When you're navigating an incredibly tough situation, you need clear, straightforward answers. So let's get right to the heart of the matter: does life insurance pay out for suicide in the UK? The simple answer is yes, it usually does, but there's a crucial condition attached.

Understanding Suicide and Life Insurance Payouts in the UK

Almost every UK life insurance policy has what's known as a 'suicide clause'. In plain language, this means the policy won't pay out if the person covered dies by suicide within a specific timeframe, which is typically the first 12 months after the policy starts.

Once that initial period is over, a claim for a death by suicide would usually be paid out, just like any other claim, as long as all the other policy conditions have been met. It’s a sensitive topic, and this guide is here to walk you through it with clarity and compassion.

We'll break down exactly how this clause works and touch on why being honest about mental health when you first is so important. Getting to grips with these details is the key to making sure your family is truly protected.

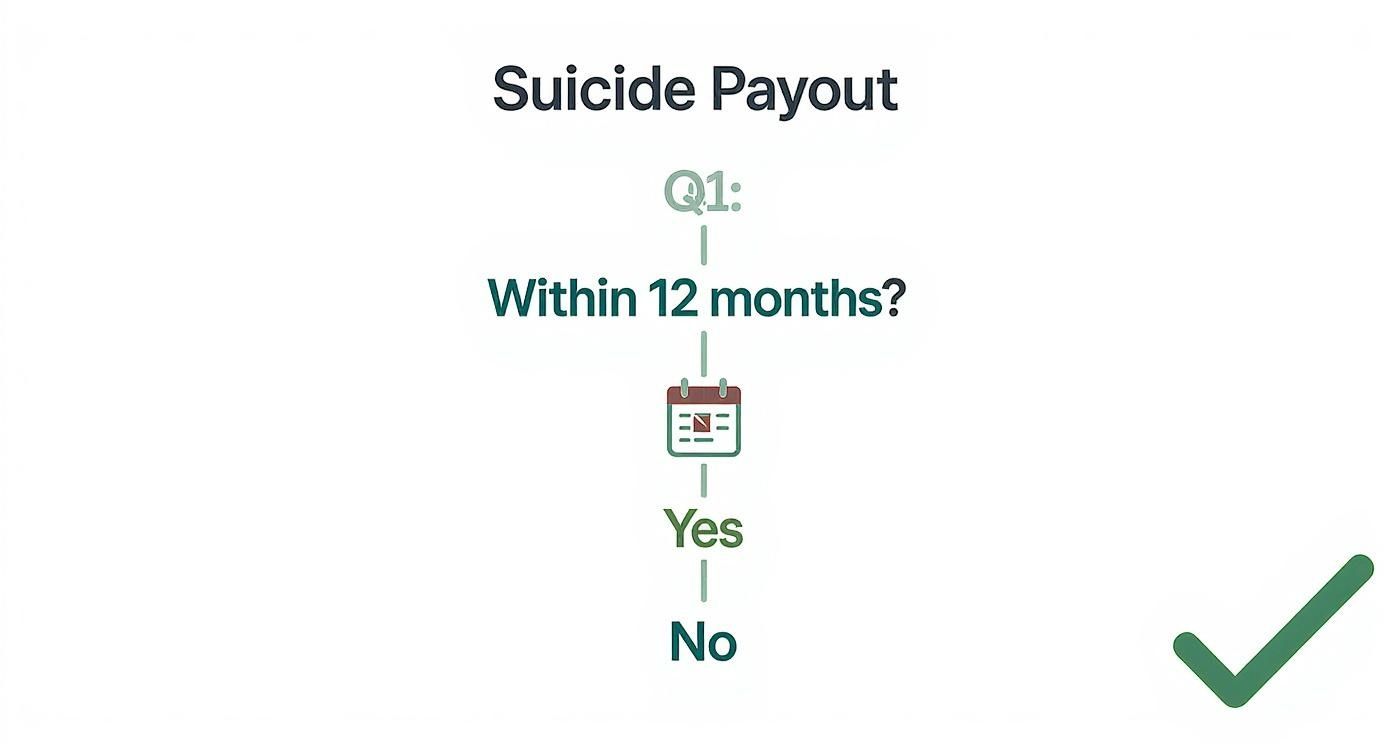

The Payout Decision Process

To make this crystal clear, here’s a simple visual that shows how insurers typically handle a claim in this situation.

As you can see, the timing is everything. The first thing an insurer will look at is how long the policy was in place before the death occurred. This is the most critical factor in their decision.

To give you a quick overview, here’s a simple table summarising the likely outcomes.

UK Life Insurance Suicide Payout Summary

| Scenario | Likely Payout Outcome | Key Factor |

|---|---|---|

| Death by suicide within the first 12 months of the policy | Claim Denied. Premiums may be refunded. | The 'suicide clause' is active during this initial period. |

| Death by suicide after the first 12 months of the policy | Claim Paid. The full sum assured is typically paid out. | The exclusion period has passed. |

| Non-disclosure of mental health issues on application | Claim may be Denied. Payout could be reduced or refused. | Honesty during the application process is a contractual requirement. |

Essentially, the suicide clause is standard practice across the board for UK insurers. After that initial 'exclusion period' of 12 months has passed, insurers will typically pay out the full amount to the beneficiaries. If you want to dive deeper into the general rules, you can discover more insights about life insurance rules at iaminsured.co.uk.

Understanding this rule is vital for homeowners, parents, or anyone with people who depend on them financially. Whether you're looking at a level term policy to cover your mortgage or an over 50s plan, this clause will almost certainly be in the small print. Our goal is to give you the facts your family needs to understand where they stand.

Understanding the Life Insurance Suicide Clause

Just about every personal life insurance policy in the UK has something called a suicide clause. It’s easy to misunderstand this, but it’s not meant to be a penalty. Think of it as a standard safety feature for the insurance provider. Its main job is to prevent a tragic situation where someone might take out a large policy with the immediate intention of ending their life, just to leave a payout for their family.

This clause sets up a waiting period, sometimes called an exclusion period. This is a specific timeframe right at the start of your policy where a death by suicide won't be covered.

How Long Does the Suicide Clause Last?

The length of this waiting period can differ from one insurer to the next, but the most common timeframe you’ll see in the UK is 12 months from the day the policy begins. Some providers, such as Aviva or Legal & General, may extend this to 24 months, which is why it's so important to read your policy documents to know exactly where you stand.

If the policyholder dies by suicide within this initial period, the claim for the lump sum payout will almost certainly be denied. However, any reputable insurer will do the right thing and refund all the premiums that have been paid up to that point. This means your loved ones wouldn't get the large sum assured, but they would get back every penny that was paid for the cover.

Once this initial waiting period is over, the suicide clause essentially becomes inactive.

A claim for death by suicide that happens after the clause's waiting period has ended will generally be handled just like any other claim, as long as all the other policy terms have been met.

When the Clause Can Reset

Now, here's something crucial to grasp: this waiting period isn't always a one-and-done deal. The clause can actually be reapplied, or "reset," in a few specific situations.

For example, if you make a major change to your policy down the line, the clock on that waiting period might start ticking all over again. The most common triggers are:

- Increasing your cover amount: Let's say you increase your sum assured from £150,000 to £250,000 to cover a bigger mortgage. The suicide clause could restart, but usually only for the new, increased portion of the cover.

- Reinstating a lapsed policy: If you miss payments and your policy lapses, then you later get it reinstated, the insurer might treat this as a brand-new start date. This could reset the suicide clause for the entire policy.

Getting your head around these details is fundamental to knowing what protection you really have. This isn't some obscure rule designed to catch you out; it's a standard industry practice designed to keep things fair for everyone. Knowing these specifics is a key part of choosing the right life insurance policy to protect your family.

The Critical Role of Mental Health Disclosure

Think of a life insurance policy not just as a document, but as a contract built on a foundation of trust. It’s a two-way street. When you , the insurer needs a complete and honest picture of your health history to figure out the risk involved and offer you a fair deal. This absolutely includes your mental health.

It can feel incredibly daunting to share sensitive details about conditions like depression, anxiety, or especially any past suicide attempts. There's a common fear that being upfront will automatically lead to sky-high premiums or even an outright 'no'. While it's true that your health history shapes the terms of your policy, keeping quiet is a much, much bigger gamble.

In the insurance world, deliberately leaving out crucial facts has a specific name: 'non-disclosure'. This isn't a minor oversight; it's a serious issue that can give an insurer the legal right to completely void your policy, making it worthless. This principle is upheld by UK regulators like the Financial Conduct Authority (FCA).

The Consequences of Non-Disclosure

Let's imagine a scenario. A family makes a claim years after the policy was taken out, well past the initial suicide clause period. During the standard investigation, the insurer uncovers old medical records. These records show a history of severe depression that was never mentioned on the original application form.

This discovery of non-disclosure gives them solid grounds to refuse the payout. Just like that, your loved ones are left in the exact financial hole you worked so hard to protect them from. It's a truly heartbreaking outcome, and one that's entirely avoidable with transparency from day one.

Being honest on your application is the only way to guarantee that the contract you've paid for will be honoured when your family needs it most. Honesty protects your policy; silence can destroy it.

Why Full Transparency Is Your Safest Option

I can't overstate how vital full disclosure is. Any life insurance claim involving suicide in the UK triggers a thorough investigation before any decision is made. If the insurer finds out that mental health issues or substance abuse problems were hidden during the application process, they can refuse to pay out—no matter when the death occurred.

Research often suggests a high percentage of those who die by suicide have an underlying mental illness, which makes accurate disclosure absolutely critical for a valid policy. You can learn more about these claim investigation findings from Reassured.co.uk.

Ultimately, being upfront is always the best strategy. Insurers are experienced in assessing applications that include mental health conditions. Yes, it might affect your premiums, but it is far better to have a valid policy with slightly higher payments than a one that won't actually pay out.

For more guidance, you can explore our detailed article on how life insurance for various medical conditions is handled by UK providers. It’s all about protecting the financial security you’re working so hard to create for your family.

How Insurers Investigate a Suicide Claim

When a claim is submitted after a death by suicide, it naturally triggers a more thorough review than other types of claims. This isn't about being intrusive during an incredibly difficult time. It’s simply a necessary step for the insurer to make sure all the policy's terms were met before paying out.

It’s wise for families to know that this process can take a bit longer, so they’re prepared for what’s involved.

The first thing your beneficiaries will need to do is provide some key documents. This always includes the official death certificate, and usually the coroner’s report, which gives the formal cause of death.

The Two Main Areas of Focus

An insurer’s investigation really boils down to two key questions. Answering them confirms the policy is valid and the claim can be paid.

Confirming the Date of Death: The claims team will check the date of death against the policy’s start date. They’re making sure the death happened outside the initial suicide clause period, which is typically 12 months here in the UK. If the death falls inside this window, the claim for the full payout will almost certainly be denied, though any premiums paid are usually refunded.

Reviewing the Original Application: Next, the insurer will take a close look at the information provided on the original application form. They’ll cross-reference this with medical records requested from the deceased’s GP. The main thing they're looking for here are signs of non-disclosure — particularly around a history of mental health conditions or substance use that wasn't mentioned upfront.

In some cases, insurers use specialised teams or even independent insurance claim investigators to gather all the necessary facts.

The investigation's purpose is straightforward: to confirm that the policy is a valid contract based on honest disclosure and that the death occurred outside of any specific exclusion periods.

Knowing what to expect can help set realistic expectations for your loved ones. For a general overview of the claims process, our guide explains in detail how to claim on a life insurance policy in the UK. Being prepared with the right information really can make a big difference.

How Different UK Life Insurance Policies Treat Suicide

It’s a common mistake to think all life insurance policies play by the same rules, but when it comes to suicide, the details can vary quite a bit depending on the type of cover you have. Knowing these differences is crucial to understanding what protection is really there for your family.

For the most common policies that people take out themselves, like Level Term or Decreasing Term Insurance, you'll almost always find that standard 12 or 24-month suicide clause we've been talking about. These are the typical plans people buy to cover their mortgage or leave a financial cushion for their loved ones.

But the picture changes completely when we start looking at policies offered through your job.

Employer Schemes vs Personal Policies

The big exception to the rule is a 'Death in Service' benefit. This is a type of group life insurance that many employers provide as part of their benefits package.

One of the most significant features of these group schemes is that they typically do not have a suicide clause. This means that if an employee were to tragically die by suicide, the policy would generally pay out to their beneficiaries, regardless of how long they'd been with the company or covered by the scheme.

Group life insurance plans sponsored by employers are a significant exception, often providing a payout for suicide without the waiting period found in personal policies. In contrast, personal insurance claims for suicide within the exclusion period are usually denied. You can read the full analysis on global insurance trends from rgare.com.

This is a massive distinction. While your personal policy has that initial waiting period, the cover from your job could offer immediate protection for this specific cause of death.

Over 50s Policies

Another policy with its own unique structure is an Over 50s Plan. These plans are designed to offer competitive acceptance to UK residents aged 50-85, with no medical questions asked.

Because of this competitive acceptance, they work a little differently. Instead of a specific clause just for suicide, they usually have an initial waiting period of one or two years for death by any cause.

So, if the policyholder dies from any natural cause, an accident, or suicide within this initial period, the full payout won't be made. What happens instead is the insurer simply refunds all the premiums paid up to that point. Once this one or two-year period is over, the policy pays out the full sum assured for death by any cause, and that includes suicide.

Making sense of these different structures can feel complicated, and our guide comparing whole life vs term insurance is a great resource for clarifying some of the key differences.

Suicide Clause Comparison Across UK Policy Types

To make things clearer, let’s break down how the suicide clause typically works across the most common types of life insurance in the UK. This table gives you a quick snapshot of what to expect from each.

| Policy Type | Typical Suicide Clause | Key Considerations |

|---|---|---|

| Term Life Insurance | Standard 12-24 month exclusion period. | This is the most common personal policy. The waiting period is a standard feature. |

| Whole of Life Insurance | Standard 12-24 month exclusion period. | Similar to term insurance, personal whole of life plans have the same exclusion. |

| Death in Service | Usually no suicide clause. | A huge benefit of employer-provided schemes. The policy typically pays from day one. |

| Over 50s Plans | No specific suicide clause, but a 1-2 year waiting period for any cause of death. | If death occurs during the waiting period, premiums are refunded instead of a full payout. |

As you can see, knowing whether your protection comes from a personal plan, your employer, or a specialised Over 50s policy is vital. It’s the only way to be certain about the cover you have in place.

Final Thoughts and Where to Find Support

Trying to get your head around the ins and outs of life insurance and suicide can be a lot to take in. But getting to grips with what your policy actually says is a crucial step towards giving your family peace of mind for the future.

The main thing to remember is this: most UK life insurance policies do pay out for suicide, but only after an initial waiting period has passed. This is usually 12 months. On top of that, being completely upfront about your mental health history when you is non-negotiable. Think of that honesty as the foundation for your family's financial security; holding anything back could unfortunately void the policy down the line.

Seeking Help and Support

If you or someone you know is going through a tough time, it's so important to know that help is out there. Reaching out is a real sign of strength, and there are some brilliant organisations ready to listen without any judgement at all.

We can't recommend enough getting in touch with trained professionals who offer confidential help. These services are free to use and available around the clock.

- Samaritans: You can ring them anytime for a confidential chat on 116 123.

- Mind: A fantastic resource for advice and support for anyone dealing with a mental health problem.

- Campaign Against Living Miserably (CALM): They run a helpline and webchat from 5pm to midnight, every single day.

Making a properly informed decision about your insurance is vital. Our goal here is simply to give you the clarity you need to find the right cover for your situation and protect the people you love most.

Ready to get your family’s financial future sorted? You can get a personalised life insurance quote in just a few minutes, or have a chat with one of our friendly advisers for a bit of guidance.

Frequently Asked Questions

When you're trying to get your head around life insurance, it’s completely normal to have a lot of questions, especially about a topic as sensitive as this. We get asked these all the time, so here are some straightforward answers.

Can I Get Life Insurance with Mental Health Issues?

Yes, absolutely. Having a history of mental health conditions like depression or anxiety doesn't automatically mean you can't get life insurance here in the UK.

The most important thing is to be upfront and honest about your medical history when you . Insurers will take a look at your specific situation—your diagnosis, what treatment you've had, and how well your condition is being managed. It might affect your premiums, but it rarely means an outright 'no'.

What if a Coroner's Verdict Is Unclear?

This is a really good question. Sometimes, a coroner's verdict comes back as 'open' or inconclusive, meaning the exact cause of death isn't certain. When this happens, the life insurance company will do its own digging to make a decision on the claim.

They'll look at the case on the ‘balance of probabilities’. This means they'll use evidence from medical records and police reports to figure out if the death was likely a suicide. Whether they pay out then depends on what they find and, crucially, whether the death happened after the policy's suicide exclusion period had passed. For anyone trying to support someone through profound mental health struggles, you might find some helpful guidance on how to help someone self-harming here.

Are Premiums Refunded for a Denied Suicide Claim?

If a claim is turned down because a death by suicide happened during that initial exclusion period (usually the first 12-24 months), the good news is that most UK insurers will refund all the premiums that have been paid. This means the family or beneficiaries at least get back the money that was put into the policy.

But, it's not a hard and fast rule across the board. The best thing to do is always check the specific terms and conditions tucked away in your policy documents. That's the only way to be 100% sure of what your insurer's process is.

Ready to find the right protection for your family, without any of the confusing jargon? At Discount Life Cover, our expert advisers are here to help you compare your options and really understand the details. Get your free, no-obligation quote today and take that first important step towards securing your family’s future.

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply