Let's get one thing straight: driving a lorry for a living is a tough job with its own set of risks, but that doesn't mean getting affordable life insurance is complicated. It's actually more straightforward than you might think.

In the UK, there isn't a special "lorry driver life insurance" policy. Instead, you for standard life insurance, and the underwriters simply factor your profession into their assessment. This guide will explain how it all works, what policies are best for you, and how to get the right cover without paying over the odds.

Why Lorry Drivers Need a Financial Safety Net

Life on the road isn't a standard 9-to-5. You're dealing with long hours, extended periods away from home, and the obvious risks that come with operating a heavy goods vehicle. Because of this, having a solid financial backup plan isn't just a 'nice to have'—it's essential.

Life insurance is the ultimate safety net for your loved ones. It’s there to provide them with stability and security if the worst should happen.

It’s a common myth that being a lorry driver is a major hurdle to getting affordable life cover. While insurers do need to understand the specifics of your job, it’s just one piece of the puzzle. Your role is simply another factor in a standard application, sitting alongside your age, health, and lifestyle.

Protecting What Matters Most

At its core, life insurance is about shielding your family from financial hardship. If you were no longer around, your income would stop, but the mortgage, rent, and bills certainly wouldn't. A life insurance payout provides a tax-free lump sum that can tackle those immediate and long-term costs head-on.

Here’s what that financial support could cover:

- Mortgage or Rent: Keeping a roof over your family's head without the stress of monthly housing payments.

- Household Bills: Taking care of day-to-day running costs like utilities, council tax, and food, so your family can maintain their standard of living.

- Outstanding Debts: Wiping the slate clean on personal loans, credit card balances, or car finance, so those burdens aren't passed on.

- Childcare and Education: Creating a fund for your children's future, whether that's for nursery fees, university costs, or just helping them get started in life.

The Reality of the Profession

The haulage industry is the backbone of the UK economy, with around 268,000 people employed as Heavy Goods Vehicle (HGV) drivers. This is a massive workforce facing unique occupational hazards, which is naturally something life insurance providers consider.

A robust life insurance policy acknowledges the risks you take on every day while giving you total peace of mind. It ensures all your hard work translates into long-term security for your family, no matter what happens down the road.

Beyond the worst-case scenario, it’s also wise to think about what would happen if you couldn't work due to illness or injury. While life insurance pays out upon death, other policies are designed to protect your earnings while you're still here. To learn more about protecting your income if you're made redundant or can't work, check out our guide on income protection and redundancy cover. This kind of policy provides a regular monthly income to help you stay on top of your finances during tough times, adding another vital layer of protection for you and your family.

How Insurers Assess Your Risk on the Road

When you for lorry driver life insurance, insurers are trying to build a complete picture of you. They gather information from different parts of your life to get a sense of the risk involved before they can give you a final price for your premium.

This isn't about penalising you for being a professional driver. It's simply about pricing a policy fairly based on a mix of factors from both your work and personal life. All UK insurers are regulated by the Financial Conduct Authority (FCA), ensuring this process is fair and transparent.

Your Professional Profile

First, an insurer will want to get to grips with your day-to-day work. They need to understand the nuts and bolts of your job, because not all HGV driving roles are created equal when it comes to risk.

Here's what they'll likely look at:

- HGV Licence Class: The type of vehicle you operate (e.g., Class 1 versus a Class 2) gives them an idea about the complexity of your job.

- Type of Goods Transported: There’s a world of difference between hauling pallets of crisps and transporting flammable liquids or chemicals. Carrying hazardous materials (ADR work) is naturally seen as a higher-risk job.

- Typical Driving Hours: Are you working long, unpredictable shifts or more regular hours? Insurers know that fatigue is a serious risk factor in the transport industry.

- Routes Driven: Doing long-haul international runs might be viewed differently from making local drops around the UK. Factors like different road conditions and more time away from home can play a part.

While insurers look at the risks of the job itself, your own safety record matters. Consistently performing thorough pre-trip inspections shows you’re a responsible professional, and that's always a big plus in their book.

Your Personal Profile

Once they have a handle on your professional life, the insurer will combine it with your personal details to complete the picture. These are the same sorts of questions anyone ing for life insurance would be asked, regardless of their job.

An insurer's job is to balance the facts. They weigh the professional risks of your driving career against the personal details of your health and lifestyle to arrive at a fair premium.

The key personal factors are:

- Age and Health: It's no surprise that younger, healthier applicants usually get lower premiums. They'll ask about your medical history, any existing conditions like high blood pressure or diabetes, and your height and weight (BMI).

- Lifestyle Choices: Your habits outside the cab make a difference. Smoking or vaping will increase your premiums significantly, as will heavy drinking.

- Driving Record: While this is crucial for your vehicle insurance, a history of serious driving offences (like a drink-driving conviction) could also give a life insurer pause for thought.

At the end of the day, this assessment explains why quotes for lorry driver life insurance can be so different from one person to the next. Two drivers with the exact same job title could get completely different prices based on their own unique mix of work duties, health, and lifestyle.

Choosing the Right Policy for Your Journey

Trying to pick a life insurance policy can feel a bit like reading a complex road map without a satnav. With so many different routes on offer, it’s easy to feel lost. This section is your personal guide, cutting through the jargon to help you figure out the most common and suitable policies for lorry drivers here in the UK.

The key is to match the policy to where you are in life. Are you a young driver who's just taken on a mortgage and is starting a family? Or perhaps an older driver wanting to cover funeral costs and leave a small gift for the grandkids? The right policy for one person might be completely wrong for another.

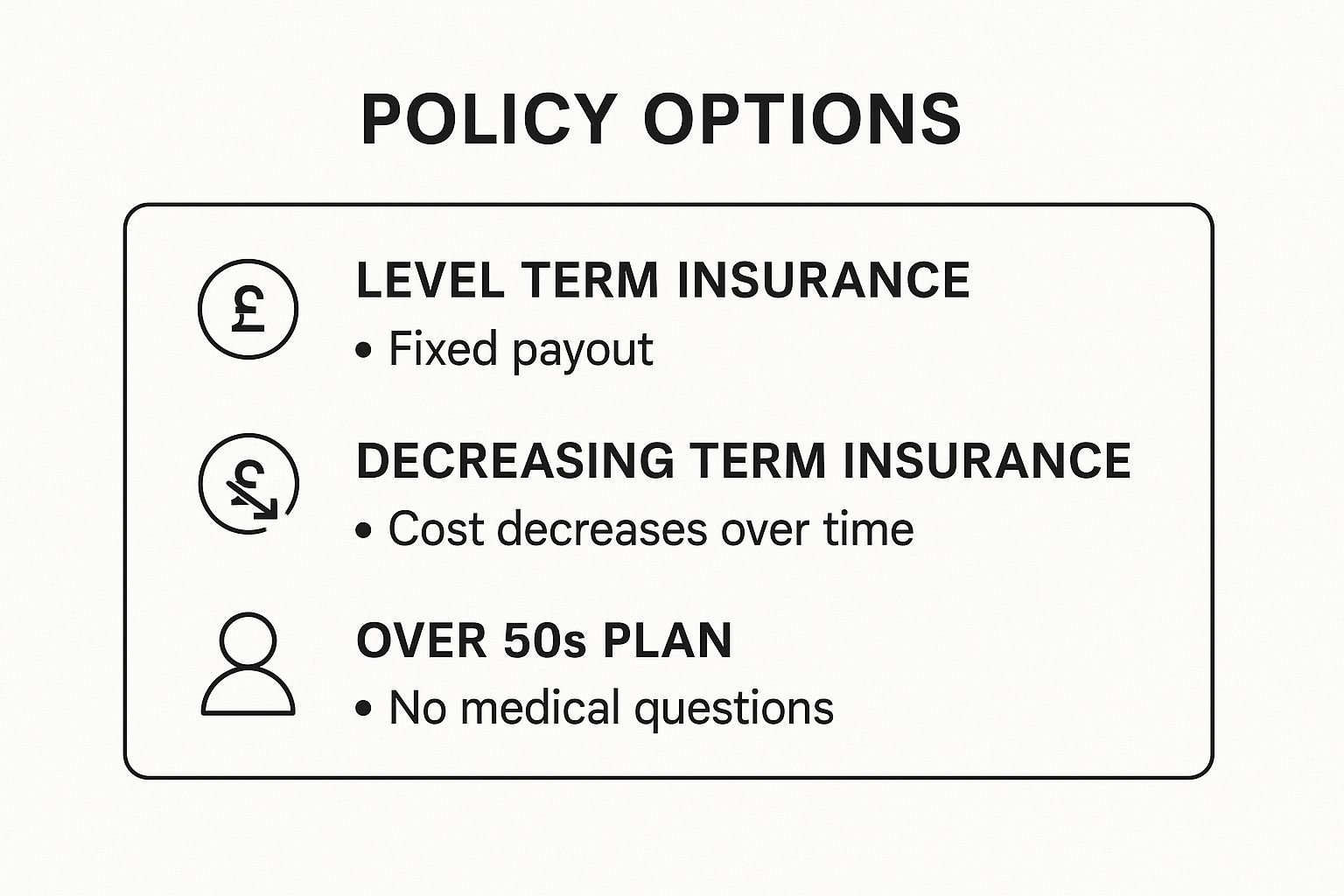

Level Term Insurance: A Fixed Payout for Peace of Mind

Level term insurance is one of the most straightforward types of cover. It’s simple: you pick a set amount of cover (the payout) and a specific period of time (the term), say, £150,000 over 25 years. If you pass away within that term, your family receives the full £150,000 as a tax-free lump sum.

The "level" part is important—it means your monthly premium and the final payout amount stay the same for the whole policy. That predictability makes it a brilliant choice for families who need a reliable financial safety net.

- Best for: Covering an interest-only mortgage, replacing your lost income to cover living costs, and providing for your children until they are financially independent.

- Example: A 40-year-old lorry driver with two young kids might take out a £200,000 policy for a 20-year term. This ensures that if the worst should happen, there’s a solid fund in place to support their family.

Decreasing Term Insurance: Cover That Shrinks with Your Mortgage

Decreasing term insurance works a little differently. The total payout amount gradually reduces over time, usually in line with a large repayment debt like a mortgage.

Because the potential payout gets smaller each year, the premiums for decreasing term insurance are almost always lower than for level term cover. This makes it a very cost-effective way to protect against a specific financial liability.

The main job of decreasing term insurance is to make sure your biggest debt—usually your mortgage—is paid off. This secures the family home for your loved ones, so they don’t have to worry about finding the money for repayments.

- Best for: Homeowners with a repayment mortgage.

- Example: A driver with £180,000 left on a 22-year repayment mortgage could take out a decreasing term policy to match it. As they pay down the mortgage, the life insurance cover drops alongside it, making sure the remaining balance is always covered.

Over 50s Plans: Acceptance for Later Life

For drivers aged 50-85, a competitive acceptance Over 50s plan can be a great option. These policies are designed to be incredibly accessible, which means you won’t have to answer any medical questions or go through a health check to be accepted.

This infographic breaks down the core features of these key policy types.

The biggest draws for Over 50s plans are their simplicity and that competitive acceptance. The payout is usually smaller than with term insurance and is intended to cover things like funeral costs, settle small outstanding bills, or be left as a final gift to family. Premiums are fixed for life (or until a certain age, like 90).

- Best for: Older drivers (50-85) who may have health conditions or simply want a straightforward way to cover funeral expenses without medical checks.

- Example: A 58-year-old driver with some health issues wants to ensure their funeral is paid for. An Over 50s plan provides a competitive lump sum for this purpose.

Adding Critical Illness Cover for Extra Protection

Standard life insurance looks after your family after you’re gone, but what if a serious illness stops you from ever getting behind the wheel again? For a professional driver, a career-ending diagnosis can be just as financially devastating as death.

This is where Critical Illness Cover steps in. It's usually added to a life insurance policy for an extra cost and pays out a tax-free lump sum if you’re diagnosed with one of the specific, serious conditions listed in the policy. This payout gives you immediate financial breathing room, letting you focus on getting better without the stress of mounting bills.

Why Is Critical Illness Cover Important for Lorry Drivers?

The life of a lorry driver often means long, sedentary hours and unpredictable sleep, which can raise the risk of certain health problems. A serious diagnosis like a heart attack, stroke, or some cancers could mean having to surrender your HGV licence, cutting off your main source of income in an instant.

Some of the most common conditions covered include:

- Heart attacks

- Strokes

- Certain types and severities of cancer

- Multiple sclerosis

- Kidney failure

The list of illnesses covered will vary between insurers like Aviva, Legal & General, and Zurich, so it’s crucial to read the policy documents. A payout from this cover could be a genuine financial lifeline.

A critical illness diagnosis doesn't just impact your health; it can halt your career in its tracks. The payout from this cover acts as a financial buffer, replacing lost income and covering costs while you adapt to a new reality off the road.

Getting your head around exactly what is critical illness insurance and how it works with your main life policy is a key step in building a proper safety net.

How a Payout Can Be Used

The lump sum from a critical illness claim is paid directly to you, and it’s yours to use however you need. For a driver forced to give up their licence, the money could be used to:

- Pay off the mortgage or cover rent for several years.

- Clear outstanding debts like car finance or credit cards.

- Fund private medical treatment or specialist therapies.

- Make adaptations to your home, like installing a stairlift.

- Cover everyday living costs while you can't earn.

In short, it provides a vital financial cushion and buys you and your family time to adjust without the immediate panic of a lost salary.

Practical Steps to Lower Your Insurance Premiums

It’s a common myth that having a higher-risk job means you're automatically stuck with sky-high insurance costs. You actually have more say over the price of your life insurance than you might realise. Taking a few sensible steps can genuinely lower your monthly premiums, all without having to settle for a lesser policy.

Focus on Your Health and Lifestyle

One of the most powerful ways to bring down your insurance costs is by looking after your health. Insurers reward a healthy lifestyle with lower premiums.

Quit Smoking: This is the big one. Smokers and vapers can easily pay double what a non-smoker pays for the same cover. If you can stay nicotine-free for at least 12 months, most insurers will reclassify you as a non-smoker, which could slash your costs.

Maintain a Healthy Weight: Your Body Mass Index (BMI) is a key health marker for insurers. A high BMI often means higher premiums, so focusing on a balanced diet and exercise can make a real financial difference.

Reduce Alcohol Intake: Be honest about how much you drink per week. If your consumption is within the NHS recommended guidelines, you're more likely to get a standard rate without price hikes.

Be Smart About Your Application

How you for cover is every bit as important as your health or your job.

Always Compare Quotes: This is non-negotiable. Never just take the first price you're offered. Premiums for lorry drivers can vary massively between providers because they all weigh risk differently. Using a specialist broker lets you see quotes from dozens of UK insurers in one place, making sure you don't miss out on the best deal. You can get a feel for how prices work by looking at different term life insurance rates.

Be Completely Honest: It might seem tempting to gloss over a health condition or not mention that you smoke, but this is a huge mistake. Hiding information is called 'non-disclosure', and it can completely invalidate your policy. If that happens, your family gets nothing. Being upfront from the start is the only way to guarantee your cover is solid.

While this guide is about personal life insurance, some of the same logic applies to commercial policies too. You might find some useful tips in articles that discuss ways to reduce truck insurance costs for more ideas on proving you're a lower-risk driver.

FAQ: Common Questions from Lorry Drivers

Here are straight answers to the most common questions we get from drivers about life insurance.

Will points on my driving licence affect my life insurance application?

For minor offences like a couple of speeding tickets, life insurers generally aren't concerned. However, a history of serious convictions, such as for drink-driving (DR10), could be seen as a sign of a riskier lifestyle and may lead to higher premiums. Always be honest about your driving history.

Do I need to tell my insurer if I start hauling hazardous goods?

Yes, absolutely. Your life insurance is a contract based on the information you provided at the start. If your job role changes significantly to become higher risk (e.g., moving from general haulage to transporting hazardous materials), you must inform your insurer to ensure your policy remains valid.

Is my employer's Death in Service benefit enough?

Death in Service cover is a valuable employee benefit, but it's risky to rely on it alone. The cover is tied to your job – if you leave, you lose it. The payout is also typically only 2-4 times your salary, which may not be enough to clear a mortgage and support your family long-term. A personal life insurance policy belongs to you, stays with you regardless of your employer, and can be tailored to the exact amount your family needs.

What if I have a medical condition? Can I still get cover?

Yes, in most cases. It is rare to be declined for life insurance outright. If you have a pre-existing medical condition, an insurer might offer you cover with a higher premium or add an 'exclusion' for that specific condition. For older drivers or those with more complex health issues, a Over 50s plan is an option as it doesn't require any medical questions. The key is to shop around, as some insurers are more lenient with certain conditions than others.

Ready to find the right cover to protect your family's future? At Discount Life Cover, we make it simple to compare quotes from the UK's leading insurers, ensuring you get the best possible price for your lorry driver life insurance.

Get your free, no-obligation quote today and secure peace of mind on the road.

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply