Imagine having a financial safety net for your family that's competitive to be there, no matter what. That’s the simple idea behind whole of life cover. It's a type of life insurance designed to pay out a competitive lump sum whenever you pass away, as long as you’ve kept up with your payments. It provides permanent peace of mind.

What Is Whole of Life Cover and How Does It Work?

At its core, whole of life cover is a straightforward promise. You agree to pay a set amount each month—your premiums—and in return, your insurer guarantees to pay out a tax-free lump sum when you die. This payout is known as the 'sum assured'.

Think of it as a permanent financial umbrella for your family. Unlike other policies that close up after a certain number of years, this umbrella stays open for your entire life, ready to shield your loved ones from financial hardship when they need it most.

This is what makes it so different from its more common cousin, term life insurance. Term cover only protects you for a specific period, say 10, 20, or 30 years. If you outlive that policy, there’s no payout. With whole of life, the payout is a certainty, not a possibility.

The Purpose of Your Policy

The main reason people take out a whole of life policy is to provide a significant, tax-free sum of money to their beneficiaries—the people they choose to receive the money. This financial boost can be used for all sorts of things, easing the pressure on your family during an incredibly tough time.

Some common reasons for the payout include:

- Covering Funeral Costs: Funerals in the UK aren't cheap, and the cost can come as a real shock. A policy payout can cover these expenses completely, so your family doesn't have to worry about finding the money.

- Clearing Outstanding Debts: Any lingering personal loans, credit card balances, or other debts can be wiped clean without eating into your family’s savings.

- Leaving a Financial Legacy: Many people use whole of life cover to leave a competitive inheritance for their children or grandchildren, giving them a leg up with a house deposit, university fees, or just a financial head start in life.

- Inheritance Tax Planning: For those with larger estates, this type of policy is a really effective tool for Inheritance Tax (IHT) planning. We’ll get into the specifics of that a bit later.

Understanding the Premiums

Because the payout is competitive, the monthly premiums for whole of life cover are typically higher than for term insurance. You're paying for certainty. The cost simply reflects the fact that the insurer knows it will have to pay out eventually.

UK insurers calculate these premiums based on a few personal details, like your age, health, lifestyle (whether you smoke, for instance), and the amount of cover you want. Generally speaking, the younger and healthier you are when you take out the policy, the lower your premiums will be. You essentially lock in a better rate for life, which can be a very smart move if you're planning for your family's long-term financial security.

Getting to Grips with Your Policy's Features

While the basic idea of a competitive payout sounds simple enough, not all whole of life policies are cut from the same cloth. Getting familiar with the specific features is the key to picking a plan that actually fits your long-term financial picture and gives your family the right kind of security.

The absolute cornerstone of any policy is the competitive payout. It’s a straightforward contract: as long as you keep up with your premiums, the insurer will pay out the agreed-upon sum when you pass away. This rock-solid certainty is what makes it such a powerful tool for planning ahead.

Then you have the sum assured. This is the tax-free lump sum your family will get. You set this amount right at the start, thinking about what you want to leave behind. It could be enough to pay off the mortgage, handle a potential Inheritance Tax bill, or simply provide a comfortable legacy for your loved ones.

vs. Reviewable Premiums

One of the biggest decisions you'll make is about your premiums. Insurers in the UK usually offer two different ways of structuring them, and your choice will have a major impact on your budget down the line.

- Premiums: These are locked in for the life of the policy. What you pay on day one is exactly what you’ll pay decades from now. This gives you predictability and makes it much easier to budget for the long haul. No surprises.

- Reviewable Premiums: These start off but come with a catch. The insurer will review them at set times, maybe every five or ten years. After a review, your premiums could go up—sometimes by a lot—based on things like their overall risk assessment or even just you getting older.

So, you have a classic trade-off. premiums offer complete peace of mind, while reviewable premiums give you a lower starting cost but with a question mark hanging over the future. Most people find the certainty of competitive premiums is well worth it to avoid a nasty financial shock later in life.

Think of a policy with competitive premiums like fixing your mortgage rate for the entire term. You know exactly what’s coming out of your account each month, start to finish, protecting you from whatever the market or the insurer decides to do later on.

Investment-Linked Whole of Life Cover

If you’re comfortable with a bit more risk for the chance of a bigger reward, some whole of life cover policies can be linked to investments. You’ll often hear these called investment-linked or unit-linked plans.

Here’s how they work: a chunk of your premium is used to buy units in an investment fund. The final payout your family receives is then tied to how well those investments do. This brings both an opportunity and a risk to the table.

- Potential for Growth: If the funds perform well, the payout could end up being much larger than the original sum you were assured.

- Investment Risk: On the flip side, if the investments take a tumble, the payout could be lower. Insurers usually set a minimum competitive sum assured to provide a safety net, but any extra growth is never a sure thing.

These policies are definitely more complex and are best suited to someone with a healthy appetite for risk. They are regulated by the Financial Conduct Authority (FCA), which means the risks have to be spelled out clearly. Before you even think about an investment-linked option, you need to be completely comfortable with the fact that the final value isn’t fixed. For anyone who wants absolute certainty, a standard whole of life policy with a competitive sum and competitive premiums is the most straightforward and predictable choice.

A Smart Strategy for Inheritance Tax Planning

One of the cleverest ways to use whole of life cover in the UK is for tackling Inheritance Tax (IHT). Let's be honest, with house prices shooting up over the years, more and more families are finding themselves unexpectedly caught in the IHT net. It’s not just for the super-rich anymore. This is where a whole of life policy can be a real game-changer.

So, what is Inheritance Tax? It's a tax on the estate of someone who has passed away—that’s their property, money, and belongings all bundled together. If your estate's value tips over a certain amount (currently £325,000 per person), your loved ones could be hit with a hefty 40% tax bill on everything above that limit. That kind of bill can force families into heartbreaking decisions, like selling the family home just to pay HMRC.

The Office for Budget Responsibility has crunched the numbers and predicts IHT payments will climb to £9.8 billion by 2028-29. This is happening largely because soaring property values are pushing more ordinary estates over the tax-free line. It's this growing financial squeeze that has people looking for smart solutions like whole of life cover.

