When you're faced with making a life insurance claim, it usually boils down to three key things: letting the insurer know what's happened, getting hold of a certified death certificate, and filling out their claim form. It all starts with tracking down the policy documents to make sure you're the person who is supposed to receive the payout.

Your First Steps After Losing a Loved One

Coming to terms with the loss of a loved one is one of life's toughest challenges, and the last thing you want to deal with is a mountain of paperwork. The first few days are for grieving, but taking a couple of practical steps early on can make claiming the life insurance a whole lot less stressful down the line.

The single most important document you'll need is the official death certificate. Think of it as the key that starts the whole claims process. In England and Wales, you generally need to register the death within five days (it's eight in Scotland). It’s a good idea to ask for several official copies straight away. You’ll be surprised how many different organisations, not just the insurer, will need to see one.

Locating the Policy Documents

With the death certificate sorted, your next job is to find the actual life insurance policy. This can sometimes feel like a treasure hunt. The best place to start is with your loved one's important papers – check filing cabinets, desk drawers, or a home safe.

Don't panic if the paperwork is nowhere to be found. A good workaround is to check their bank statements for regular payments to an insurance company. Look for names like Aviva, Legal & General, or Vitality. This is often the clearest clue you'll get. Once you know which company it is, their claims department can usually find the policy with just the deceased’s full name, date of birth, and address.

The most important thing to remember is that you don't need to have all the answers at once. Take it one step at a time. The first move is simply to confirm a policy exists and who the provider is.

Making the Initial Contact

Once you've got the policy information and the death certificate, it's time to get in touch with the insurer. When you call, have this information ready:

- The policy number.

- The full name of the person who has passed away.

- Your name, contact details, and your relationship to them.

This first conversation is really just to let them know about the death and kick things off. They’ll then tell you exactly which forms and other documents they need from you. Of course, alongside these administrative tasks, looking after yourself is what matters most. In these difficult moments, small gestures can mean a lot; discovering meaningful sympathy gifts for loss can offer a little comfort and show you're thinking of others who are also grieving.

Gathering the Essential Claim Paperwork

After you've made that first difficult call, the insurer will send over a claim form along with a list of the documents they need. It's easy to look at this as just another bit of admin, but getting all the paperwork right from the very beginning is the single best way to ensure the claim goes through smoothly.

Think of it as building a watertight case for the claims assessor—one that leaves no room for doubt or delay.

The absolute cornerstone of any claim is the original death certificate. You might be able to use a certified copy, but the original is always best. This is the non-negotiable proof the insurer needs, which is why it's a smart move to order several copies when you register the death. You'll be surprised how many organisations ask for one.

You’ll also need to tackle the claim form itself. Fill it out with care, leaving no blank spaces or vague answers. Anything that isn't crystal clear will almost certainly result in the forms being sent back, adding frustrating delays to the process.

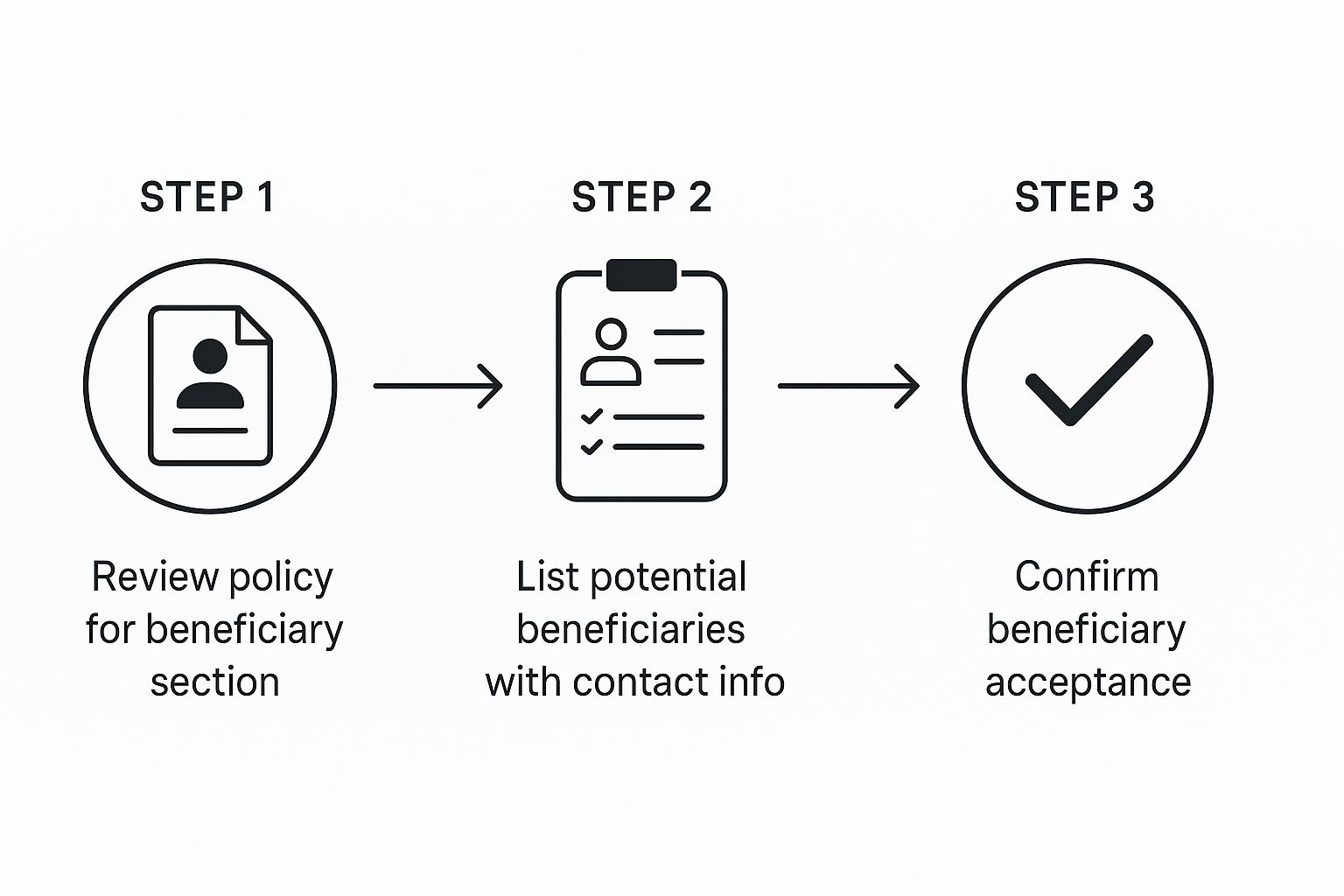

Beneficiary vs. Executor: Who Signs the Forms?

This is a really common question, and it can cause a bit of confusion. The answer all comes down to who is legally entitled to the policy payout.

The Beneficiary: If a specific person (or several people) is named as the beneficiary on the policy documents, they are the ones who need to complete and sign the claim forms. The money will then be paid directly to them.

The Executor: If there isn't a named beneficiary, or if the policy is set up to pay into the deceased's estate, then the executor of the will steps in. It's their responsibility to make the claim. In this case, the payout becomes part of the estate and is distributed as outlined in the will.

This infographic breaks down the initial steps to figure out who the beneficiaries are.

As you can see, the first port of call is always the policy document itself to identify who is formally named before you do anything else.

To help you stay organised, here's a quick checklist of the core documents you'll almost certainly need.

Essential Documents for a Life Insurance Claim

| Document | Purpose | Where to Obtain It |

|---|---|---|

| Original Death Certificate | Provides official proof of death to the insurer. | The local register office where the death was registered. |

| Completed Claim Form | The insurer's official form for initiating the claim process. | Provided by the life insurance company after initial contact. |

| The Original Policy Document | Confirms the details of the life insurance cover, including the sum assured and named beneficiaries. | Should be with the deceased's personal papers. If lost, the insurer can provide a copy. |

| Proof of Identity (Claimant) | Verifies the identity of the person making the claim (e.g., passport, driving licence). | Personal documents of the claimant. |

| Grant of Probate (if applicable) | Legally confirms the executor's authority to manage the deceased's estate. | Obtained by ing to the Probate Registry. |

Having these ready to go will make a huge difference to how quickly and easily the claim is processed.

When Probate Becomes Necessary

If the policy payout is directed to the estate, the insurance company will almost certainly ask for a grant of probate. This is the official legal document that gives the executor the authority to deal with the deceased's assets.

Be warned: getting probate isn't a quick process. It can easily take several months, which is a major factor in the overall claim timeline.

One of the most effective ways to avoid the delays and complexities of probate is to place the life insurance policy into a trust. A trust legally separates the policy from the person's estate, allowing the payout to go directly and quickly to the beneficiaries.

It’s a surprisingly straightforward step that can save your loved ones a huge amount of time and stress down the line. If you want to get into the details, you can read our comprehensive guide on putting life insurance in trust. It explains exactly how this simple legal wrapper can make all the difference when it’s time to claim.

Finally, pull together any other supporting documents they might ask for, such as the deceased's birth or marriage certificate, which help confirm identities and relationships. Having everything organised in one place before you send it off just makes the claims assessor's job easier, which is exactly what you want.

What Happens During the Claims Process

Once you've sent off the claim form and all the supporting paperwork, it can feel like you’re stuck in a waiting game. But your file doesn't just sit in a queue. Knowing what’s happening behind the scenes can really help manage expectations and reduce some of the anxiety during this time.

Your submission lands on the desk of a claims assessor. Think of them as the key decision-maker. It's their job to methodically review every detail you've provided to make sure the claim is valid and lines up with the policy's terms and conditions.

The assessor will carefully check that everything is present and correct. They'll verify the death certificate, confirm the policyholder's identity, and make sure the claimant is the rightful beneficiary named in the policy.

Realistic Timelines for Payouts

The big question on everyone's mind is, "how long will this take?" The good news is that most claims in the UK are pretty straightforward. If all the paperwork is in order and the circumstances are clear, many insurers will get the money paid out within one to two months.

Of course, some situations just take more time. Insurers have a duty to all their policyholders to ensure every claim is genuine, which sometimes means they need to dig a little deeper.

- Policies in their infancy: If a claim is made within the first one or two years of the policy starting (known as the contestability period), insurers will almost always take a closer look.

- Unclear cause of death: If the cause of death isn't immediately clear or is waiting on a coroner's report, the process will naturally be paused until that official information is available.

- Requesting third-party info: The assessor might need to get medical records from the deceased’s GP to verify the information given on the original application form.

These extra checks are just standard procedure. They aren't a sign that there's a problem with your claim – it’s simply the insurer carrying out its due diligence.

Why Do Insurers Investigate Some Claims?

That "contestability period" I mentioned is a standard feature in most life insurance policies. It gives the insurer the right to investigate a claim more thoroughly if the death happens shortly after the policy was taken out.

The main reason for this is to check for non-disclosure. This is where the policyholder might have unintentionally (or deliberately) left out important information on their application, like a pre-existing medical condition or the fact they were a smoker. If significant non-disclosure is found, it can unfortunately affect the claim's validity.

Despite these checks, it’s crucial to remember that the UK insurance industry has an exceptionally high payout rate. Insurers are in the business of paying valid claims, not finding reasons to reject them.

For example, in 2024, VitalityLife paid out £142 million in claims, honouring an impressive 98.9% of Life Cover claims. Figures like this highlight the reliability of UK insurers and should provide some reassurance that the system works for the vast majority of families. You can read more about their latest claims statistics on their site.

The key is to be patient and responsive. If the claims assessor gets in touch asking for more information, providing it promptly is the best thing you can do to keep the process moving forward.

Navigating Potential Claim Delays or Denials

While the vast majority of life insurance claims in the UK are paid without any drama, it’s smart to understand what can cause a delay or, in very rare cases, a denial.

Knowing the potential hurdles isn’t about causing worry. It's about empowering you with the right knowledge to make sure the process is as smooth as possible for your family.

The single biggest reason a claim gets scrutinised is something called non-disclosure. In simple terms, this just means information on the original application was inaccurate or incomplete.

The Impact of Non-Disclosure

Non-disclosure can be completely accidental. Someone might forget about a minor medical consultation from years back, or maybe they downplay their smoking habit, calling themselves a 'social smoker' when they were actually more regular than that.

Even these small, seemingly insignificant details can have big consequences down the line.

If an insurer is processing a claim and discovers information that contradicts what was on the application, they’ll dig deeper. This can cause delays while they chase up GP records or, in the worst-case scenario, lead to a smaller payout or even a complete rejection of the claim.

The insurer's decision usually comes down to one question: would the hidden information have changed their original underwriting decision? In other words, would they have still offered cover, or maybe charged a higher premium for it?

The key takeaway is simple: honesty and thoroughness when you first are everything. An accurate application is the best guarantee you can give your loved ones of a straightforward payout when they need it most.

When a Claim Doesn't Meet the Policy Definition

Another reason a claim might be rejected is that the situation simply doesn't match the specific terms and conditions of the policy. This is especially true for policies that have added benefits, like critical illness cover.

Every policy has a precise list of medical conditions it covers and, crucially, the level of severity required for a valid claim.

Statistical data from Aviva shows that while claim declines are low, they do happen. Of the small percentage of claims refused, the main reasons were non-disclosure (2.4%) or not meeting the specific policy definitions (5.8%). This really highlights just how vital it is to understand exactly what you're covered for. You can find more detail in Aviva's individual protection claims report.

Similarly, certain exclusions can lead to a denial, like death due to suicide within the first 12-24 months of taking out the policy. You can get to grips with the specifics by reading our guide on whether life insurance pays for suicide, which explains the clauses insurers typically include.

What to Do If Your Claim Is Unfairly Denied

If you genuinely believe a claim has been unfairly delayed or denied, you have clear rights and a path to follow, overseen by the Financial Conduct Authority (FCA).

The first port of call is always the insurer's formal complaints procedure. Lay out your case clearly and provide any evidence you have to back it up.

If you go through that entire process and still aren't happy with the final decision, you can take your complaint to the Financial Ombudsman Service. This is an independent body set up to resolve disputes between consumers and financial companies in the UK. Their service is free to use, and their decision is binding on the insurance company.

Understanding the Payout Process

Once the insurer gives the claim the green light, the final step is getting the money. This is obviously the most critical stage, and knowing what to expect can really help you plan ahead during what is an incredibly tough time. The process itself is usually straightforward, but one key detail can make a massive difference to how quickly the funds actually land in the beneficiaries' bank accounts.

In most situations, the life insurance payout arrives as a single, tax-free lump sum. This cash is designed to provide immediate financial relief, whether that’s to sort out funeral costs, clear the mortgage, or just replace the income of a loved one who's no longer around.

But the speed of this final step all comes down to one crucial thing: whether the policy was written 'in trust'.

The Vital Role of a Trust

A trust is just a simple legal wrapper that keeps the life insurance policy separate from the deceased's estate. You can think of it as a protective bubble around the payout.

When a policy is safely inside a trust, the insurer pays the money straight to the people named as trustees. They then pass it on to the beneficiaries. This simple setup has some huge advantages:

- Speed: The payout completely sidesteps the long and often complicated probate process.

- Tax Efficiency: The money isn't seen as part of the estate, which means it isn't liable for Inheritance Tax.

- Control: The policyholder’s wishes are followed to the letter, making sure the right people get the money without any fuss or delay.

What this means in the real world is that beneficiaries often get the funds within just a few weeks of the claim being approved, giving them financial stability when they need it most.

What Happens Without a Trust

Now, if a policy isn't in trust, things get a bit more complicated. The payout is made directly to the deceased person's legal estate. The money essentially gets lumped in with everything else they owned, from their house to their savings.

This is where you can run into some serious delays. Before a penny can be handed out, the executor of the will needs to get a 'grant of probate'. Our 2023 guide to probate dives into this legal maze in more detail, but the main thing to know is that it can easily take several months, sometimes even longer. All the while, the life insurance money is locked away, completely out of reach.

Putting a policy in trust is one of the smartest moves a policyholder can make. It ensures the payout steers clear of the messy business of estate administration, delivering faster access to the money and keeping it safe from Inheritance Tax.

Managing the Payout

Receiving a large sum of money, especially when you're grieving, can feel pretty overwhelming. It's often a good idea to just take a breath and not rush into any big financial decisions.

This is where getting some professional guidance from an independent financial adviser can be worth its weight in gold. They can offer impartial advice on the best way to manage the funds to support your family's future, whether that means investing, saving, or paying off debts. Having that expert support can bring some much-needed clarity and confidence as you figure out the path forward.

Frequently Asked Questions About Life Insurance Claims

When you're dealing with a life insurance claim, it's natural to have questions. It's an emotional time, and the process can seem daunting. Here are clear answers to some of the most common queries we hear from clients.

How Long Does a Life Insurance Claim Take in the UK?

For most straightforward UK claims where all paperwork is in order, you can expect the payout within one to two months. This is common for policies that have been running for a few years with a clear cause of death. However, claims can take longer if the death occurs within the policy's first two years (the 'contestability period') or if a coroner's investigation is required, as the insurer will need to conduct a more detailed review.

What If I Cannot Find the Life Insurance Policy Documents?

Don't panic. First, check the deceased’s bank statements for regular payments to insurers like Aviva, Legal & General, or LV=. Once you identify the insurer, their claims department can usually locate the policy using the person's name, date of birth, and address. If that doesn't work, services like the Unclaimed Assets Register can search for policies, though they do charge a fee.

Is the Life Insurance Payout Taxable in the UK?

No, the lump sum payout from a UK life insurance policy is typically paid free of income tax and capital gains tax. However, the payout may be subject to Inheritance Tax (IHT) if the policy was not written in trust. If the payout is made to the deceased's estate and the total value exceeds the IHT threshold (£325,000 in 2024/25), the amount over this limit could be taxed at 40%. Placing a policy in trust keeps the payout separate from the estate, shielding it from IHT.

Get Support With Your Life Insurance Needs

Navigating a life insurance claim is often just one part of a difficult and emotional journey. We've outlined the key steps for how to claim life insurance, from gathering the initial paperwork to understanding the final payout. The key takeaways are to act quickly, keep communication open with the insurer, and recognise the significant benefits of having a policy written in trust.

Whether you are currently managing a claim or planning for your family's future, being prepared is vital. Taking a moment now to review an existing policy or arrange a new one is one of the most valuable steps you can take for your loved ones. It ensures that when the time comes, the process is as smooth and straightforward as possible.

At Discount Life Cover, our goal is to make finding the right protection simple. You can compare quotes from the UK's top insurers in minutes and secure peace of mind.

Get your free, no-obligation quote today at https://discountlifecover.co.uk.

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply