As an electrician, your work is physically demanding and carries a unique set of risks every single day. That’s why sorting out electrician life insurance is one of the most practical things you can do for your family. It's about making sure they're financially looked after, no matter what happens. And despite the hazards of the job, getting affordable, solid cover is more straightforward than you might think.

Why Specialist Life Insurance is a Bright Idea for Electricians

Being an electrician isn't a desk job. You're dealing with high-voltage systems, working at height, and sometimes squeezing into tight, confined spaces. The potential for a serious accident is always there. This is exactly why a robust financial safety net isn't just a 'nice-to-have'—it's the cornerstone of responsible planning for you and your loved ones.

Life insurance pays out a tax-free lump sum to your family if you pass away while the policy is active. This cash can be a lifeline, helping your family to:

- Pay off the mortgage: Keeping a roof over their heads without financial strain.

- Cover everyday living costs: Things like bills, food, and childcare don't stop, and this helps replace your income.

- Clear outstanding debts: Wiping the slate clean on personal loans or credit cards.

- Fund their future: Whether it's for the children's university education or other big life goals.

Acknowledging the Risks of Your Trade

Insurers understand that not all jobs are created equal. The very nature of your work as a sparky means you face more risks than someone in an office. It’s a similar story for others in manual trades, and you can get a better feel for how insurers see these jobs in our guide to construction worker life insurance.

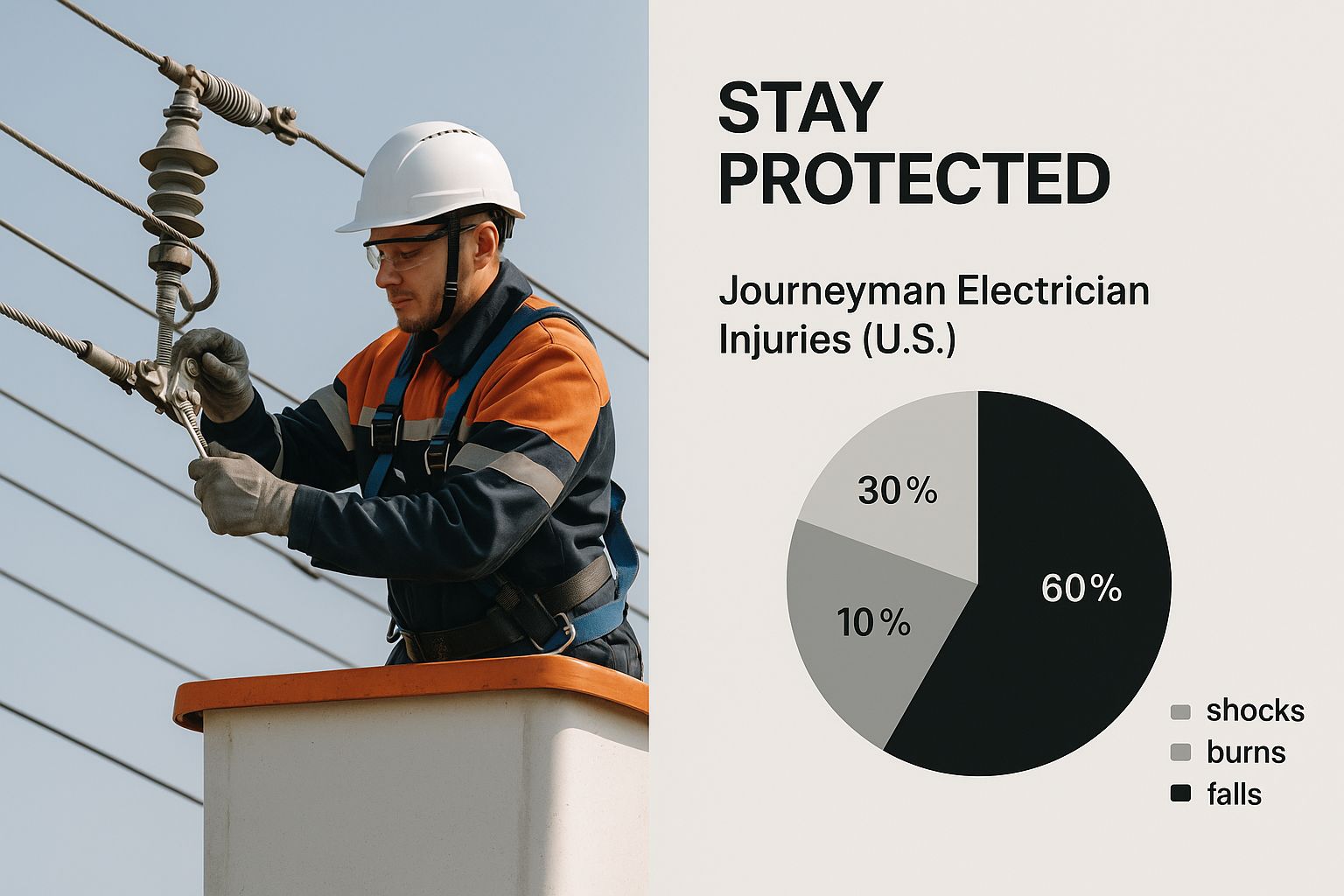

The infographic below drives home why it's so important to have protection when you're in a high-risk trade.

It’s a stark reminder that working with high-voltage equipment, often at height, demands a solid plan B. The risks are real, but the good news is they can be managed with the right financial safeguards in place.

Peace of Mind for You and Your Family

At the end of the day, electrician life insurance is all about buying peace of mind. Knowing your family won't be plunged into financial hardship if the worst should happen lets you focus on your work and enjoy life with confidence. It's a practical tool that protects the future you're working so hard to build. Without it, your family could be left vulnerable, facing an uncertain future during an already devastating time.

How Insurers Assess Risk for Electricians

When you for life insurance, the provider goes through a process called underwriting. Think of it as them building a complete picture of your life to work out how much of a risk you are to insure. This ultimately decides the cost of your policy, which is known as your premium. For electricians, they will look closely at what you do for a living, alongside all the usual personal factors.

What insurers really care about is the nitty-gritty of your day-to-day job. No two electricians have the exact same role, so the risk assessment isn't one-size-fits-all. The final price and even the availability of your policy will depend heavily on your specific working conditions, as well as standard things like your age and health.

The good news? For the majority of sparkies working in typical domestic or commercial settings, electrician life insurance is often available at standard rates. Modern safety protocols mean the job isn't automatically thrown into the high-risk category anymore.

Professional Risk Factors

The first thing any insurer wants to know is what kind of environments you work in. Are you mostly wiring up new builds and kitchens, or does your job take you to more hazardous locations?

Insurers will look carefully at the risk management strategies you and your employer have in place. Taking a look at something like a comprehensive construction risk assessment template gives you a good idea of the kinds of hazards they're thinking about.

They will want answers to questions like:

- Work Environment: Do you work in standard residential homes and commercial offices, or are you on high-risk industrial sites like power stations, offshore rigs, or railways?

- Working at Height: Does your job regularly involve working at significant heights, say on scaffolding, pylons, or transmission towers?

- Voltage Levels: Are you dealing with standard domestic voltages or high-voltage industrial systems?

- Safety Record: Have you had any work-related accidents in the past?

It's straightforward: an electrician with a spotless safety record working on residential projects is going to be seen as a much lower risk than someone who regularly works at height with high-voltage equipment.

How Your Work Environment Impacts Your Life Insurance Premium

To give you a clearer picture, let's break down how different jobs can affect your premium. Insurers group roles into different risk bands, which directly influences the price you'll pay.

| Work Environment | Typical Risk Level (for Insurers) | Potential Premium Impact |

|---|---|---|

| Domestic/Residential Electrician | Standard | Premiums are usually offered at standard rates, with no extra cost. |

| Commercial Electrician (Offices, Shops) | Standard | Also typically qualifies for standard rates, assuming no unusual risks. |

| Industrial Electrician (Factories, Plants) | Medium Risk | May see a small increase (a 'loading') on the standard premium. |

| High Voltage or Live Line Work | High Risk | Expect a significant premium loading due to the increased danger. |

| Offshore/Rail/Power Station Electrician | High Risk | Often leads to a major premium increase, or cover may be declined. |

| Working at Significant Heights (>12m) | High Risk | Premiums will be higher; some insurers may have specific exclusions. |

As you can see, where you work matters just as much as what you do. An insurer's main goal is to match the price of your policy to the level of risk they are taking on.

Personal and Lifestyle Factors

Of course, it’s not all about your job. Insurers will also look at the same personal factors they do for everyone else. These are just as crucial for calculating your premium and have nothing to do with the risks of your trade.

Your health, age, and lifestyle choices are just as important as your occupation in determining your life insurance premium. A healthy, non-smoking electrician in their 30s will almost always pay less than a 50-year-old smoker in the same job.

These standard assessment points include:

- Age: It's a simple fact – the younger you are when you take out a policy, the your premiums will be.

- Health and Medical History: They will ask about your current health, your weight, and any pre-existing conditions you might have.

- Lifestyle Choices: This covers the big ones like your smoking status and alcohol consumption, but also any high-risk hobbies like rock climbing or motorsports.

Being completely honest and upfront about both your work and your personal details is the best approach. It’s the only way to make sure you get the right cover at a fair price.

Choosing the Right Life Insurance Policy

Once you’ve got your head around how insurers see your job, the next step is picking a policy that actually fits your life. Life insurance in the UK isn't a one-size-fits-all product; it's a whole range of options built for different situations. The right choice for you will hinge on your personal circumstances – things like whether you have a mortgage, young children depending on you, or if you're thinking about inheritance.

Think of it like picking the right tool for the job. You wouldn't use a multimeter to hammer in a nail, and the same logic applies here. Getting the right policy means your financial protection is doing exactly what you need it to do, efficiently and effectively.

For most electricians, the decision boils down to one of three main types of cover. Let's break them down with some real-world examples to see how they actually work.

Level Term Insurance

Level Term Insurance is as straightforward as it gets. You pick a lump sum amount (the payout) and a policy length (the term), and both stay exactly the same for the whole time. If you pass away within that term, your family gets the pre-agreed amount, tax-free.

This policy is perfect for creating a fixed financial safety net for your loved ones.

- Example Scenario: Mark is a 35-year-old self-employed electrician with two young children. He wants to be sure that if anything happened to him before they're financially independent, there's enough cash to cover childcare, university fees, and day-to-day living costs. He takes out a £250,000 level term policy that runs for 25 years.

Decreasing Term Insurance

Decreasing Term Insurance is built for one main job: to cover a big debt that shrinks over time, like a repayment mortgage. The potential payout goes down each year, roughly matching what you still owe on your mortgage. Because the insurer's risk is dropping over time, this is usually the cheapest type of life cover you can get.

- Example Scenario: Sarah, a 28-year-old electrician, has just bought her first flat with a £180,000 repayment mortgage over 30 years. She takes out a decreasing term policy to run alongside it. If she were to pass away, the policy would pay out enough to clear the mortgage, meaning her partner wouldn't have to worry about losing their home.

Whole of Life Insurance

Just as the name suggests, Whole of Life Insurance covers you for your entire life, not just a set period. As long as you keep paying the premiums, it guarantees a payout whenever you die. Because of that guarantee, it costs more than term insurance. People often use this type of policy for inheritance tax planning or to make sure there's money set aside for funeral costs.

As you weigh up your options, you might come across other types of cover, like Variable Universal Life Insurance, which can help you make a well-rounded decision, though these are less common in the UK market. For a proper deep dive into the most popular UK policies, you can read more in our detailed guide on how to choose the right life insurance.

Protecting Your Livelihood with Add-On Cover

Standard life insurance is a fantastic way to protect your family's future, but it only pays out after you’ve passed away. What happens if a serious illness or accident takes you off the tools while you're still alive? As an electrician, your income relies on you being physically able to work. Losing that can put your family’s finances in immediate jeopardy.

This is where add-on policies, often called 'living benefits', become so important. They build a vital safety net that protects you and your income, not just your loved ones after you're gone. For anyone in a physical trade, these covers are arguably just as crucial as life insurance itself, giving you cash when you need it most.

Critical Illness Cover Explained

Critical Illness Cover does exactly what it says on the tin. It's a policy that pays out a tax-free lump sum if you're diagnosed with one of the specific, serious conditions listed by the insurer. We’re talking about major health events like a heart attack, stroke, or certain types of cancer.

Think of it as a financial first-aid kit. The payout gives you instant breathing space to sort out your finances, letting you focus on getting better without the added stress of bills piling up.

The money from a critical illness claim is yours to use however you need it. It could clear the mortgage, pay for private treatment to speed up your recovery, or simply cover the household bills while you can't earn.

Income Protection Insurance

While critical illness cover gives you a one-off payment, Income Protection Insurance works quite differently. It’s designed to replace a chunk of your monthly earnings if you're unable to work due to any illness or injury – not just a specific list of critical ones.

This policy pays a regular, tax-free income until you're fit enough to get back on the tools, you retire, or the policy term ends, whichever comes first. For a self-employed sparky with no sick pay to fall back on, this can be the difference between staying afloat and facing real financial hardship. We explore how this can also help during unexpected unemployment in our guide to income protection and redundancy.

How These Covers Work in Practice

Let's look at a real-world example to see how this all comes together for someone in your trade.

- Scenario: David, a 42-year-old electrician, has a nasty fall from a ladder and suffers a serious back injury. His doctor tells him he will be unable to work for at least a year.

- Without Cover: David’s income dries up instantly. His family is forced to burn through their savings and rely on state benefits, quickly falling behind on the mortgage and everyday bills. The financial pressure makes a difficult situation much worse.

- With Cover: David's Income Protection policy kicks in after his pre-agreed waiting period. He starts receiving 60% of his usual monthly income, tax-free. This allows his family to keep up with their costs and maintain their lifestyle. With the money worries taken care of, he can concentrate fully on his physiotherapy and recovery without the fear of losing his home.

By combining your life insurance with these living benefits, you create a protection plan that's truly robust. It ensures your family is looked after whether you're no longer around or simply can't work, safeguarding the future you've worked so hard to build.

The Hidden Risks of Being Underinsured

It’s a common trap many electricians fall into: assuming the 'death in service' benefit from your employer has you covered. And while it’s a decent perk to have, relying on it alone can leave your family in a seriously vulnerable position if the worst happens.

Death in service cover usually pays out a multiple of your salary, often somewhere between two and four times what you earn. On paper, that sounds like a lot of money. But when you start doing the maths, you quickly realise it might not even be enough to clear the mortgage, let alone cover all the family's living costs for years to come.

The biggest catch? This cover is tied to your job. If you switch firms, decide to go self-employed, or get made redundant, that protection disappears overnight. It often vanishes just as you're getting older and finding your own personal life insurance has become a lot more expensive.

Challenging the "It Won’t Happen to Me" Mindset

When you're busy on the tools, it's easy to push thoughts of accidents or illness to the back of your mind. But the reality of working as a sparky is that the risks are always there, whether it's from high voltages or simply working at height. The immediate physical dangers are obvious, but the real hidden threat is the financial devastation for your family if you’re not properly prepared.

Data from the Association of British Insurers (ABI) shows that while many people have some form of life insurance, a significant number are underinsured. This is particularly true for those in skilled trades where incomes can be high, but so are the risks.

Being underinsured means that even if you have some cover, the payout wouldn't be enough to maintain your family's standard of living, pay off the mortgage, and secure their future. It's a gamble that’s simply not worth taking.

Without enough personal electrician life insurance, your family could be forced to make some difficult decisions. They might have to sell the family home, use up their savings, or take on debt just to keep their heads above water. That's a mountain of financial stress piled on top of an already heartbreaking emotional loss.

A personal life insurance policy isn't a 'nice-to-have'; it's a non-negotiable part of your financial toolkit. It's yours, it’s designed around your family’s actual needs, and it sticks with you no matter who signs your pay cheques. It’s the only real way to guarantee the future you're working so hard to build is truly secure.

Securing the Best Electrician Life Insurance Quote

Navigating the insurance market can feel like trying to understand a complex wiring diagram, but getting the best cover for you and your family breaks down into a few simple steps. With the right approach, you can secure robust protection at a price that makes sense.

Your first step is always transparency. When you fill out your application, be completely upfront about your health, lifestyle, and exactly what your job involves day-to-day. Honesty isn't just the best policy; it's essential to ensure the cover you get is rock-solid and will pay out without a problem when your family needs it most.

Compare Quotes from Multiple Insurers

You wouldn't buy the first reel of cable you see without checking the price at a couple of suppliers, would you? The same logic applies to life insurance. Premiums can vary wildly between providers, even for the exact same level of cover. Some insurers are simply more comfortable with the trades and might offer you a much better rate.

The single most effective way to save money and find the right policy is to compare quotes from a wide range of UK insurers. It’s the only way to be sure you aren’t overpaying and that you’ve found a provider who properly understands your profession.

Work with a Specialist Broker

This is where a specialist broker, like us here at Discount Life Cover, can make all the difference. Instead of spending hours contacting dozens of insurers yourself, we do all the legwork for you. We know this market inside and out, so we can quickly pinpoint which providers will likely offer the best terms for someone with your specific circumstances.

It’s also reassuring to know that all advice and quotes you receive in the UK are regulated by the Financial Conduct Authority (FCA), giving you peace of mind that you're protected as a consumer.

Armed with this knowledge, you’re in a great position to find the right protection. The next move is yours – take action and get a personalised, no-obligation quote to secure your family’s financial future.

Your Questions Answered

We get a lot of questions about how life insurance works for tradespeople. Here are some clear, straightforward answers to the common queries we hear from electricians like you.

Is Life Insurance More Expensive for Electricians?

Not usually, no. It’s a common myth, but the vast majority of electricians working in standard domestic or commercial settings can get life insurance at standard rates. Insurers are far more interested in the specifics of what you do day-to-day—like consistently working at extreme heights or with exceptionally high-voltage equipment—than they are in your job title.

For most sparkies with a solid safety record, your personal health and lifestyle choices will have a much bigger impact on your premium than your profession.

Do I Need to Tell My Insurer if My Job Changes?

Absolutely, yes. It's vital to keep your insurer in the loop. Think about it: if you switch from wiring new builds to maintaining offshore wind turbines, the risk profile of your job has changed dramatically. Not telling them about a significant change like that could, in the worst-case scenario, invalidate your policy.

Always give your provider a heads-up about any major changes to your work. This ensures your cover stays valid and your family remains fully protected.

Is My Employer’s Death in Service Benefit Enough?

Relying solely on a death in service benefit is a risky strategy. These policies typically pay out a fairly small multiple of your salary (often 2-4x), which might not stretch far enough to clear the mortgage and support your family for the long term.

The biggest catch? This cover is tied directly to your job. If you change employers, go self-employed, or are made redundant, that protection vanishes overnight, leaving your family completely exposed. A personal electrician life insurance policy is yours and yours alone, giving you and your family security that you control, no matter where you work.

Ready to find the right protection for your family? The team at Discount Life Cover can help you compare quotes from the UK's leading insurers to find a policy that fits your job and your budget.

Get Your Free, No-Obligation Quote Today

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply