Securing construction worker life insurance is a vital step in protecting your family’s financial future. It’s a physically demanding trade with inherent risks, and the right cover ensures your loved ones receive a tax-free lump sum if you were to pass away. This financial safety net helps them manage the mortgage, household bills, and daily living costs without your income.

Why Your Trade Needs Specialist Life Insurance

Working in construction is physically demanding and carries daily risks far beyond a typical office job. From working at height on scaffolding to operating heavy machinery, your profession is viewed differently by insurers. A standard, one-size-fits-all policy may not provide adequate protection, potentially leaving dangerous gaps in your cover or unpleasant surprises in the small print.

Specialist life insurance is designed for the realities of your work. The insurers offering these policies understand the distinction between a scaffolder and a site manager. They assess your application based on the specifics of your role, not a generic "construction" label. Getting this right is crucial for finding a policy that offers proper protection at a fair price.

Understanding the Insurer's Perspective

When you for a policy, an insurer's primary task is to assess the level of risk they are taking on. For anyone in the construction trades, they will focus on several key areas:

- Working at Height: How much of your time is spent working above ground level, and at what height?

- Machinery Use: Do you operate heavy or potentially dangerous equipment?

- Hazardous Materials: Are you exposed to substances like asbestos, solvents, or industrial chemicals?

- Location of Work: Does your job take you to high-risk environments, such as motorways, railway lines, or demolition sites?

Being completely transparent about these details is essential. It enables the insurer to offer you the right cover from the outset, preventing claim rejections when your family needs the payout most. For those in particularly high-risk roles, it is worth exploring policies designed specifically for hazardous occupation cover.

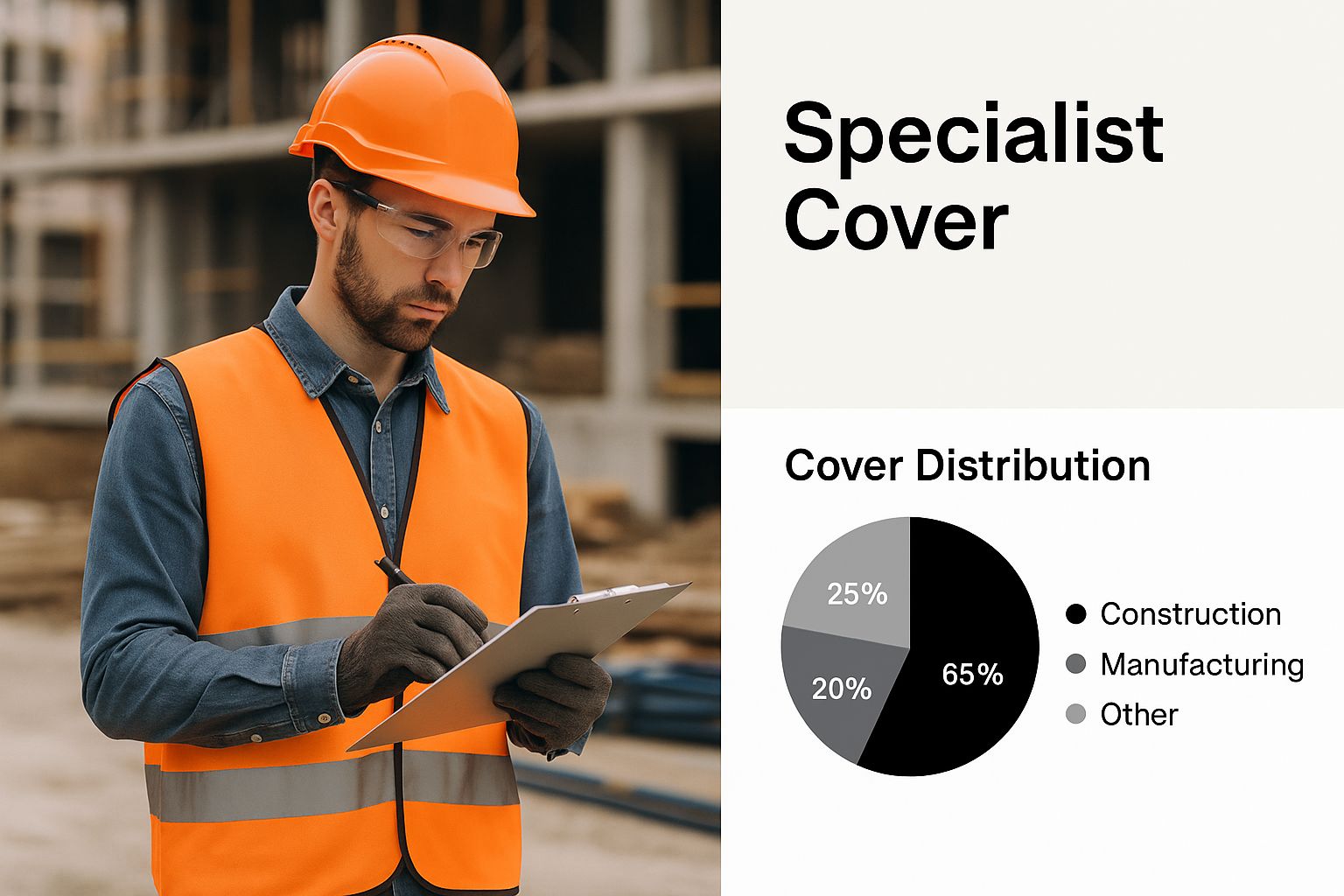

This infographic provides a clear overview of why a specialist approach is so important for the construction industry.

As you can see, a generic policy simply doesn't account for the unique dangers you face on site every day.

Securing Financial Peace of Mind

Ultimately, life insurance is about providing peace of mind. Knowing your family is protected should the worst happen is invaluable. The UK insurance market, regulated by the Financial Conduct Authority (FCA), is well-equipped to provide robust protection, even for high-risk occupations. Finding affordable, comprehensive cover is entirely achievable.

By working with a specialist broker, you can connect with an insurer who genuinely understands your trade and won't penalise you unfairly. This protection ensures the mortgage gets paid, debts are cleared, and your family can remain financially stable. It’s not just an insurance policy; it’s the foundation of your family’s financial security.

How Your Job Role Impacts Your Premiums

Have you ever wondered why a roofer might pay more for life insurance than a site manager? It all comes down to the underwriting process, where insurers carefully assess the specific risks associated with your trade. It’s not as simple as categorising everyone under a single "construction" umbrella; the details of your daily job make all the difference.

Insurers see a wide variety of roles within the construction industry, each with its own risk level. A steel erector working at significant heights faces entirely different hazards than an architect who spends most of their time in an office with occasional site visits. This is why obtaining the right construction worker life insurance depends on providing a crystal-clear picture of your day-to-day responsibilities.

The Logic Behind Risk Assessment

When an underwriter reviews your application, their main objective is to determine the likelihood of a claim. For those in construction, they focus on several key factors that directly impact your premiums.

- Working at Height: This is a major consideration. The more time you spend off the ground, and the higher you go, the greater the risk an insurer perceives.

- Operating Heavy Machinery: Roles involving cranes, diggers, or other powerful equipment are often considered higher risk due to the potential for serious accidents.

- Handling Hazardous Materials: If your job involves exposure to substances like asbestos, industrial chemicals, or even heavy dust, insurers will factor in the potential long-term health effects.

- Working Environment: Your work location also matters. A job on a busy motorway, railway line, or demolition site naturally carries more risk than working on a new residential build.

The UK construction industry is vast, employing around 2.2 million people. With such a wide range of roles, it makes sense that insurers use different criteria. Crane operators might see higher premiums, while surveyors often benefit from a smoother underwriting process.

Comparing Different Construction Roles

To illustrate, let's look at how insurers might view different trades. Not all construction jobs are equal in their eyes, and this table provides a general idea of their logic. Remember, your final premium will always depend on your full personal circumstances. Comparing different term life insurance rates can also give you a better understanding of how these factors add up.

Example Risk Levels and Potential Premium Impact for Construction Trades

| Risk Level | Example Job Roles | Key Risk Factors | Typical Premium Impact |

|---|---|---|---|

| Lower Risk | Architect, Surveyor, Site Manager | Primarily office-based, occasional site visits, minimal physical risk. | Standard or near-standard premiums. |

| Moderate Risk | Electrician, Plumber, Bricklayer | Regular physical work, some work at height, use of power tools. | Small increase on standard premiums. |

| Higher Risk | Scaffolder, Roofer, Steel Erector | Frequent work at significant heights, heavy lifting, high-risk environments. | Noticeable increase, may require a specialist insurer. |

This breakdown highlights why being honest and detailed in your application is so important. When you accurately describe your duties, you help the insurer place you in the correct risk category. Ultimately, this means you get a fair price for the right level of cover, with no unwelcome surprises later on.

Choosing the Right Life Insurance Policy

Understanding life insurance can feel overwhelming, but it essentially comes down to choosing the right tool for the job. For those in construction, selecting a policy is not just a tick-box exercise; it's about building a solid financial defence for your family that truly meets your needs.

Let's break down the main options in plain English.

Most policies fall into a category known as term insurance. This simply means the policy runs for a fixed period – for example, 25 years – and only pays out if you pass away during that term. It's a straightforward and often highly affordable way to secure a significant amount of protection when your family needs it most.

Within term insurance, there are two key types that serve different purposes. Understanding the distinction is vital for making the right choice.

Level Term vs Decreasing Term Cover

Think of these two policies as tools designed for different jobs on the same site.

Level Term Insurance: With this policy, the payout amount (the 'sum assured') remains the same from the first day to the last. If you take out a £200,000 policy for 20 years, your family receives £200,000 whether you pass away in year one or year nineteen. This makes it ideal for covering costs that don't decrease over time, like replacing your income to handle rent, bills, childcare, and other family expenses. It is often chosen by parents with young children.

Decreasing Term Insurance: This type of cover is specifically designed to protect a repayment mortgage. The payout amount reduces over time, roughly in line with your outstanding mortgage balance. Because the insurer's potential payout gets smaller each year, the premiums are typically lower than for a level term policy. It’s a very cost-effective way to ensure your largest debt is cleared.

Whole of Life Insurance

Another option is Whole of Life insurance. Unlike term policies, this cover has no end date. It guarantees a payout whenever you pass away, provided you have kept up with the monthly payments.

Because the payout is certain, these policies are more expensive. They are often used for specific financial planning purposes, such as covering a potential inheritance tax bill or leaving a competitive legacy for your children or grandchildren.

For most young families and homeowners in the trades, a term policy provides the best value for money and the protection you need right now.

Choosing the right policy ensures your financial safety net is fit for purpose. A Decreasing Term policy is perfect for mortgage protection, while Level Term provides a consistent lump sum to support your family's ongoing lifestyle.

It’s also worth remembering that other legal arrangements can be important. For instance, putting your policy 'in trust' can help ensure the payout goes to your chosen beneficiaries quickly and avoids being counted for inheritance tax purposes. While we can provide information, it's always best to seek legal advice on matters like how guardianship impacts life insurance policies to ensure your long-term plans are secure. The main thing is to match your policy directly to the financial promises you want to keep for your family.

Protecting Your Livelihood While You're Still Here

Protecting your family’s finances isn’t just about what happens if you’re no longer around. In a physically demanding trade like construction, a serious illness or injury is a far more common threat to your income than death. This is where your financial safety net needs to be at its strongest, covering you while you're still here.

Two crucial layers of that safety net are Critical Illness Cover and Income Protection. It's best to think of them as essential tools in your kit, designed to protect your earnings and keep your family stable if you’re suddenly unable to work.

Critical Illness Cover Explained

Critical Illness Cover is straightforward: it pays out a one-off, tax-free lump sum if you're diagnosed with a specific, serious condition listed in your policy. These are major life events like a heart attack, stroke, or certain types of cancer.

For a construction worker, this money can be a lifeline. For example, a self-employed bricklayer diagnosed with a critical illness could use the payout to clear the mortgage, pay for home adaptations, and handle bills. It provides the financial breathing space to focus completely on recovery, without the added stress of worrying about returning to work.

Income Protection Insurance

While Critical Illness Cover provides a lump sum for a specific event, Income Protection works differently. It pays you a regular, replacement monthly income if any illness or injury covered by your policy prevents you from working. It’s designed to keep money coming in, month after month, until you can get back on the tools.

Consider an electrician who suffers a severe back injury and is signed off work for a year. Income Protection could replace a significant portion of their lost earnings, ensuring the rent, food, and bills are covered. For the self-employed, who have no employee sick pay to fall back on, this type of cover is less of a 'nice-to-have' and more of an absolute necessity. You can learn more about how income protection covers you during these periods.

The toll of the job isn't just physical. Mental health challenges are a significant issue in the UK construction sector, with many workers experiencing poor mental health in often stressful conditions. This can lead to significant time off work, making income protection a vital support system for both physical and mental wellbeing. Discover more insights about these workplace risks.

Finding the Best and Most Affordable Cover

Securing the right construction worker life insurance at a price that fits your budget isn't just about finding the cheapest quote. It’s about getting solid protection from an insurer who understands what you do for a living.

The single most important step is to be completely upfront when you . Insurers need the full picture of your job – how often you work at height, the tools you use daily, and the specific sites you work on.

It might be tempting to omit details to get a lower premium, but that's a risk not worth taking. If you fail to disclose important information and your family needs to make a claim, the insurer could reduce the payout or, in the worst case, void the policy entirely. Honesty ensures the policy will perform when it’s needed most.

Why a Specialist Broker Is Your Best Tool

Navigating the insurance market alone can be challenging, especially in a high-risk trade. That's where a specialist broker like Discount Life Cover makes a real difference. We know the UK insurers, including those from major providers like Aviva, Legal & General, and Zurich, who are more reasonable when it comes to the construction industry.

A specialist broker is on your side. They understand how insurers assess risk for trades like yours and can connect you with providers offering fair terms. This alone could save you hundreds of pounds a year compared to going with a standard provider.

Our job is to match your unique situation to the right insurer, ensuring you don't pay more than necessary for the protection your family deserves. While life insurance is a crucial part of your plan, considering other practical options like over-50s plans or prepaid funeral services can also provide extra peace of mind for specific needs.

Ultimately, being transparent about your work and using an expert to compare the market is the smartest way to get robust, affordable cover that lets you get on with the job without worry.

Frequently Asked Questions (FAQ)

We understand that sorting out construction worker life insurance brings up specific questions related to your trade. Here are clear answers to some of the most common queries.

Can I get life insurance if I work at heights?

Yes, absolutely. Working at height is a standard part of many construction roles, and UK insurers are well-acquainted with it. During the application, you will be asked for specific details, such as the maximum height you work at and the proportion of your time spent at that height. Providing accurate information is key to securing a fairly priced policy that provides valid cover.

What if I move into a less risky role?

If you change your job from a hands-on role like a scaffolder to a less physically risky one, such as a site manager, you should inform your insurer. In many cases, this change can lead to a reduction in your monthly premiums. Your policy is not set in stone; insurers can review your cover when your circumstances change significantly. It’s always worth checking if your new role qualifies you for a better rate.

Is insurance more expensive if I’m self-employed?

No, being self-employed does not automatically increase the cost of your life insurance. Insurers are focused on the risks associated with your specific trade and your personal health, not your employment status. A self-employed electrician will undergo the same risk assessment as one employed by a large company. However, the lack of employer sick pay makes adding income protection or critical illness cover even more important for self-employed workers.

What happens if I don’t disclose all my duties?

This is critically important. Failing to provide a full and honest account of your job duties is known as 'non-disclosure' and can invalidate your policy. If you omit key information, such as handling hazardous materials, and a claim is later made, the insurer has the right to refuse the payout. Transparency from the start is the only way to guarantee the protection you are paying for will be there for your family.

Ready to find the right protection for you and your family? The team at Discount Life Cover are experts in finding affordable life insurance for tradespeople across the UK. Get a fast, free quote today and see how simple it can be.

➡️ Compare Cheap Life Insurance Quotes Now

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply