Working offshore is a brilliant way to provide for your family, but it comes with a unique set of risks. The problem is, most standard life insurance policies just aren't built for the job. That's where a specialist offshore worker life insurance policy comes in. It’s designed specifically to fill those gaps, giving you a proper financial safety net that understands the realities of your profession. It’s about making sure your loved ones are protected, no matter what.

Why Your Job Requires Specialist Life Insurance

Life on a rig or support vessel in the North Sea is a world away from a typical nine-to-five. The financial rewards are great, but the risks you face every day are just as significant. Standard life insurance policies, the kind designed for office jobs, are often riddled with clauses that could reduce or even completely void a claim if an accident or illness is linked to a hazardous job like yours.

Think about an engineer from Aberdeen who spends weeks at a time on a platform. He's got a mortgage and two children at school. A standard policy might have exclusions for things like helicopter travel or incidents involving high-pressure equipment. This could leave his family without financial support at the worst possible moment.

Protecting Against Occupational Risks

Specialist cover is built from the ground up with your job in mind. It starts from the basic truth that your work environment is inherently more dangerous. The insurers who offer these policies, which are regulated by the Financial Conduct Authority (FCA) in the UK, genuinely understand the offshore industry and are equipped to underwrite the risks that come with it.

A policy that's tailored to your job acknowledges the reality of your work, ensuring your family's financial future isn't left to chance. It turns your premium from just another monthly bill into a solid guarantee that the mortgage gets paid and your family can maintain their standard of living.

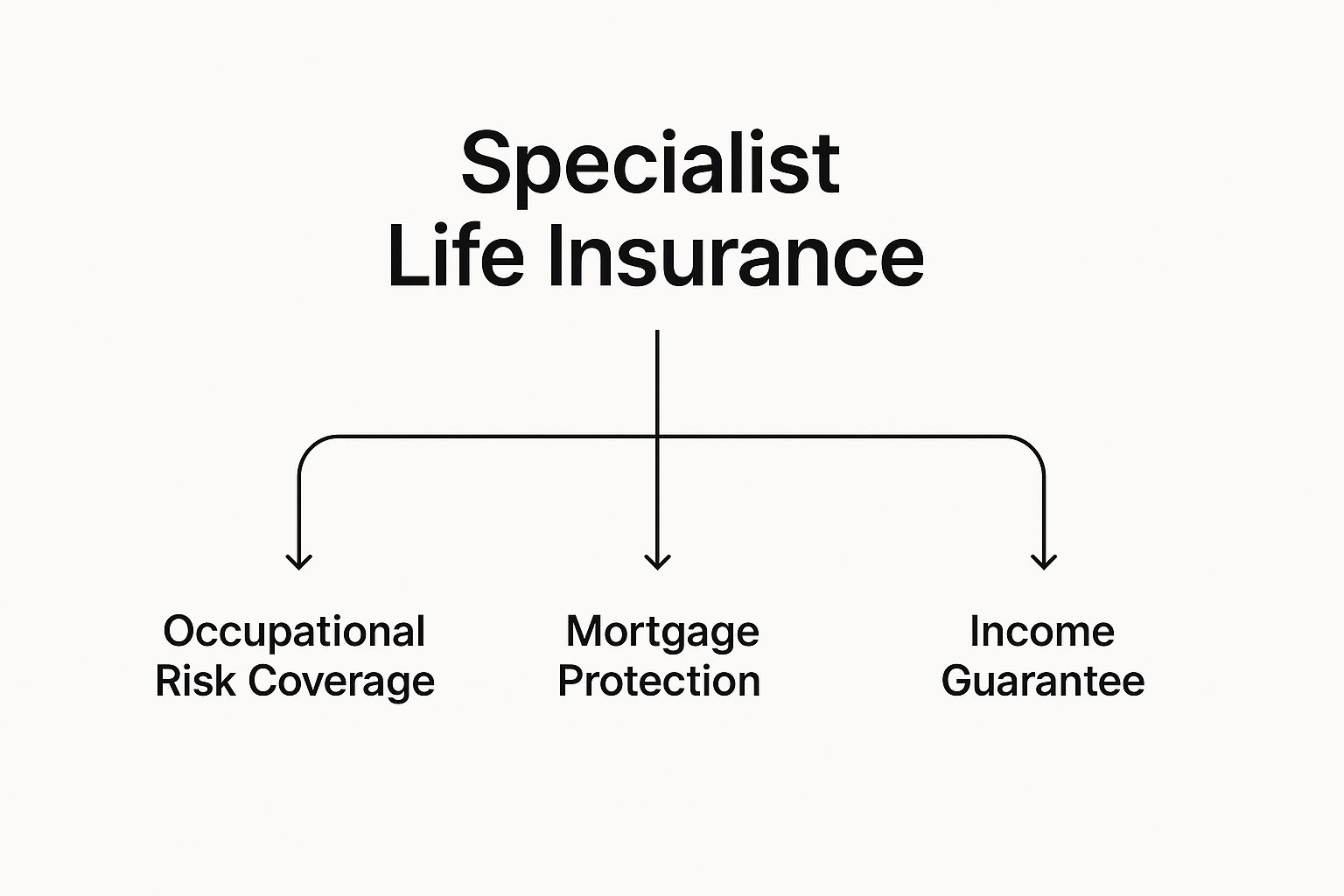

This diagram shows how specialist life insurance acts as a multi-layered financial shield for you and your family.

As you can see, it's all about connecting the cover directly to its core purpose: protecting against job-specific dangers, securing the family home, and replacing your lost income.

The UK's offshore oil and gas industry supports around 280,000 jobs, and workers face everything from the risks of helicopter transit and working at heights to exposure to hazardous materials. Specialist life insurance is specifically designed to pay out a tax-free lump sum to your loved ones if the worst happens.

Given the heightened health risks, from cardiovascular issues to permanent disability, adding critical illness cover is also a very smart move. You can learn more about why insurance is so vital for high-risk professions and how these policies are put together. For anyone working offshore, having the right kind of specialist life insurance isn’t just an option—it's a fundamental part of responsible financial planning.

How Insurers Assess the Risks of Offshore Work

When you fill out a life insurance application and write 'offshore worker' as your job, insurers don't just see a single title. They immediately begin a detailed look into what you really do day-to-day. This isn't about being nosy; it’s simply about pricing the policy fairly based on the real-world risks involved.

This process goes a lot deeper than most people think. An underwriter will break down the hazards of your job into a few key areas to build your personal 'risk profile'. Understanding these categories makes it crystal clear why a standard high-street insurer might decline your application, while a specialist provider knows exactly how to weigh up the different factors.

Environmental and Geographical Dangers

First up, they look at where you're working. The harsh conditions of the North Sea are a world away from the Gulf of Mexico or the waters off West Africa. Insurers will look into:

- Weather Severity: How often do you face extreme weather? Constant high winds and rough seas have a direct knock-on effect on safety.

- Geopolitical Stability: Working in politically unstable parts of the world adds a layer of risk that has nothing to do with your actual job.

- Location: How remote is the rig? The distance from shore directly impacts how quickly emergency medical help can get to you, a massive factor for underwriters.

This geographical breakdown is the foundation of your risk profile. Even with the best safety gear, the environment itself is a constant, unavoidable hazard that has to be factored into the price.

On-the-Job Hazards and Day-to-Day Tasks

Next, the underwriters zoom in on your specific role. An admin staff member who spends most of their time in the living quarters is in a completely different risk bracket to a subsea engineer or a derrickhand.

The insurer's goal is simple: to understand what your daily work actually looks like. They need to know if you're working at height, handling pressurised equipment, diving, or operating heavy machinery. Each activity carries its own, very specific level of risk.

They'll want to know the specifics, such as:

- Your Exact Role: Are you drilling, doing maintenance, working in catering, or in a management position?

- Exposure to Hazardous Materials: Do you handle hazardous chemicals, flammable materials, or work around loud machinery?

- Working at Height or Depth: Any job involving rope access, diving, or regular work up on the derrick is automatically flagged as higher risk.

To give you some context, the UK's Health and Safety Executive (HSE) states that over 20,000 people work in the offshore sector. They're all exposed to both immediate physical dangers and the risk of longer-term health problems. While UK safety laws are strict, the rotational and often contract-based nature of the work means many miss out on solid employee benefits, making personal life cover absolutely vital.

Travel and Transit Risks

Finally, there's a unique risk that standard insurers often worry about: just getting to and from the rig. For most offshore workers, this means regular helicopter flights.

Now, helicopter travel is statistically very safe, but it's still classed as a 'non-standard' form of travel with its own set of risks that need to be underwritten. This is a classic stumbling block. A mainstream insurer might just put an automatic exclusion on your policy for it, whereas a specialist understands that it’s just part of the commute.

Understanding these specific factors is the key to getting the right cover. For anyone in a high-risk job, it pays to know what's going on behind the scenes, and you can learn more in our guide on how high-risk life insurance works. To get a broader view on how risks are managed in the workplace, looking into the world of health and safety consulting services can be insightful.

To pull all this together, here’s a quick look at how an insurer might view common offshore risks.

How UK Insurers View Common Offshore Risks

| Risk Factor | Specific On-the-Job Examples | Impact on Your Insurance Application |

|---|---|---|

| Extreme Weather Exposure | Working on deck in the North Sea during winter storms. | A significant factor. Insurers will want to know how much of your time is spent exposed to the elements. |

| Working at Height | Rope access technicians, derrickhands, maintenance crew on the flare stack. | Considered a high-risk activity. Your premium will likely be higher, and a specialist insurer is essential. |

| Subsea Operations | Commercial divers, ROV pilots, subsea engineers. | A major risk factor. Diving often requires a heavily specialised policy with specific terms. |

| Helicopter Transit | Regular crew changes via helicopter. | A standard part of the job for specialists, but can cause mainstream insurers to add exclusions or decline cover. |

| Hazardous Materials | Handling drilling muds, chemicals, or working near flammable substances. | The specific materials and your level of exposure will be assessed. Could lead to increased premiums. |

| Geopolitical Instability | Working in regions with political unrest or piracy risks. | This is an external risk that underwriters will consider, potentially increasing the cost of your cover. |

Ultimately, the more detail you can provide about your safety training, your specific duties, and the precautions your employer takes, the better. It helps the underwriter build a complete and accurate picture, which almost always works in your favour.

Choosing the Right Type of Cover for Your Needs

Trying to understand life insurance can feel like a mammoth task, especially when you throw a high-risk job into the mix. But really, it all boils down to one simple thing: finding a policy that properly looks after your family and fits your financial situation. For offshore workers, that means getting solid protection without any needless complexity.

The good news is that you have access to the same core types of life insurance as anyone else in the UK. The real difference is in the details – specifically, how insurers view the risks of your job. Let's break down the main options so you can see what might work for you.

Term Life Insurance: A Solid Foundation

Term life insurance is the most common type of cover in the UK. It’s straightforward and does exactly what it says on the tin. You pick a payout amount (the 'sum assured') and how long you want the cover to last (the 'term') – say, £250,000 over 25 years. If you pass away within that timeframe, your family gets a tax-free lump sum. If you outlive the policy, the cover simply stops and no payout is made.

Its simplicity and affordability make it an excellent choice for protecting your family during your main working years. There are two main types you'll come across:

Level Term Insurance: With this policy, the payout amount stays exactly the same from day one to the final day of the policy. If you have £300,000 of cover for 30 years, your family gets £300,000 whether you pass away in year one or year 29. This is perfect for covering an interest-only mortgage or leaving a lump sum to replace your income and help your loved ones with daily living costs.

Decreasing Term Insurance: This type is built specifically to cover a repayment mortgage. The payout amount gradually drops over the years, roughly in line with what you still owe the bank. Because the potential payout for the insurer gets smaller every year, the premiums are usually than for level term cover. It's a very cost-effective way to make sure your family's home is secure.

Critical Illness Cover: An Essential Add-on

Life insurance has your family covered if the worst happens, but what if a serious illness or injury means you can never work offshore again? That's where Critical Illness Cover steps in. Think of it as an optional extra you can add to your life insurance policy.

This cover pays out a tax-free lump sum if you're diagnosed with a serious medical condition defined in the policy, like a heart attack, stroke, or certain types of cancer. For an offshore worker, a diagnosis that ends your career could be a financial catastrophe. This payout is a vital safety net, giving you the breathing room to:

- Pay off the mortgage or other large debts.

- Cover private medical bills or adapt your home.

- Replace your lost income while you focus on recovery.

Given the physical nature of offshore work, adding critical illness cover is a smart move. It builds a much stronger financial wall around you and your family.

Exploring Other Policy Types

While term insurance is the go-to for most, it’s worth knowing what else is available. Whole of Life insurance, for example, does what its name suggests – it covers you for your entire life and guarantees a payout whenever you pass away. Because the payout is certain, the premiums are much higher, and it's typically used for specific purposes like inheritance tax planning.

Insurers look very closely at the specifics of your role – an administrator obviously faces less risk than a rig operator. They'll also consider your work location (UK waters are generally seen as safer) and even how you get to the rig.

While Whole of Life might be too expensive for many, an alternative for older or retired offshore workers is an 'over 50s' plan. These policies guarantee acceptance for UK residents aged 50-85 with no medical or job-related questions asked. The drawback is they usually have a waiting period (typically 12-24 months) before they pay the full amount for death by natural causes. You can dig deeper into these specialist insurance options for offshore workers to see the finer details.

Ultimately, choosing the right type of offshore worker life insurance is all about matching the policy to your family's needs, both for today and for the years to come.

How Your Specific Role Impacts Your Premiums

When you for offshore worker life insurance, insurers want to look beyond your job title. To get the premium right, they need to understand the reality of your day-to-day work. It's a bit like putting a puzzle together, where your specific duties, the environment you work in, and your personal health are all crucial pieces that form your complete risk profile.

This isn’t about penalising you for your profession; it’s about pricing the policy fairly based on the facts. It's perfectly possible for two people with the same "Offshore Technician" title to end up with wildly different premiums, all based on what their jobs actually involve. Let's break down the key things that influence the final price you'll pay.

Your Professional Duties Under the Microscope

The single biggest factor is what you actually do during your rotation. An underwriter’s job is to build a crystal-clear picture of your tasks, responsibilities, and the equipment you handle.

Role and Responsibilities: A project manager who spends 90% of their time in an office environment is a much lower risk than a rope access technician working on the derrick every day. The more hands-on and physically demanding your role, the higher the perceived risk. Your specific profession, such as being one of the many skilled offshore engineers, plays a massive part in this.

Working at Height or Depth: If your job involves working at significant heights (like on a flare stack) or in subsea operations (as a commercial diver, for instance), insurers will automatically flag this as a high-risk activity. These kinds of duties often mean you'll need cover from a specialist insurer who genuinely understands the dangers involved.

Handling Hazardous Materials: Are you regularly exposed to industrial chemicals, drilling fluids, or other hazardous materials? This can also increase your premiums. Insurers will want to know exactly what substances you handle and what safety protocols are in place.

At the end of the day, the more detail you can give about your training and safety record, the better. It helps the insurer make an informed decision based on you, not a vague job description.

Geographical and Travel Factors

Where you work in the world is almost as important as what you do. The location of your rig or vessel has a direct bearing on the risks you're exposed to.

For instance, insurers generally see the UK Continental Shelf (UKCS), which covers most of the North Sea, as a relatively low-risk area. This is thanks to its tough safety regulations and political stability. As a result, many workers based here can get life insurance at standard or near-standard rates.

However, if your work takes you to more volatile regions, such as parts of West Africa or the Middle East, underwriters will have to factor in the increased risks of things like political instability or even piracy. This can lead to higher premiums or specific exclusions in your policy.

Helicopter travel is another classic sticking point. For you, it’s just the daily commute. But for many mainstream insurers, it's a non-standard risk. A specialist provider, on the other hand, understands it's just part of the job, and they'll underwrite your policy accordingly.

Personal Health and Lifestyle Choices

Finally, your personal details play a vital role, just as they would for any other life insurance application. These factors have nothing to do with your job offshore, but they are just as important in setting your final premium.

Age and Health: It's a simple fact that younger applicants in good health will almost always pay less. Any pre-existing medical conditions, like high blood pressure or diabetes, will need to be assessed. Being completely honest here is crucial – it ensures your policy is valid when it's needed most.

Smoker Status: Insurers view smoking as a major health risk. Premiums for smokers can easily be double what non-smokers pay.

Hobbies and Pastimes: Do you spend your time off scuba diving, rock climbing, or mountaineering? If you have any hazardous hobbies, these will also be factored into your overall risk profile.

By understanding how these professional and personal elements all come together, you can get a much clearer picture of what really drives the cost of your offshore worker life insurance policy.

Your Step-by-Step Guide to a Smooth Application

Applying for specialist life insurance like this can feel daunting, but a little bit of preparation makes all the difference. To get the best possible outcome, you need to give the insurer a crystal-clear picture of what you do for a living. This helps them assess the risks fairly and accurately.

Think of it this way: the more organised you are, the smoother the process. Let's walk through the key steps to make sure you have everything ready to go, avoiding delays and helping you secure the right cover at a sensible price.

Gather Your Key Information

Before you start filling out forms, take a bit of time to pull all your details together. Insurers need the specifics to make a decision, and having it all on hand from the start will speed things up massively.

They’ll primarily want to know about three areas of your life:

- Your Job: Don't just put "Offshore Worker." They'll want to know exactly what you do. What are your specific duties? What equipment do you use day-to-day? Crucially, how much time do you spend on riskier tasks, like working at heights or handling hazardous materials?

- Your Health: You’ll face the usual medical questions. This includes any past or present health conditions, your height and weight, and whether you smoke or vape. Be completely open and honest.

- Your Lifestyle: Insurers are also interested in what you do in your spare time. If you have any hobbies that carry a bit of risk, like scuba diving, motorsports, or rock climbing, they’ll want to know about it.

Getting this all down on paper first will set you up for a much easier application.

To make things even simpler, we've put together a checklist of the key information you'll need. Having these details ready will make the whole process faster and more straightforward.

Your Offshore Life Insurance Application Checklist

| Information Needed | Specific Details to Include | Why It Matters to Insurers |

|---|---|---|

| Personal Details | Full name, date of birth, address, contact information. | Standard identity verification to start your policy. |

| Occupational Details | Exact job title, name of employer, typical duties, specific equipment used. | Helps them understand the precise nature of your work beyond a generic title. |

| Work Environment | Location (e.g., North Sea rig), time spent offshore vs. onshore, travel methods (e.g., helicopter). | The environment is a key factor in assessing the level of risk you face daily. |

| High-Risk Activities | Details of any work at height, use of hazardous materials, diving, or operating heavy machinery. | This is the crucial information underwriters use to calculate your specific risk profile. |

| Health & Medical History | Pre-existing conditions, medications, height, weight, smoking/vaping status, alcohol consumption. | Your overall health is a primary factor in determining life insurance premiums. |

| Lifestyle & Hobbies | Participation in any adventurous sports like diving, climbing, motorsports, or private aviation. | Hobbies can sometimes carry risks that need to be factored into your policy. |

| Financial Details | Your annual income and details of any existing life insurance policies. | This helps determine the appropriate level of cover and ensures you aren't over-insured. |

Getting this information together might take a little effort upfront, but it pays off by preventing back-and-forth questions and potential delays down the line.

Why Honesty Is Non-Negotiable

When it comes to any insurance application, being upfront isn't just a good idea—it's essential. It might be tempting to downplay the risky parts of your job to try and get a quote, but that's a gamble you really don't want to take. It can have absolutely devastating consequences.

Under UK law, if an insurer finds out you weren't truthful on your application (a 'non-disclosure'), they have the right to void your policy. That means your family would get nothing, and all the money you paid in premiums would be lost.

Full disclosure means being completely honest about your job, your health, and your lifestyle. It's the only way to guarantee your policy is rock-solid and will actually pay out if your family ever needs to make a claim.

Why You Should Talk to a Specialist Broker

Trying to navigate the world of offshore worker life insurance by yourself can be tough going. Most high-street insurers just don't have the experience to properly understand your role, which often leads to sky-high quotes or even an outright decline.

This is where a specialist broker, like us here at Discount Life Cover, can be a game-changer. A broker who understands the offshore industry knows exactly how to help.

- They know how to frame your application. They understand what underwriters are looking for and can present your case in the most favourable light.

- They have access to the right insurers. They’ve built relationships with providers who actually specialise in high-risk jobs and are far more likely to offer you fair terms.

- They save you time, hassle, and money. By shopping the market for you, they find the best quotes without you having to fill out endless forms for different companies.

Working with an expert takes all the guesswork out of the process and seriously boosts your chances of getting affordable, comprehensive cover. They're in your corner, guiding you every step of the way.

Finding Affordable Cover Without Compromise

If you work offshore, you might assume that getting robust life insurance is going to be expensive. But paying sky-high premiums is far from a given. There's a common myth that all policies for hazardous jobs come with a hefty price tag. The reality? Many workers on the UK Continental Shelf secure comprehensive cover at standard, or very close to standard, rates.

The secret to unlocking affordable protection is knowing that not all insurers see risk in the same light. One provider might take one look at your job title and immediately add a significant premium increase. Another, more specialist insurer, will take the time to really understand your specific duties and the safety protocols you follow, leading to a much fairer price.

The Power of Comparison

This difference between insurers makes shopping around absolutely essential. Going straight to a single provider is a bit of a gamble; you could unknowingly be talking to the one company that’s most cautious about your profession. To find the best value without cutting corners on your cover, you need to compare quotes from a wide range of providers.

This is where working with a specialist really pays off. An expert adviser or broker who gets the offshore industry can connect you with the insurers most likely to offer favourable terms. They know which providers have experience underwriting roles like yours and can present your application in the best possible light. You can learn more about the benefits of using a life insurance broker in our detailed guide.

Finding the right offshore worker life insurance isn’t about just accepting the first quote you get. It’s about strategically navigating the market to find an insurer who properly understands and fairly prices your level of risk.

Ultimately, the best way to find out what your real options are is to see them for yourself. Getting a no-obligation quote is the first step towards securing proper peace of mind for your family.

Ready to see how affordable your cover could be? The team at Discount Life Cover can help you compare quotes from leading UK insurers who specialise in offshore professions.

Frequently Asked Questions

It's only natural to have a few questions when you're sorting out something as important as offshore worker life insurance. To make things a bit easier, we've pulled together the most common queries we get from offshore professionals just like you.

Will My Policy Cover Me if I Work Abroad?

That's a big one, and the honest answer is: it depends entirely on your specific policy. When you're ing for cover, you absolutely have to be upfront about every location you work in or might be sent to in the future.

A policy for someone working in the highly regulated North Sea is going to look very different from one for an engineer on a rig in a more politically volatile region. Some UK insurers might exclude certain high-risk countries, while others will offer global cover but charge a higher premium for it. The golden rule here is total transparency. Tell your insurer or broker everything about your work locations to make sure your cover is solid, wherever the job takes you.

Can I Get Critical Illness Cover as an Offshore Worker?

Yes, absolutely – and for many, it’s a vital piece of the financial puzzle. Given how physically demanding the job can be and the inherent risks involved, adding critical illness cover provides a crucial safety net.

If you were diagnosed with a serious illness specified in the policy and couldn't work anymore, the lump sum payout could be a genuine lifesaver. The application process is very similar to life insurance; they’ll look at your job, your health, and your lifestyle. A specialist broker really proves their worth here, as they know exactly which insurers are best for high-risk jobs and can find you a competitive deal.

Do I Need to Tell My Insurer if My Job Duties Change?

Without a doubt. You must let your provider know about any major changes to your role. Your life insurance policy is a contract based on the facts you gave them at the start. If those facts change significantly, the insurer needs to know.

For instance, if you get a promotion from a desk job to working on the rig, or if you start handling new hazardous materials, that’s a material change that could impact your policy. Keeping quiet about it could, in a worst-case scenario, invalidate your policy entirely. Just give your insurer or broker a call to discuss any changes. It’s a quick conversation that ensures your cover stays valid and fit for purpose.

Is Life Insurance Always Expensive for Offshore Workers?

This is probably the biggest myth out there. While the profession is considered high-risk, that doesn't automatically mean your premiums will break the bank. In reality, many offshore workers, especially those in admin, technical, or catering roles within UK waters, often get life insurance at standard rates or with just a small price increase.

The final cost really comes down to the specifics: what you do, where you do it, your personal health, and your lifestyle. By using a specialist broker who can scan the , you can connect with insurers who will assess your individual risk fairly. More often than not, this leads to premiums that are much more affordable than you might think, putting essential protection well within reach.

Ready to secure that peace of mind for your family? At Discount Life Cover, we help you compare quotes from the UK's top insurers to find the right protection at the competitive. Get your free, no-obligation quote today.

Get a Personalised Quote from Discount Life Cover

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply