It's one of the most difficult questions we're asked, but an important one: does life insurance cover suicide? The simple answer is yes, it usually does. However, there's a crucial detail every policyholder needs to understand, known as the 'suicide clause'.

Think of this clause as an initial waiting period. If a death from suicide occurs within the first 12 months of the policy starting, the insurer will almost certainly not pay out the full life insurance benefit. This guide explains how this works in the UK market.

Understanding Suicide Cover in UK Life Insurance

When you're trying to get your head around this sensitive topic, the suicide clause is the most important part to understand. It isn't there to be cruel or to pass judgement. It’s a necessary protection for insurance companies, regulated by bodies like the Financial Conduct Authority (FCA).

Without it, there's a risk that someone could take out a large policy with the intention of ending their life to leave a large payout for their family. The clause helps to keep the entire insurance system fair and sustainable for all policyholders.

After that initial 12-month period is over, a claim for suicide is treated just like any other claim, and the full cover amount is paid out to the beneficiaries. It’s a standard feature you’ll find in almost every UK life insurance policy. For more detail, you can read about how insurance policies handle suicide claims on iaminsured.co.uk.

The First Year Exclusion Period

Those first 12 months are absolutely key. This is when the suicide clause is in effect. If a claim is made during this window, the insurer will investigate the cause of death. If it's confirmed as suicide, the claim for the main payout will be denied.

However, this doesn't mean the insurer keeps all the money. In nearly all cases, they will refund the premiums that have been paid up to that point. So, while the large sum assured isn’t paid, your family won't be left out of pocket for the monthly payments.

This waiting period is standard practice across the UK insurance industry, from large insurers like Aviva and Legal & General to smaller, more specialist firms. It applies to the most common types of cover people buy, like level term and decreasing term life insurance, which are popular for protecting mortgages and young families.

For example, a parent in their 30s taking out a level term policy to protect their children would be subject to this 12-month clause. If they were to die by suicide after 13 months, their family would receive the full payout.

UK Life Insurance Suicide Clause At a Glance

The table below gives a simple overview of how a UK insurer will likely respond to a claim related to suicide, based on how long the policy has been active.

| Time of Death | Claim Outcome | Reason |

|---|---|---|

| Within the first 12 months | Claim denied, premiums refunded | The suicide clause is active, preventing a payout but ensuring premiums are returned. |

| After the first 12 months | Full payout is approved | The suicide clause has expired. The claim is treated like any other cause of death. |

This distinction is the cornerstone of how the industry handles such a sensitive issue. Once that initial year has passed, the policy is designed to provide the financial protection your family was promised, regardless of the circumstances.

Understanding the Suicide Clause in Your Policy

It’s one of the most sensitive topics in life insurance, but one that must be understood. The suicide clause is a standard feature in almost every life insurance policy you'll find in the UK. Think of it as a probationary period when your cover first starts.

Its purpose is straightforward: to prevent insurance fraud. Insurers have to protect their entire pool of policyholders from the rare but serious risk of someone taking out a large policy with the immediate intention of their family claiming on it. This safeguard keeps the system fair and helps keep premiums affordable for everyone.

How Long Does the Clause Last?

For the vast majority of UK providers, including major insurers like Aviva and Legal & General, the suicide clause lasts for 12 months. This countdown starts from your policy's official start date—the day your cover formally begins.

This isn't a penalty; it's simply standard industry practice. Once that first year is over, a death by suicide is typically treated no differently to any other cause of death, meaning the full claim amount would be paid to your beneficiaries.

It’s also crucial to know that this 12-month clock can reset. If you miss premium payments and your policy lapses, you might need to go through underwriting again to have it reinstated. If that happens, the suicide clause period usually starts again from the new reinstatement date.

The suicide clause isn’t designed to penalise families going through an unimaginable tragedy. It's a necessary measure to protect the integrity of the insurance system, ensuring claims are paid for unforeseen events—which is the fundamental reason insurance exists.

What Happens if a Claim is Made During This Period?

If the insured person dies by suicide within the first 12 months of the policy, the insurer won't pay out the main death benefit. However, that doesn't mean your family is left with nothing.

In almost all cases, the insurer will refund 100% of the premiums that have been paid into the policy up to that point. This ensures that the money you’ve put in is returned to your estate or beneficiaries, even though the full cover amount isn't paid out.

Getting your head around the suicide clause in the UK is essential for understanding how your policy works in these difficult situations. Once you see it for what it is—a standard, logical part of life cover—it's far less intimidating than it sounds.

How Mental Health History Affects Your Application

Applying for life insurance when you've dealt with mental health conditions can feel daunting. It’s natural to worry that a history of something like depression or anxiety might mean an automatic "no," but that’s rarely the case. Thankfully, UK insurers have come a long way and now look at every application on a case-by-case basis.

The key is to be prepared for the underwriting process. This is simply the insurer's way of getting to know you and evaluating risk, and they'll ask specific questions about your mental health to get a full picture of your overall wellbeing.

What Insurers Need to Know

When you fill out your application form, expect some questions about your mental health. This is a standard part of the process, no different from them asking about physical conditions like high blood pressure or diabetes.

You'll likely be asked about things like:

- Specific Diagnoses: Have you ever been diagnosed with a condition like depression, anxiety, bipolar disorder, or PTSD?

- Treatment History: Have you received any treatment, whether that's medication, counselling, or other therapies?

- Severity and Timeframes: When were you diagnosed, how long did your symptoms last, and have you had any recent episodes?

- Hospital Stays: Have you ever needed to stay in hospital because of your mental health?

- Suicide Attempts or Ideation: Have you ever attempted suicide or had suicidal thoughts?

Answering these questions openly is absolutely crucial. Remember, the insurer isn't there to judge you. They just need to accurately assess the level of risk so they can offer you the right policy on the right terms.

The Critical Importance of Honesty

It can be tempting to skim over details or even leave out parts of your mental health history, but that would be a huge mistake. Failing to disclose everything is known as non-disclosure, and the consequences can be devastating.

If you were to pass away and the insurer later discovered you'd withheld important information, they could legally cancel the policy and refuse to pay the claim. This would mean your loved ones are left without the financial safety net you worked so hard to put in place. When it comes to insurance, honesty really is the only policy.

The link between mental health and life insurance is undeniable. In fact, suicide is a leading reason for life insurance claims among men in their 20s and 30s, making up around 30% of claims in this age group. This stark statistic is exactly why insurers pay such close attention to mental health disclosures. Anyone with a history of suicide attempts will find their application reviewed very carefully. You can see more on these claim statistics and insurer policies at legalandgeneral.com.

Trying to find cover with a complex health history can feel like a minefield, but you don't have to navigate it alone. Specialist brokers know the market inside and out and have helped countless people with different conditions find the cover they need. You can find some great guidance on getting life insurance with pre-existing medical conditions to see what your options are. At the end of the day, a past or present mental health condition shouldn't stop you from securing your family’s future.

Comparing How Different Policies Treat Suicide

Not all life insurance policies are the same, and the way they handle claims related to suicide can vary. Understanding these differences is vital if you want to pick the right cover for your family. While the 12-month suicide clause is standard across the board, how it's applied—and whether other waiting periods are in play—depends on the type of product you choose.

Let's break down some of the most common types of cover you'll find in the UK and see how each one approaches this sensitive issue.

Term Life Insurance Policies

Term life insurance is the most common type of protection in the UK. This includes both Level Term and Decreasing Term policies, and they're designed to do one simple thing: pay out a lump sum if you pass away within a set period.

For these policies, the 12-month suicide clause is almost always in effect. If the policyholder dies by suicide within that first year, the insurer will almost certainly decline the claim. However, they will refund all the premiums that have been paid. Once that first year is up, a death by suicide is generally treated like any other cause of death, and the full payout is made to the beneficiaries.

Over 50s Life Insurance Plans

Over 50s plans are a different type of policy. They offer competitive acceptance to UK residents aged 50-85, with no medical questions. Because the insurer is taking on a lot of unknown risk, these policies come with a broader waiting period.

Here’s what you need to know:

- General Waiting Period: Most Over 50s plans have a waiting period of 12 to 24 months for death from any cause. If you die from natural causes during this initial window, the insurer won’t pay the full sum but will refund the premiums you've paid in.

- Accidental Death: The main exception is usually accidental death, which is typically covered from day one.

- Suicide: Because of this general waiting period, a death by suicide within the first one or two years wouldn't lead to a full payout, although the premiums would be returned. After the waiting period ends, the policy pays out the full cash sum, regardless of how the death occurred.

Critical Illness Cover

It's also important to understand where Critical Illness Cover fits in. This is often added onto a life insurance policy and is designed to pay out if you're diagnosed with a specific serious illness, like cancer or a heart attack.

Critical Illness Cover is for surviving a specified medical diagnosis, not for death. A claim resulting from suicide or a self-inflicted injury would not be covered under the critical illness part of a policy, as it simply doesn't meet the definition of a qualifying illness.

Suicide Cover Across Different UK Insurance Policies

To make it clearer, here’s a quick comparison of how the suicide clause and general death benefit rules to different types of UK life insurance.

| Policy Type | Typical Suicide Clause | Key Considerations |

|---|---|---|

| Term Life Insurance | 12-month exclusion period. Premiums are refunded if death occurs within this time. | After the first year, suicide is typically covered in full. |

| Whole of Life Insurance | Similar to term cover, with a standard 12-month exclusion period. | As it provides lifetime cover, the clause only applies to the first year of the policy. |

| Over 50s Plans | Covered by a general waiting period of 12-24 months for most causes of death. | The waiting period isn't specific to suicide but applies to nearly all causes except accidental death. |

| Critical Illness Cover | Not applicable. This cover is for diagnosis of specific illnesses, not death. | Self-inflicted injuries are explicitly excluded from claims. |

This table shows that while the 12-month suicide clause is a common thread, you must look at the overall policy structure—especially with products like Over 50s plans—to understand the full picture.

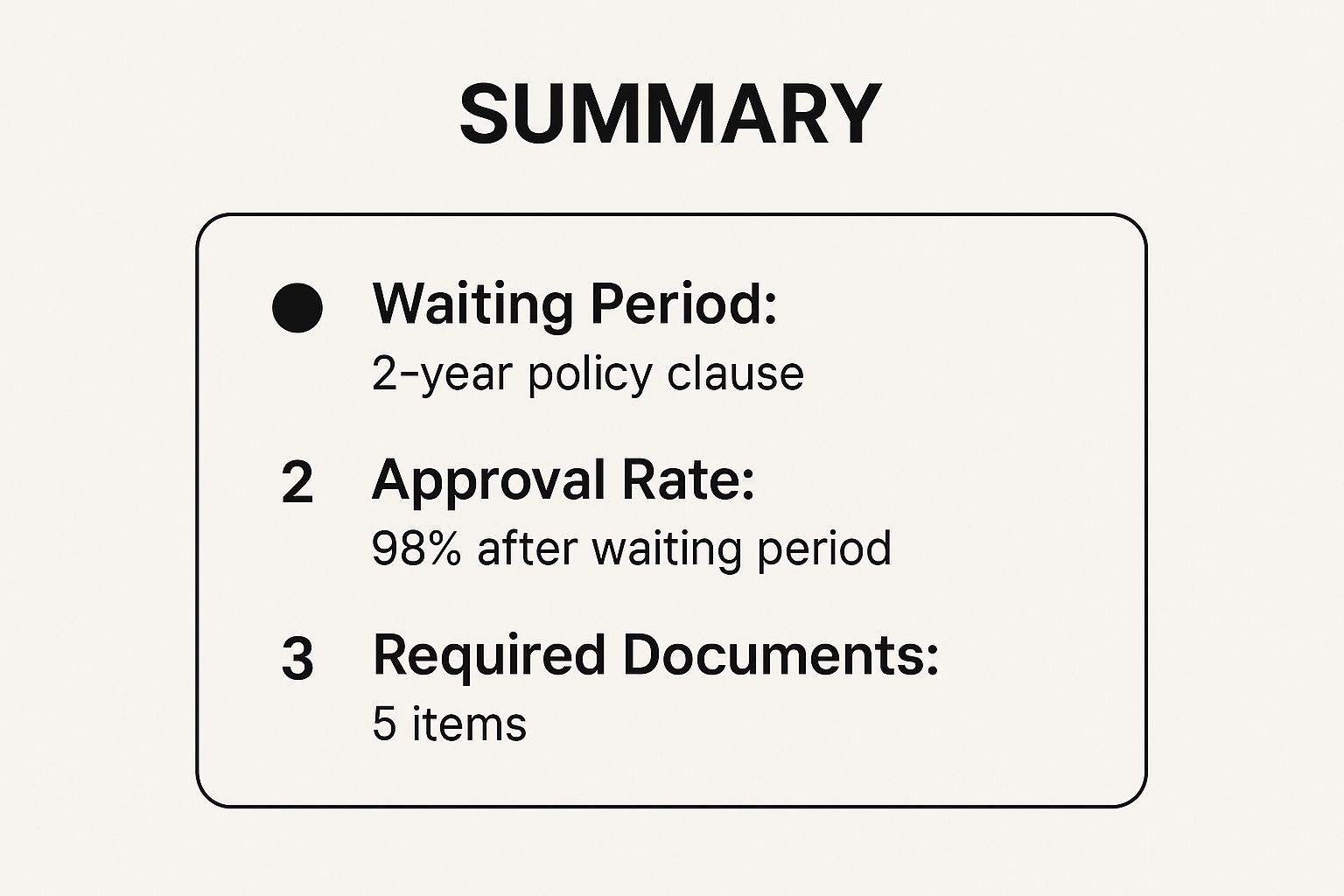

This infographic summarises the key elements an insurer looks at when processing a sensitive claim after any initial exclusion period has passed.

The data highlights that once you're past the initial exclusion periods laid out in the policy, the approval rate for claims is extremely high, as long as all the correct documentation is provided.

What to Expect During the Claims Process

For the family left behind, making a life insurance claim after a suicide is an incredibly tough and emotionally draining time. Knowing what to expect from the process can help set expectations and make things run as smoothly as possible. At the end of the day, the insurer's job is to check the claim against the policy's terms and conditions.

When a claim is submitted, especially one involving a suicide, the insurer has to launch a full investigation. This isn't about distrust; it's standard procedure to ensure all the facts are straight. The first thing a beneficiary needs to do is let the insurer know what's happened and provide a copy of the death certificate.

The Insurer's Investigation

The claims team needs to verify two key things: the official cause of death and the exact date it happened. This is to confirm whether the death occurred inside or outside of that initial 12-month suicide clause period.

To get this confirmation, they'll usually ask for a few documents:

- The original policy documents to check the specific terms of the cover.

- A claimant’s statement, which details their relationship to the person who has passed away.

- The official death certificate, as this states the cause of death.

- A coroner’s or police report to give them more detail on the circumstances.

Insurers also have the right to look at the deceased's medical history, which they'll compare against the information given on the original application form. What they're looking for here is any evidence of non-disclosure – particularly around any pre-existing mental health conditions that weren't mentioned when the policy was first set up.

Managing Timelines and Expectations

It’s important to be prepared for these sensitive claims to take a bit longer to process than more straightforward ones. Waiting for reports from coroners and doctors can naturally cause delays. Our guide on how long life insurance takes to pay out in the UK gives more detail on typical timelines.

The reason for these thorough checks is partly down to national data. Suicide accounts for over 25% of non-medical deaths within some UK insurance portfolios. With ONS data showing around 5,500 suicides each year in England and Wales, you can see why insurers have rigorous procedures to verify the timing and cause of death.

The best thing you can do is provide all the information they ask for as quickly and accurately as you can. Keeping the lines of communication open with the insurer's claims department will help you stay in the loop and can prevent unnecessary hold-ups. The whole point is to give you a clear, supportive path so you know what's needed during an unimaginably difficult time.

Getting Help and Final Thoughts

Trying to understand the ins and outs of life insurance and mental health can feel like a massive task. But if there's one thing to take away, it's this: in the UK, life insurance policies generally do cover suicide.

The crucial detail is that the policy needs to have been active for more than the initial 12-month exclusion period. That’s why being completely upfront and honest about your mental health history when you is so important—it's the only way to be certain your family is properly protected.

Of course, some policies, like Over 50s plans, have slightly different rules, so always check the specific terms. But remember, having a past or present mental health condition should never be a barrier to securing your family's financial future.

Where to Find Support

If you or someone you know is going through a tough time, please know that help is available. Reaching out and talking to someone is a vital first step.

- Samaritans: You can call them for free, anytime, 24/7, on 116 123 or visit their website for support.

- Mind: This fantastic charity provides advice and support for anyone experiencing a mental health problem. You can reach their Infoline at 0300 123 3393.

For anyone wanting to gain a deeper insight into the complexities of suicidal ideation, there's a helpful article on understanding suicidal thoughts from a counsellor's perspective.

Protecting your loved ones is one of the most important financial decisions you'll ever make. Here at Discount Life Cover, we can help you find the right policy for your unique circumstances, whatever they may be.

Take the first step today. Get your free, no-obligation life insurance quote and give your family the peace of mind they deserve.

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Your Questions Answered (FAQ)

This is a sensitive topic, and it’s natural to have questions. Here are clear answers to some common queries about life insurance and suicide.

Will a history of depression make my premiums more expensive?

It can, but it's not a given. Insurers don't just see the word "depression" and automatically hike up the price. They look at the bigger picture of your mental health journey.

What they’re interested in is:

- The specifics of your experience: A single, mild episode that was treated years ago is very different from a recent, more severe diagnosis.

- How it's been managed: Showing a history of consistent treatment, like therapy or medication that has kept things stable, is a positive. It shows you're managing your health.

- How long since you've had symptoms: The more time that's passed since you last struggled with symptoms, the less it's likely to affect your premiums.

The best thing you can do is be completely open. Insurers are far more likely to offer you good terms if you give them a full and honest history. It allows them to assess the actual risk accurately.

What happens if the cause of death is unclear?

If the cause of death isn't immediately obvious and an investigation is needed, the life insurance claim is put on hold. The insurance company will wait for the official verdict before they proceed.

In these situations, a coroner's report is usually the key document. It establishes the official cause and date of death, but getting it can take several months, which unfortunately delays the payout. The insurer needs that report to confirm whether the death happened inside the policy's 12-month suicide exclusion period.

Can an insurer refuse a suicide claim after 12 months?

It’s incredibly rare for a UK insurer to reject a suicide claim once that initial 12-month period is over. After the first year, a death by suicide is generally handled just like any other cause of death.

The one major exception? If the insurer discovers there was non-disclosure on the original application. For example, if the person didn't mention a significant history of mental health struggles, previous suicide attempts, or related treatments when they took out the policy, the insurer could declare the policy void. The claim would be denied because the contract was agreed upon using incomplete or misleading information. Being honest from day one is the only way to be certain the policy will pay out when needed.

Ready to find the right protection for your family? The team at Discount Life Cover can help you compare policies from leading UK insurers to find cover that fits your needs and budget.

Get your free, no-obligation quote today and secure your family's future.

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply