As a firefighter, you spend your career protecting others, walking into dangers most people run from. It's a selfless job, and that commitment means thinking about firefighter life insurance isn't just another box to tick. It’s a crucial piece of financial protection for your family, making sure they’re looked after, no matter what happens on a shout.

Why Specialist Life Insurance is a Must

Your role is unique, and your life insurance needs to reflect that. There's a common myth that having a high-risk job automatically means you'll face complicated and expensive cover, but that’s not always the reality. In fact, many UK firefighters can get life insurance on standard terms.

Insurers know your profession comes with risks. But they look at the whole picture, not just your job title. They’ll consider your specific duties, your overall health, your lifestyle, and even your hobbies. You might be surprised to learn that premium increases based solely on being a firefighter are less common than you'd think; the focus is on you as an individual.

Looking Beyond Your Employer's Benefits

Most firefighters get a 'death in service' benefit through their employment package. It's a great perk, usually paying out a lump sum of two to four times your annual salary if you pass away while employed. So, on a £35,000 salary, that could be a payout of around £105,000.

While that sounds like a lot of money, it often doesn't stretch as far as a family truly needs. Just think about the big financial responsibilities it would have to cover:

- The mortgage: Clearing the family home is usually the top priority.

- Daily living costs: Covering bills, food, and transport for years to come.

- Future education: Funding for your children's school fees or university.

- Outstanding debts: Paying off any loans, credit cards, or car finance.

A personal life insurance policy acts as a vital extra layer of security that your death in service benefit simply can't match. It’s your own portable safety net that stays with you, even if you decide to leave the fire service.

This is something we see across all emergency services, as we've covered in our guide to life insurance for police officers. A personal policy means the cover amount is built around your family’s specific long-term needs, giving you genuine peace of mind that goes way beyond a standard workplace benefit.

To help you get started, we've summarised the main points you'll need to think about.

Key Considerations for Firefighter Life Insurance

| Consideration | Why It Matters for Firefighters |

|---|---|

| Death in Service vs. Personal Policy | Your employer's benefit is a great start, but a personal policy offers tailored, portable cover that isn't tied to your job. |

| Your Specific Role | Insurers will want to know about your duties. A frontline firefighter may be viewed differently from one in a training or administrative role. |

| Health and Lifestyle | Your fitness, smoking status, and hobbies all play a big part in determining your premiums, often more so than your job itself. |

| Critical Illness Cover | This can be added to your policy to provide a payout if you're diagnosed with a serious illness, offering a financial buffer during recovery. |

| Waiver of Premium | Consider this add-on. If you're unable to work due to illness or injury, it covers your premiums so your policy doesn't lapse when you need it most. |

Ultimately, getting the right firefighter life insurance is about building a solid financial shield that protects your loved ones' future, whatever your career path holds.

How UK Insurers Assess Your Profession

When you for firefighter life insurance, the provider will start a process called underwriting. It's not as intimidating as it sounds. In plain language, it’s how an insurer reviews your application to understand the level of risk involved.

Essentially, they're building your personal ‘risk profile’. This profile isn’t just about your job title, though. Insurers regulated by the Financial Conduct Authority (FCA) take a much broader view, piecing together several key factors to work out your eligibility and what your monthly premium will be.

What Underwriters Look For

The assessment goes a lot deeper than a simple yes or no. Insurers really dig into the specifics of your life and career to get the full picture.

Here are the key areas they’ll focus on:

- Your Specific Duties: Are you on the front line as an operational firefighter, or is your role more focused on training, admin, or fire safety inspections? Any specialist duties, like rope rescue or responding to hazardous material incidents, will also be factored in.

- Your Health and Medical History: This is a standard part of any life insurance application and includes your current health, any pre-existing conditions, your height, and your weight.

- Lifestyle Choices: Things like whether you smoke or vape, how much you drink, and your general fitness level all play a role in the assessment.

- High-Risk Hobbies: What you get up to outside of work matters, too. If you’re into hobbies like rock climbing, scuba diving, or private piloting, insurers will need to account for that.

Knowing what they look for is a big help because these are the very things that directly influence the final offer you get. You can get more information in our detailed guide on how high-risk life insurance is assessed for different jobs and hobbies.

Understanding Premium Loading

Based on your risk profile, an insurer might what’s known as a ‘premium loading’. It's just industry-speak for a calculated increase on the standard premium price. It’s not a penalty; it's simply the insurer adjusting the cost to reflect a higher-than-average level of risk.

For a firefighter, a premium loading is the insurer's way of acknowledging the hazards that come with the territory. It ensures your policy is priced correctly, which means your cover is solid and will actually pay out when it’s needed most.

The UK's operational fire service is made up of around 35,000 dedicated professionals. To put the risks into perspective, in the year ending March 2023, there were 2,223 non-fatal casualties among firefighters in England alone. Statistics like these are why some insurers might add a risk adjustment.

Why Honesty Is Non-Negotiable

Being completely straight with the insurer during your application is absolutely crucial. It can be tempting to downplay certain duties or perhaps a lifestyle habit to try and get a lower premium, but this can backfire spectacularly.

If an insurer finds out that information was left out—a practice called non-disclosure—they have every right to invalidate your policy. That could mean your loved ones get nothing, which defeats the entire purpose of having life insurance in the first place. By giving a full and honest account of your job and lifestyle, you make sure the policy you get is a reliable promise to protect your family's future.

Choosing the Right Life Insurance Policy

Trying to get your head around life insurance can feel like a minefield, but understanding the main types of policy is the first big step. For UK firefighters, the choice usually boils down to three core options. Each one is built for different financial needs and stages of life.

It's not about finding the "best" one, but about finding the one that fits your family's situation like a glove.

Think of it like picking the right tool for a job on the station – you wouldn't grab a Halligan tool to fix the kettle. In the same way, the right life insurance policy depends entirely on what you need it to do for your family if you're not around. Let's break down the main contenders.

Level Term Insurance: A Consistent Safety Net

Level Term insurance is probably the most straightforward type of cover you can get. You pick a cash lump sum (the 'sum assured') and how long you want the cover for (the 'term'). If you pass away during that term, your family gets that exact amount. The key thing here is that the payout does not change.

- Who it’s for: This is often an excellent fit for firefighters with younger families. That competitive payout can be a lifeline, replacing your lost income, covering day-to-day bills, and making sure big future costs like university fees are sorted.

- Real-world example: Imagine a 35-year-old firefighter with two small children and a partner. They take out a £250,000 level term policy for 25 years. It doesn't matter if they pass away in year three or year 23 – their family receives the full £250,000. It's solid, consistent protection until the children can stand on their own two feet.

With level term cover, you get predictable, stable protection. Your monthly premium and the final payout are fixed from day one, which makes it easy to budget for and dead simple for your loved ones to understand.

Decreasing Term Insurance: The Mortgage Protector

Decreasing Term insurance works a bit differently. The payout amount actually shrinks over the life of the policy. It's designed to fall in line with a large repayment debt, like a mortgage. Because the insurer's risk gets smaller over time, your premiums are usually than a level term policy.

- Who it’s for: This is the perfect partner for a repayment mortgage. As you chip away at your home loan, the amount you owe goes down, and so does your life insurance cover. It’s all about making sure your family isn't left struggling with a massive mortgage bill.

- Real-world example: A firefighter buys a new house with a £300,000 mortgage over 30 years. They take out a decreasing term policy to match. After 15 years, their outstanding mortgage might be down to £150,000, and the policy's potential payout will have dropped to a similar amount.

Whole of Life Insurance: A Lifelong Guarantee

Unlike term policies that run out after a set period, a Whole of Life policy covers you for your whole life. It guarantees a payout whenever you pass away, as long as you've kept up with the payments. These policies are generally more expensive than term cover.

- Who it’s for: This is often the choice for firefighters who want to leave a competitive inheritance, ensure funeral costs are covered without fuss, or help their family deal with a potential inheritance tax bill. It's less about covering short-term debts and more about leaving a lasting legacy.

- Real-world example: A firefighter in their late 50s has paid off the mortgage and their children are financially independent. They take out a £50,000 whole of life policy. This lump sum ensures their family has immediate cash to handle funeral expenses and other final costs, without having to raid their own savings at a difficult time.

At the end of the day, choosing the right firefighter life insurance is all about matching the product to your family’s specific needs. Once you get these key differences, you can pick the cover that gives you genuine peace of mind.

Adding Critical Illness and Income Protection

Thinking about financial protection often goes straight to the worst-case scenario. But for a job as physically demanding as firefighting, what happens if you're hit with a serious illness or injury? What if you can't work?

That's where a couple of powerful add-ons to your life insurance come into their own, creating a much stronger financial safety net for you and your family.

Life insurance pays out when you pass away, but these policies are all about supporting you during your lifetime. They tackle that nagging question: what happens to the bills if I can't earn my living? Let's break them down.

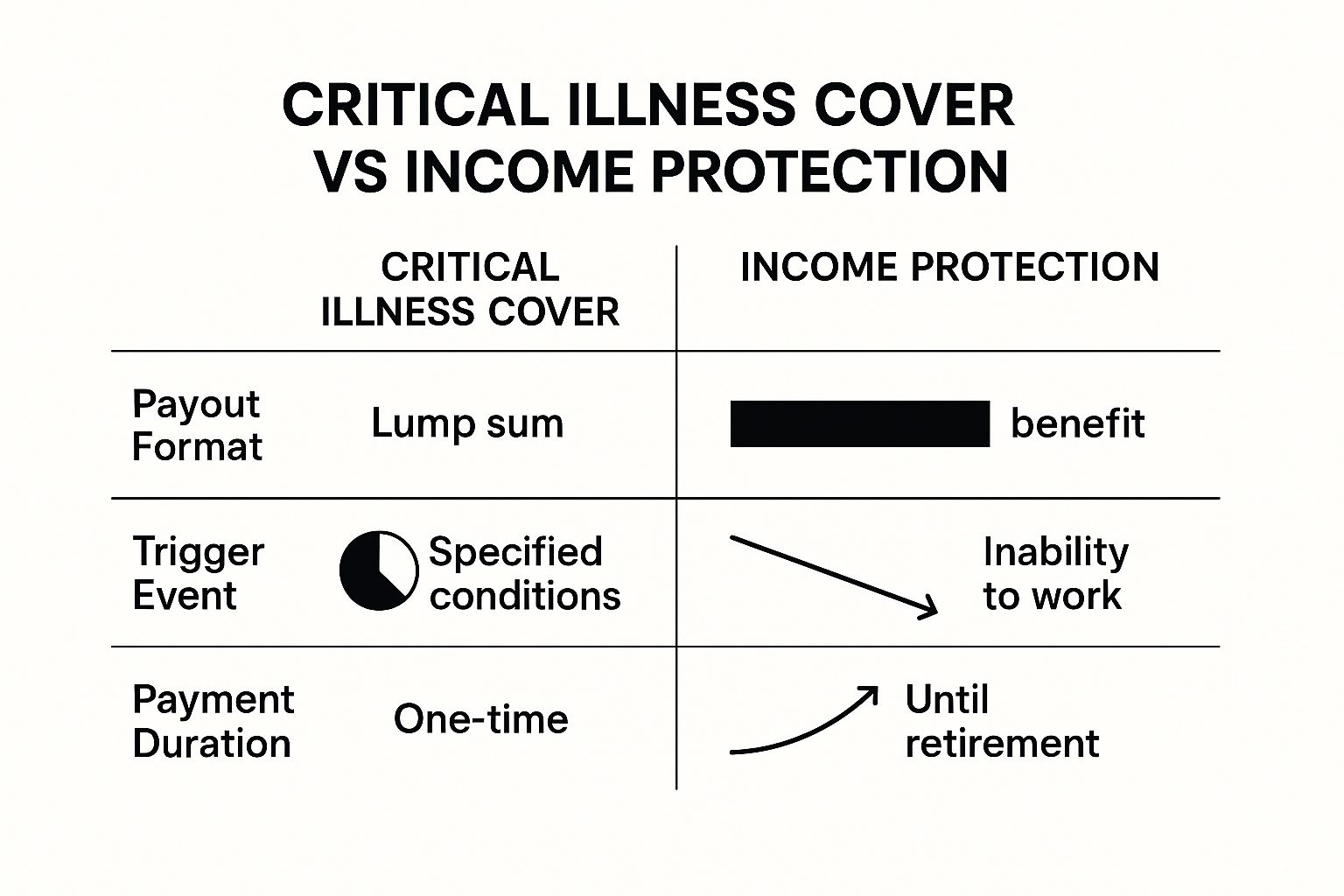

Critical Illness Cover Explained

Critical Illness Cover is a policy add-on that pays you a tax-free lump sum if you're diagnosed with a serious medical condition that's listed on your policy. Every insurer has its own list, but you'll almost always find major events like heart attacks, strokes, and certain types of cancer covered.

Think of it as an emergency fund that drops into your bank account exactly when you need it most. It gives you the space to breathe and focus purely on getting better, without the added stress of money worries.

This cash is yours to use as you wish. It could clear the mortgage, pay for private medical care, adapt your home if needed, or simply keep the household running while you’re out of action.

For firefighters, where peak physical fitness is non-negotiable, a serious diagnosis can be career-ending. This payout acts as a vital financial bridge, giving you choices and stability when you're going through a tough time. You can learn more in our detailed guide on what is critical illness insurance and the types of conditions it covers.

Income Protection: The Salary Replacement

While Critical Illness Cover is a one-off payment, Income Protection is a different type of policy altogether. It acts like a replacement salary, paying you a regular monthly benefit if you're unable to work because of an illness or injury.

This monthly payment keeps coming in until you're fit to return to work, or until your policy ends (usually when you plan to retire), whichever happens first. It's designed specifically to cover your regular outgoings – the mortgage or rent, bills, and the weekly food shop.

Imagine picking up an injury that stops you from passing your fitness test. You could be looking at a long spell off work. Income Protection ensures your household doesn't grind to a halt, stopping a health problem from becoming a full-blown financial crisis. It protects what is arguably your most important asset: your ability to earn a living.

Comparing Your Options

So, which one is right for you? Do you need both? The answer really comes down to your own situation. They offer different kinds of protection, and knowing the difference is the key to building a plan that truly has your back.

To make things clearer, let's look at how they stack up side-by-side.

Comparing Life Insurance Add-Ons for Firefighters

Here's a simple comparison to help you see the key differences at a glance:

| Feature | Critical Illness Cover | Income Protection |

|---|---|---|

| How It Pays Out | A single, tax-free lump sum payment. | A regular, tax-free monthly income. |

| What Triggers a Payout | Diagnosis of a specific, serious condition listed in the policy. | Being unable to work due to almost any illness or injury. |

| Purpose of the Money | Provides a large cash injection for major costs or to clear debts. | Replaces lost earnings to cover ongoing monthly expenses. |

Ultimately, whether you choose one or both, they offer incredible peace of mind. They make sure that if your health takes a hit, your financial wellbeing—and that of your family—doesn't have to follow suit.

How to Apply and Secure the Best Premiums

Navigating the application process is your chance to take control and lock in the best possible rates. It’s less complicated than you might think, but taking a methodical approach and being completely upfront will pave the way for affordable, solid cover that genuinely protects your family.

First things first, you'll need to get all your personal information together. Insurers need a clear picture of your health, your lifestyle, and the specifics of your role in the fire service. This isn't just about your job title; it's about the reality of what you do day-to-day.

The Importance of Full Disclosure

When you're ing, honesty isn't just the best policy – it's the only policy. It might be tempting to downplay certain parts of your job, perhaps thinking it’ll get you a lower premium, but that's a risky game to play. Insurers need to know everything to assess the risk fairly.

Be ready to share details on any specialist duties you have, such as:

- Hazardous Materials Response (HAZMAT): Dealing with chemical spills and incidents.

- Rope or Water Rescue: Specialist technical rescue operations.

- Urban Search and Rescue (USAR): Working in and around collapsed structures.

Holding back this kind of information could be seen as non-disclosure. If that happens, it could invalidate your policy, meaning a claim could be denied right when your family needs it most. A trustworthy policy is built on transparency from the very beginning.

Strengthening Your Application

While you can't change the risks that come with the job, you have a surprising amount of control over other factors that influence your premiums. Insurers look at the whole picture, and if you can show you're a low-risk individual outside of work, it can really help balance out the occupational risk.

An insurer's decision is based on a holistic view of your life. By demonstrating you are a low-risk applicant outside of your profession, you can directly and positively impact the cost of your premiums.

To put your best foot forward, focus on these key areas:

- Maintain a Healthy Lifestyle: Your Body Mass Index (BMI), blood pressure, and cholesterol levels all matter. The fact that regular fitness is a core part of your job is a massive plus point in your favour.

- Be a Non-Smoker: This is one of the single biggest things you can do to lower your premiums. If you smoke or vape, quitting can slash your costs, often after just 12 months of being nicotine-free.

- Review Your Hobbies: If you're into high-risk pastimes like scuba diving or rock climbing, be honest about them. Yes, they can affect your premiums, but transparency is always the right call.

Work with a Specialist Adviser

Finally, the single most effective way to secure the best firefighter life insurance terms is to work with a specialist broker. It’s a different world from going directly to an insurer or using a standard comparison website. A specialist lives and breathes the high-risk occupation market.

They know which insurers, like Legal & General or Aviva, are more understanding when it comes to underwriting for emergency service personnel. An adviser does the legwork for you, saving you time and almost certainly money by connecting you with providers who are far more likely to offer you standard terms. They champion your application, making sure it’s presented in the right way to the right people, which often leads to much better premiums than you could ever find on your own.

Frequently Asked Questions (FAQ)

Let's cut through the jargon and tackle some of the most common questions UK firefighters have when they start looking into life insurance.

Will my policy pay out for a death in the line of duty?

Yes, in almost every single case. When you take out a policy, the insurer is fully aware of your profession. The risks that come with firefighting are already factored into your premium right from the start. A standard UK policy is designed to pay out regardless of the cause of death, including an incident on duty. It's extremely rare for policies to have job-related exclusions, but it's always wise to check the policy documents or ask an adviser to confirm.

Is firefighter life insurance more expensive?

It can be, but it’s not a given. While firefighting is classed as a high-risk occupation, many insurers will offer standard rates, especially if you're in good health. Some providers might add a 'premium loading' (a small increase) to account for the extra risk. Ultimately, the price comes down to the insurer, your age, your health, whether you smoke, and the amount of cover you need. Using a specialist broker is the best way to find insurers who are most favourable to firefighters.

Do I need to declare my specific duties?

Yes, you absolutely must. Being upfront and honest during the application process is non-negotiable. You need to be clear about your specific role and what it involves. Be sure to mention any specialist activities, such as responding to hazardous material (HAZMAT) incidents, carrying out technical water or rope rescues, or working with an urban search and rescue team. If you hold back information, it could give the insurer a reason to refuse a claim down the line.

I have death in service cover, do I still need a personal policy?

It is strongly recommended. Your death in service benefit is a great perk, but it typically only pays out a lump sum of around 2-4 times your annual salary. For most families, that's not enough to pay off the mortgage and cover long-term living costs. Furthermore, that cover is tied to your job. If you leave the fire service, that protection disappears. A personal life insurance policy belongs to you, providing a level of cover you've chosen to meet your family's specific needs, no matter where you work.

Ready to secure your family's future? The team at Discount Life Cover is here to help you find the right protection at the right price. Get a free, no-obligation quote today and compare your options from leading UK insurers.

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply