As a police officer, you put yourself on the line every day to protect the public. But have you ever stopped to think about how secure your own family's financial future really is? This guide will break down police officer life insurance in simple, clear terms, showing you exactly how a personal policy can give your family the rock-solid protection they deserve.

Why Police Officers Need a Watertight Financial Plan

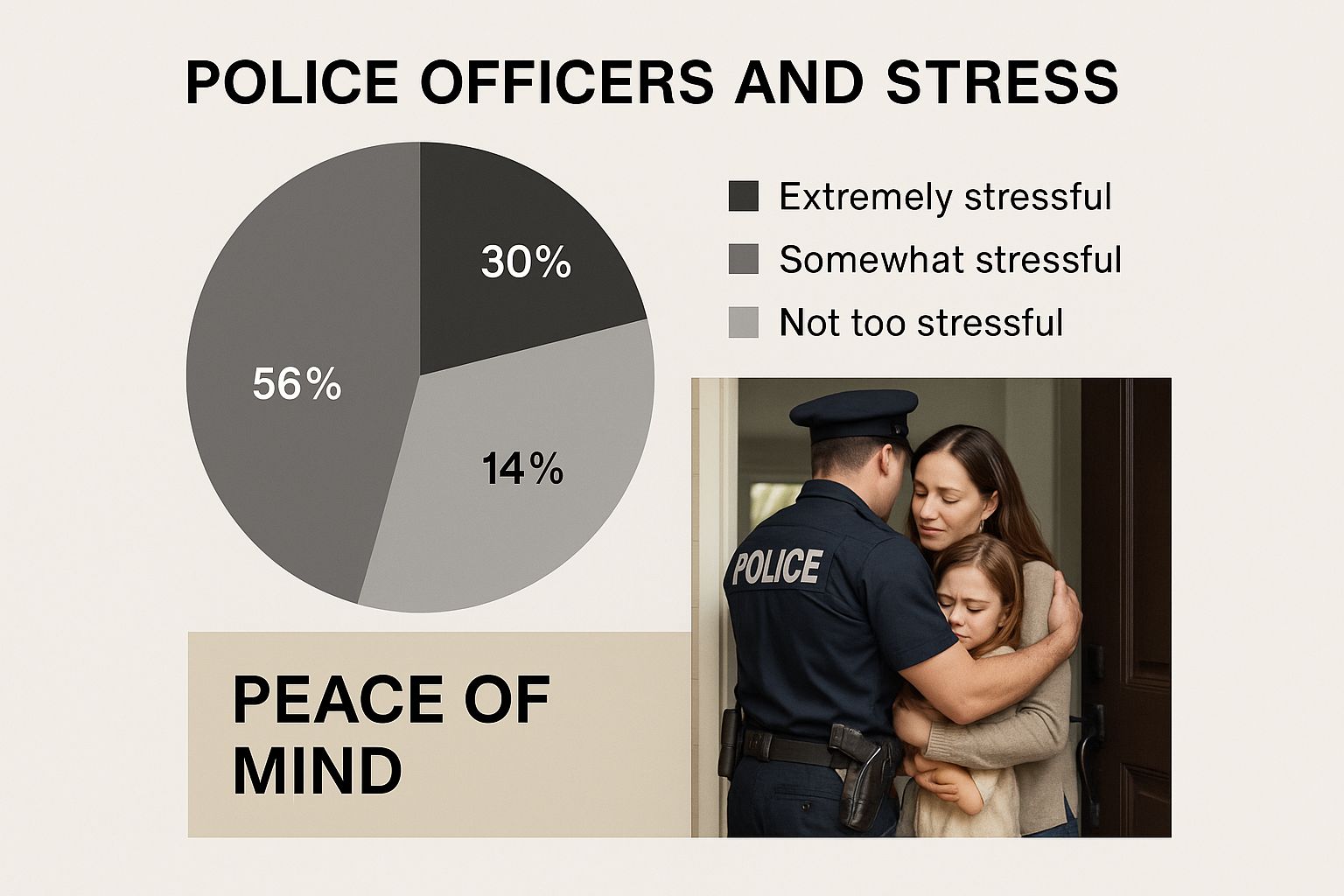

Serving in the police force is more than a job; it's a commitment to public safety, often in unpredictable and dangerous situations. While your focus is rightly on protecting others, it’s absolutely vital to make sure your own loved ones are financially shielded if the worst should happen. A personal life insurance policy is the cornerstone of that protection.

Many officers assume their 'death in service' benefit from the force is enough. While it's a valuable perk, the truth is it often falls short of what a family genuinely needs to maintain their standard of living for the long haul.

Building a Financial Safety Net

A private life insurance policy pays out a tax-free lump sum to your family, which can be a lifeline for covering essential costs. Think of it as a financial backstop that steps in to support your family when you no longer can. This payout can help them:

- Clear the mortgage: For most, the number one priority is making sure the family can stay in their home without the stress of monthly mortgage payments.

- Cover ongoing living expenses: From utility bills and council tax to the weekly food shop and transport, the costs of daily life add up fast.

- Fund future goals: The money can be put towards big life events, like your children's university education or even their future weddings.

- Settle final expenses: This includes funeral costs, which can be a significant and immediate financial burden nobody wants to worry about at a difficult time.

A truly watertight financial plan starts with getting your objectives down on paper. Learning more about setting clear financial goals is a great first step in building a solid foundation for your family's future.

Gaining Control and Peace of Mind

Here’s the thing about a death in service benefit: it’s tied to your job. A personal policy, on the other hand, is yours to keep, even if you leave the force. You're in complete control of the cover amount and how long the policy runs, making sure it lines up perfectly with your family's unique needs.

For a deeper dive into what a policy can do for you, you can explore the main benefits of life insurance in our detailed guide. Ultimately, this level of control provides genuine peace of mind, knowing your family's financial security is firmly in your hands.

Looking Beyond Your Death in Service Benefit

Many officers think the benefits package from the force is a complete financial safety net. A big part of that is the ‘death in service’ benefit, which pays out a lump sum if you pass away while still serving. And while it’s a great perk to have, relying on it as your only plan can be a massive gamble for your family's future.

Typically, a death in service payout is a multiple of your annual salary – usually between two and four times your pay. That might sound like a lot of money, but when you start chipping away at the big financial commitments, it can vanish surprisingly quickly.

Understanding the Limitations

Let's paint a picture. Say you have a young family, a £250,000 mortgage, and you’re earning £45,000 a year. A death in service benefit of three times your salary gives your family a £135,000 payout. That wouldn't even clear the mortgage, let alone cover day-to-day living costs or future expenses like sending the kids to university. This single example throws the limitations of employer-provided cover into sharp relief:

- It's tied to your job: The moment you leave the police, whether for a new career or retirement, this benefit is gone. Vanished. This could leave you uninsured just when getting a new policy might be more expensive due to age or health.

- You have no control: The payout amount is set in stone by your employer. It’s not designed around your family’s actual needs. You can’t increase it if you take out a bigger mortgage or have another child.

- It may not be enough: As we saw, the lump sum often just isn't big enough to cover a family's long-term needs, from paying off debts to replacing years of your lost income.

With around 160,000 officers serving across the UK, a huge number of people are relying on these standard benefits. But because they lack flexibility and personal control, a personal police officer life insurance policy becomes absolutely essential for creating real financial security.

Think of your death in service benefit as the foundation. It’s a solid start, but you need to build the rest of the house yourself to properly protect your family.

Securing a Policy That Works for You

A personal life insurance policy puts you firmly in control. You get to choose the exact amount of cover your family would need to be financially comfortable. You also decide how long the policy should last, making sure it aligns perfectly with your mortgage term or runs until your children are old enough to stand on their own two feet.

Even better, a personal policy opens up more ways to protect your family. For instance, you can place your policy into a trust. To get your head around this, have a read of our in-depth guide on putting life insurance in trust. In short, it helps ensure the payout gets to your loved ones quickly and can keep it outside your estate, which is a big help when it comes to inheritance tax. This is the kind of customisation that makes a personal policy a cornerstone of smart financial planning.

Decoding Your Life Insurance Options

Trying to get your head around life insurance can sometimes feel like you're reading a dense legal document. There are so many different terms and options flying about, it's easy to feel a bit lost. Let's cut through the noise and break down the most common policies for UK police officers into plain, simple English.

You'll mainly come across two types of cover: Level Term and Decreasing Term insurance. The best way to think of them is as two different tools designed for specific jobs. Picking the right one simply comes down to what you want to protect and how you need that protection to work for your family over the years.

Level Term Insurance: A Fixed Safety Net

Level Term insurance is probably the most straightforward type of cover going. You pick a cash lump sum and a set period (the 'term'), and if you were to pass away during that time, your family receives that exact amount. The payout never changes, and your monthly premiums are usually fixed right from the start.

Think of it as a constant, reliable safety net for your family. If you take out £300,000 of cover for 25 years, that net stays £300,000 strong whether a claim is needed in the first year or the 24th. This makes it a brilliant choice for things like:

- Covering an interest-only mortgage: The loan amount stays the same, so your cover should, too.

- Providing for your children: It guarantees a specific pot of money is there for their upbringing and future.

- Replacing your income: It gives your partner a predictable lump sum to handle day-to-day living costs without your salary.

Decreasing Term Insurance: A Shield for Your Mortgage

Decreasing Term insurance works a bit differently. With this policy, the total payout amount gets smaller over the term. It's cleverly designed to track the outstanding balance of a repayment mortgage. As you chip away at your home loan each year, the amount of cover needed to clear it also drops.

Because the potential payout goes down over time, the premiums for this type of cover are usually than for Level Term. It acts like a protective shield that shrinks as the debt it's covering gets smaller. This makes it the most cost-effective way to protect a repayment mortgage, making sure your family can stay in their home without that massive financial weight. If you're weighing up the two, our guide on whether you should choose level term or decreasing term life insurance is a great next step.

Comparing Key Life Insurance Policies for Police Officers

To make things clearer, let’s put the two main policy types side-by-side. This table breaks down the key differences to help you see which one aligns best with your family's needs and financial goals.

| Feature | Level Term Insurance | Decreasing Term Insurance |

|---|---|---|

| Payout Amount | Stays the same throughout the policy term. | Reduces over the policy term. |

| Primary Use | Providing a fixed lump sum for any need. | Clearing a repayment mortgage or other shrinking debt. |

| Premiums | Generally higher as the risk to the insurer is constant. | Typically lower as the potential payout decreases. |

| Best For | Interest-only mortgages, income replacement, family protection. | Cost-effectively covering a repayment mortgage. |

Ultimately, the choice depends on what you're trying to protect. Level term offers a solid, predictable foundation for your family's future, while decreasing term is the smart, budget-friendly choice for ensuring your mortgage is paid off.

Bolstering Your Cover with Add-Ons

On top of these core policies, you can always add extra layers of protection. One of the most important ones to consider is Critical Illness Cover. This is a powerful add-on that pays out a tax-free lump sum if you're diagnosed with a specific serious illness listed in the policy, like certain types of cancer, a heart attack, or a stroke. For a police officer, this can be a financial lifeline if an illness forces you out of the job you love.

How Insurers View Risk in the Police Force

It’s a common worry for police officers: will my job automatically mean sky-high life insurance premiums? It’s a perfectly logical question, given the risks you face daily. The good news is that insurers take a much more detailed and individual approach than you might think. They don’t just see the words ‘police officer’ and stamp ‘high risk’ on your application.

Instead, the people who assess your application, known as underwriters, want to get a picture of what your day-to-day role actually involves. This whole process, called underwriting, is about figuring out the precise level of risk tied to your specific duties. It means an officer working a desk job in administration will be seen very differently from a member of a specialist firearms unit.

Your Role Defines Your Risk

Insurers know the police force is incredibly diverse. There are hundreds of different roles, and each one carries its own level of risk. While the public perception of policing is often focused on the high-risk end of the scale, the reality is that most officers in the UK hold positions that insurers classify as standard or lower risk. Because of this, premiums for police officer life insurance can often be very similar to those for people in non-hazardous jobs. You can find more details on how insurers assess occupational risk at sports-fs.co.uk.

To get an accurate picture, an insurer will ask you some pretty specific questions about what you do. This is your chance to give them the full story, making sure you aren’t unfairly penalised for a risk you don’t actually face.

They’ll want to know about things like:

- Your primary duties: Are you mostly on patrol, stuck behind a desk, or part of a specialist team?

- Use of equipment: Do you routinely carry a firearm or a Taser?

- Specialist roles: Are you involved in advanced driving, public order duties, or maybe even covert operations?

- Overseas deployment: Have you served abroad in high-risk locations, or is that a possibility in your role?

By gathering all this information, they build a profile based on your real life, not on some generic stereotype of policing.

What Insurers Consider Higher Risk

Now, while many roles will sail through and qualify for standard rates, some duties will naturally attract a bit more attention from underwriters. This doesn't automatically mean you’ll be turned down for cover, but it might lead to a higher premium or certain exclusions being added to your policy.

Factors that usually lead to a closer look include:

- Regular involvement with firearms or explosives disposal.

- Working within specialist units like counter-terrorism or armed response.

- Duties that involve working at extreme heights or in confined spaces.

- Frequent high-speed driving or being involved in pursuits.

The key takeaway here is simple: honesty and detail are your best friends when you . Giving a clear, accurate description of what you do helps the insurer make a fair assessment, which often leads to more affordable premiums than you might have expected.

It’s so important to be completely transparent. If you hold back information about high-risk duties, you could put a future claim at risk. That would defeat the whole purpose of getting the policy in the first place. A fair evaluation is always based on the reality of your individual role, and that’s what gets you the right protection at the right price.

Your Step-by-Step Guide to Getting Covered

Sorting out life insurance can feel like a mountain to climb, but if you break it down into smaller, manageable steps, it’s actually pretty straightforward. This guide is all about walking you through the process, from working out your family’s needs right through to getting your application submitted with confidence.

The idea is to strip away the jargon and complexity, giving you the power to secure the protection your family deserves without all the usual headaches. Let's get stuck in.

Step 1: Work Out How Much Cover You Need

Before you even think about looking at quotes, your first job is to figure out how much cover your family would realistically need if you weren't around. This isn't a finger-in-the-air guess; it’s a proper look at your finances to make sure the payout would be enough to keep things ticking over.

A good place to start is by adding up all your major financial responsibilities. A simple way to remember this is the D.E.B.T. method:

- Debts – Add up your mortgage, any car loans, outstanding credit card balances, and other personal loans you might have.

- Education – Think about the future costs for your kids' schooling. This could be anything from private school fees to university tuition.

- Bills – How much would your family need to cover daily living costs like groceries, utilities, and running the car? A common rule of thumb is to aim for a pot of money that could replace your annual salary for at least 10 years.

- Terminal expenses – Don't overlook funeral costs. They can be a significant and immediate expense that your family would have to find.

Tallying this all up gives you a solid, personalised figure to aim for when you start looking at policies.

Step 2: Prepare Your Information

Once you've got your target cover amount, it's time to gather all the details insurers will want to see. Having this ready beforehand makes the whole application process much quicker and smoother. Insurers need a clear picture of your health, your lifestyle, and the specifics of your duties on the force.

Being completely honest isn't just good practice—it's a legal requirement. Under FCA regulations, you have a duty of fair presentation to provide accurate information. Holding back key details could invalidate a future claim, which defeats the whole point of having cover in the first place.

You'll be asked about your medical history, any pre-existing conditions, your height and weight, and whether you smoke or drink. When it comes to your job, be prepared to clearly explain your day-to-day tasks, whether you're part of a specialist unit, and any high-risk duties you perform.

Step 3: Compare Quotes and Apply

With all your information ready, it’s time to hunt down the right policy. Rather than going to individual insurers one by one, using a specialist broker like Discount Life Cover lets you compare quotes from a range of providers all at once. It saves a load of time and helps you find the most competitive price for your situation.

An experienced adviser can also steer you through the application, making sure you present everything clearly. They know how different insurers view the risks tied to policing and can match you with the provider best suited to your role. Following these steps will give you peace of mind that you're getting the best possible police officer life insurance for your family's future.

FAQs: Your Common Questions Answered

Even when you've got a good grasp of the options, it's completely normal to have a few last-minute questions before you jump in. We get it. Here are some of the most common queries we hear from officers, answered simply and directly to help you move forward with confidence.

Will a firearms role make my insurance unaffordable?

Not necessarily, no. While it’s true that being a firearms officer is seen as a higher-risk duty by insurers, it doesn't automatically mean you’ll be priced out of a policy. Far from it.

Many UK insurers actually specialise in covering police and emergency services staff, so they know exactly how to assess your role fairly. The final premium will come down to the nitty-gritty of your duties, how often you're in high-risk situations, your training, and of course, personal details like your age and health. The cost is often far more reasonable than most officers expect. The only real way to know for sure is to get a personalised quote.

Do I need to tell my insurer if my duties change?

This is a great question. Generally, the answer is no. Once your policy is up and running, the terms are locked in based on the information you gave at the start. You're not typically required to ring up your insurer every time your role or duties change.

However, there's a catch. If you decide to for a new policy or you want to increase the amount of cover you already have, you'll need to declare your current duties honestly and accurately. This ensures the new or adjusted terms are valid. When in doubt, always have a quick look at your policy documents for the specific conditions.

Is Critical Illness Cover available to police officers?

Yes, absolutely. Critical Illness Cover is widely available and a highly recommended add-on for police officers. It’s designed to pay out a tax-free lump sum if you're diagnosed with a serious medical condition specified in the policy.

Given the physical and mental toll the job can take, this cover provides a vital financial safety net if a serious illness means you can't work. The cost and availability will differ from one insurer to the next and will depend on your health, age, and lifestyle.

What happens to my policy if I leave the force?

This is one of the single biggest advantages of having your own personal life insurance policy. Your death in service benefit is tied to your job – when you leave, it's gone. A personal policy, on the other hand, is completely portable.

It belongs to you, not your employer. As long as you keep paying the premiums, your cover stays active, protecting your family no matter where your career takes you next.

It's also a good idea to know the ins and outs of your policy to make sure the claims process is as smooth as possible for your loved ones if they ever need it. To be fully prepared, it’s worth looking into the common reasons insurance claims are refused and what your options are if that happens. A little bit of knowledge here can go a long way in making sure the protection you've set up does its job.

Finding the right police officer life insurance is all about securing peace of mind. At Discount Life Cover, our expert advisers are here to help you compare quotes from the UK's leading insurers, making sure you find the best protection for your family at a competitive price.

Get Your Free, No-Obligation Quote Today

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply