy you build will shape the final cost. These are the elements you can control and adjust to fit your budget.

- Amount of Cover (Sum Assured): This is the size of the payout your loved ones will receive. A policy for £250,000 will naturally cost more per month than one for £50,000.

- Policy Length (Term): For term life insurance, a longer policy term costs more. A 25-year term presents more risk to the insurer than a 10-year term.

- Type of Cover: Level term insurance, where the payout amount stays the same, costs more than decreasing term cover. Decreasing cover is often used for repayment mortgages, as the payout reduces over time in line with the outstanding loan.

By understanding how your personal profile and policy choices fit together, you will have a much clearer idea of what your premiums will likely be.

Making Your Application Process Simple

Applying for life insurance shouldn't feel complicated. The process is surprisingly straightforward when taken one step at a time. Let's walk through what to expect, from gathering your information to submitting the application.

The journey starts by defining your goals. Are you trying to clear the mortgage for your partner, cover funeral costs, or leave a nest egg? Knowing your 'why' makes working out how much cover you need much easier.

Step 1: Get Your Information Ready

Before filling in forms or speaking with an adviser, it’s a good idea to have some key information ready. This will make the process smoother and faster.

You will generally need:

- Personal Details: Your full name, date of birth, and address.

- Lifestyle Information: Honest answers about your smoking status, alcohol consumption, and any high-risk hobbies.

- Medical History: A summary of your general health, any existing conditions, your height, weight, and your GP’s details.

- Policy Details: How much cover you would like and for how long (for a term policy).

Having this ready allows you to get accurate quotes without guesswork.

Step 2: Honesty is the Best Policy

This is the most critical part of any life insurance application. You must be upfront and truthful about your health and lifestyle. Withholding details can lead to serious problems later.

Insurers use this information to assess risk and set your premiums. If they later discover that important information was omitted—a practice known as non-disclosure—they have the right to cancel the policy and refuse to pay a claim. This would leave your family without the financial protection you intended.

The Financial Conduct Authority (FCA) requires UK insurers to treat customers fairly, and this is a two-way street. It's your responsibility to answer every question honestly. This ensures your policy is built on a solid foundation of trust.

Being honest protects both you and the insurer. It guarantees that the cover you pay for will be there for your family when they need it most.

Step 3: Compare Quotes and Apply

Once you have your information, it's time to compare your options. You could approach insurers individually, but this can be time-consuming. Using a broker, like Discount Life Cover, simplifies the process.

We can compare quotes from a panel of the UK's leading providers, saving you the effort. A good adviser will also explain different policy features and ensure you’re applying for the right type of cover for your situation.

The application is usually completed online or over the phone. For most people seeking life insurance, the journey from getting a quote to being fully covered is quicker and easier than they imagine.

Key Considerations for Your Over 50s Policy

Choosing the right policy is a fantastic first step, but the finer details can make a huge difference to its effectiveness. Getting these small things right ensures your policy works exactly as you intend.

This is especially true when you're looking for life insurance for over 50s in the UK. A little planning now can save your family a lot of hassle later.

The Power of Writing Your Policy in Trust

One of the most valuable tools is writing your life insurance ‘in trust’. While it might sound technical, the concept is simple and incredibly powerful.

When you place a policy in trust, you legally separate it from your estate. This means that when you pass away, the payout goes directly to your chosen beneficiaries. It does not get caught up in the lengthy legal process of probate, which can take months.

By writing your policy in trust, you ensure the money gets to your family quickly. Crucially, it also means the payout is typically shielded from Inheritance Tax, preserving the full value of the lump sum for your loved ones.

Most UK insurers provide the necessary forms to set this up for free when you take out your policy. For a more detailed walkthrough, you can explore our guide on putting life insurance in trust.

Potential Drawbacks of Guaranteed Plans

Guaranteed over 50s plans are excellent for their accessibility, but it's important to be aware of one potential catch. Because the payout is fixed and you may pay premiums for life (or until age 90), there's a chance you could pay more in premiums than the policy will eventually pay out.

This usually only happens if you live a very long life. For many, it's a trade-off they are happy to make for the certainty of getting cover without medical questions. A recent report highlighted this dilemma; while 78% of adults over 50 were concerned about policy costs, 62% still valued the peace of mind from easy acceptance. You can discover more insights from this 2025 market report to get a better feel for consumer trends.

Should You Add Critical Illness Cover?

Another decision is whether to add critical illness cover to your life insurance policy. This optional extra pays out a tax-free lump sum if you're diagnosed with a specified serious illness like a heart attack, stroke, or certain types of cancer.

Here’s a look at the pros and cons:

- Pros: The payout provides a vital financial cushion during recovery. It could cover lost income, pay for private medical treatment, or fund home modifications. It protects your financial stability during your lifetime.

- Cons: Adding this cover will increase your monthly premium. The list of conditions covered is specific and varies between insurers, so it's essential to read the policy details carefully.

Your Over 50s Cover Questions Answered

To help you feel more confident, we’ve answered some of the most common questions about life insurance for over 50s in the UK.

Isn't life insurance too expensive after 50?

Not necessarily. While premiums increase with age, there are still many affordable options. Guaranteed Over 50s Plans, for example, are designed for smaller budgets, with premiums often starting from just a few pounds a month. For a larger sum assured from a term or whole of life policy, the key is to compare quotes. Shopping around can reveal significant price differences between insurers.

Can I get cover if I have health problems?

Yes, absolutely. If you have pre-existing medical conditions, a Guaranteed Acceptance Over 50s Plan is an excellent choice. There are no medical questions or checks. As long as you are a UK resident in the eligible age bracket (usually 50-85), you are guaranteed to be accepted. For traditional policies like term or whole of life, you must disclose your conditions. This might mean your premium is higher, but cover is often still available, particularly with specialist insurers.

Having a health condition shouldn't stop you from getting peace of mind. The most important thing is to explore all your options and be completely honest on your application.

What is an insurance waiting period?

A waiting period (or moratorium) is a standard feature on most Guaranteed Over 50s Plans. It's an initial period, typically lasting for the first 12 or 24 months of the policy. If you were to pass away from natural causes during that time, the insurer would refund all the premiums you've paid rather than paying the full sum assured. Claims for accidental death are usually covered in full from day one. Once the waiting period ends, you are fully covered for death by any cause.

Why should I put my policy in trust?

Placing your policy in a trust is a simple legal step that separates the payout from your estate. This offers two significant advantages:

- Speed: The money can be paid directly to your beneficiaries, bypassing the often lengthy probate process, so they get the funds much faster.

- Tax Efficiency: As the payout isn't usually considered part of your estate, it is generally not subject to Inheritance Tax, ensuring your family receives the full amount.

Most insurers provide the forms to do this for free when you take out the policy.

Ready to secure your family's financial future? At Discount Life Cover, we make it simple to compare quotes from top UK insurers, helping you find the right cover at the right price. Get your free, no-obligation quote today and take the first step towards complete peace of mind.

Get a Free Life Insurance Quote Now

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.