Using a Trust to Protect Your Payout

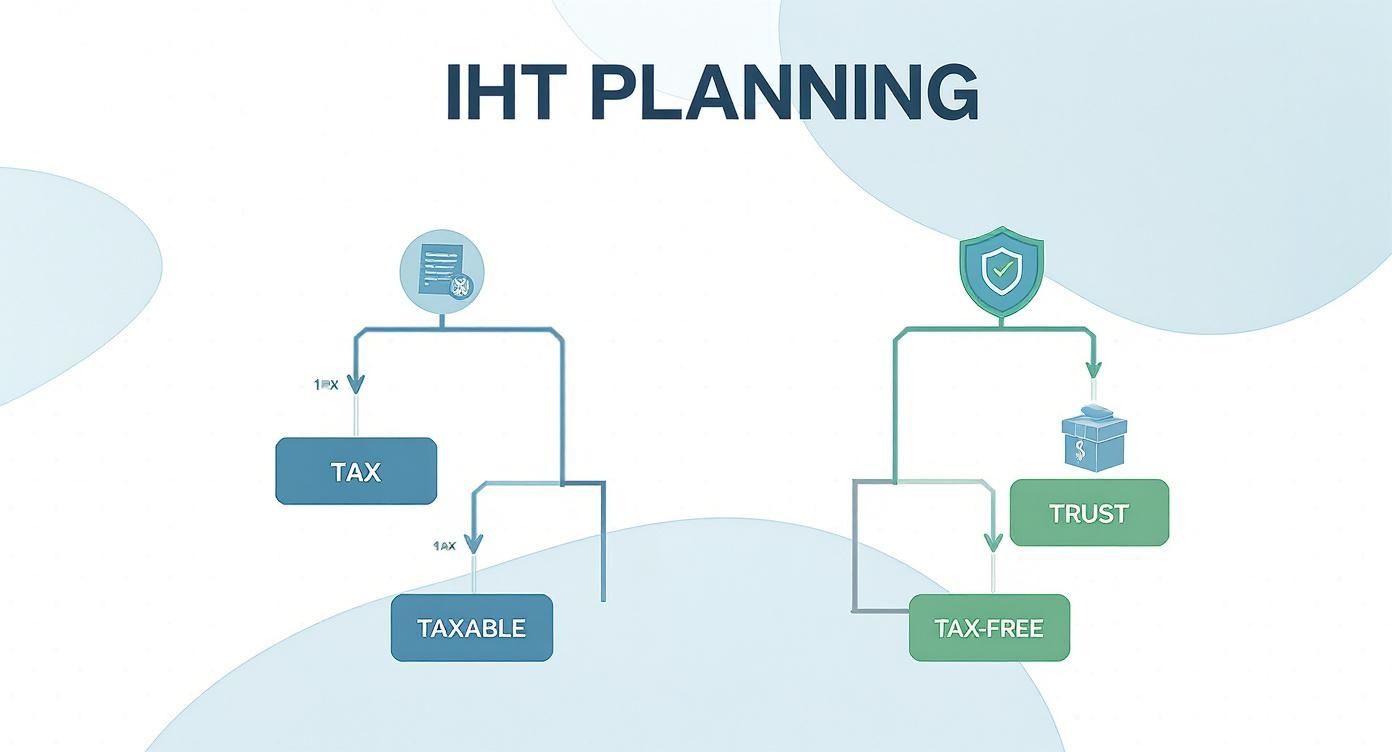

Now, just taking out a whole of life policy on its own won't solve your IHT problem. In fact, if the payout goes straight into your estate, it just makes the estate bigger and could actually increase the tax bill. The secret weapon here is putting your policy 'in trust'.

Think of a trust as a secure legal box. By placing your policy inside this box, you legally separate it from the rest of your estate. For tax purposes, it's no longer considered part of your assets.

When the policy eventually pays out, the money goes straight to the people you've appointed as trustees, who then pass it directly to your chosen beneficiaries. This simple but powerful step nails two crucial goals:

- It sidesteps Inheritance Tax: Because the payout never technically becomes part of your estate, it isn’t hit with that 40% IHT charge. Your family gets the full amount.

- It avoids probate: Probate is the official legal process of sorting out an estate, and it can drag on for months, sometimes even years. Money held in a trust is available much, much faster, getting funds to your family when they really need them.

We cover the nuts and bolts in more detail in our guide on what is Inheritance Tax.

A Real-World Example

Let's look at how this plays out in real life. Meet David and Sarah, homeowners in their late 50s with two grown-up children. Their total estate—including their home, savings, and investments—is worth £1.2 million.

Together, they have a tax-free allowance of £650,000. That leaves £550,000 of their estate exposed to a 40% IHT charge. The potential tax bill? A staggering £220,000.

To cover this, David and Sarah take out a joint whole of life policy for £220,000. And here's the crucial bit: they place the policy in trust, naming their children as the beneficiaries.

When they both pass away, the £220,000 from the policy is paid directly to their children, completely outside of the estate. They can then use this tax-free cash to settle the IHT bill, meaning they don't have to sell the family home or any other assets. The policy is transformed from a simple payout into a savvy estate planning tool. If you want to get a broader perspective, you can delve deeper into understanding inheritance tax with other expert resources.

By writing a whole of life policy in trust, you provide your beneficiaries with the exact funds needed to cover the tax liability, ensuring the assets you worked hard for pass to them intact.

Setting up a trust is usually a straightforward part of the application process. Your insurer or a financial adviser can sort it for you, often with no extra charge when you take out the policy. It’s one of the most effective ways to make sure your legacy is protected.

Comparing Your Life Insurance Options

Picking the right life insurance isn’t just ticking a box; it’s about making sure you get the policy that genuinely fits your family's future. To get it right, you need to see how whole of life cover stacks up against the other big players in the UK market. Each policy is a different tool for a different job.

Getting your head around these differences is the key to figuring out what’s best for you, whether you’re covering a mortgage, setting aside money for funeral costs, or building a legacy for your loved ones.

Whole of Life vs Term Life Insurance

The biggest difference between whole of life and term life insurance boils down to how long the cover lasts. A simple way to think about it is that term insurance is like renting protection for a set period, while whole of life is like owning it forever.

- Term Life Insurance: This covers you for a fixed number of years, maybe 20 or 30. If you pass away during that time, your family gets the payout. If you outlive the policy, the cover just stops, and that’s that. Because the payout isn't competitive, the premiums are much, much .

- Whole of Life Cover: This is lifelong protection. As long as you keep up with your premiums, a payout is competitive when you die, no matter when that is. This certainty means the premiums are naturally higher.

With term insurance, you’ll also come across two main flavours:

- Level Term: The payout amount stays the same from day one until the policy ends. It’s a great fit for covering an interest-only mortgage or leaving a specific lump sum for your family to rely on.

- Decreasing Term: Here, the payout amount shrinks over time, usually in step with a repayment mortgage. As your mortgage debt gets smaller, so does your cover, which makes it a more affordable way to protect your home.

We dive much deeper into this in our full comparison of whole of life vs term insurance.

Whole of Life vs Over 50s Plans

On the surface, Over 50s plans look a lot like whole of life cover. Both offer lifelong protection and a competitive payout. But dig a little deeper, and you’ll find they’re built for very different jobs and aimed at different people.

An Over 50s plan is technically a type of whole of life policy, but it has some crucial differences. The main one is that acceptance is usually competitive for UK residents between 50 and 80, with no medical questions asked. This makes them a lifeline for people with health issues who might be turned down for other types of cover.

But that easy access comes with a few trade-offs. The payout from an Over 50s plan is much smaller, often capped at around £20,000. They’re really designed to cover final expenses like a funeral or to leave a small cash gift. Standard whole of life cover, on the other hand, requires full medical underwriting and can provide massive payouts, making it the tool of choice for serious inheritance tax planning or leaving a substantial legacy.

To help you decide which path makes the most sense, let’s lay it all out in a simple table.

Whole of Life vs Term Life vs Over 50s Cover

| Feature | Whole of Life Cover | Term Life Insurance | Over 50s Plan |

|---|---|---|---|

| Cover Duration | Lifelong protection | Fixed period (e.g., 20-30 years) | Lifelong protection |

| Payout Guarantee | Guaranteed, whenever you pass away | Only if you pass away within the term | Guaranteed, whenever you pass away |

| Premiums | Higher | Lower | Moderate, but fixed |

| Medical Questions | Yes, full underwriting required | Yes, medical questions asked | No, acceptance is competitive |

| Sum Assured | High (can be millions) | Can be high, depending on needs | Low (typically under £20,000) |

| Best For… | Inheritance tax planning, legacy | Mortgage protection, family support | Funeral costs, small cash gifts |

As you can see, the right choice really comes down to what you’re trying to achieve and your personal circumstances. There's no single "best" option, only the one that best suits your goals.

As the infographic shows, putting your whole of life policy into a trust is a crucial step for inheritance tax planning. If you don't, the payout becomes part of your estate and can get hit with tax. A trust makes sure the full amount goes straight to your beneficiaries, tax-free.

Is Whole of Life Cover Right for You?

Figuring out if a certain type of life insurance is the right move means taking the theory and ing it to your own life. It’s about having an honest look at your personal situation, your family’s actual needs, and what you want to achieve in the long run.

A whole of life cover policy isn't for everyone, that’s for sure. But for some people, it’s an incredibly smart financial tool. To help you see if it fits, let’s walk through a few real-world scenarios where this kind of permanent cover really makes sense.

You Are Planning Your Estate

If you’ve built up significant assets—property, investments, or a healthy savings pot—you're probably thinking about the best way to pass them on. As we’ve mentioned, Inheritance Tax (IHT) can take a serious chunk out of your estate, leaving your loved ones with a lot less than you’d hoped.

This is exactly where whole of life cover steps in as a key part of your financial strategy.

- For High-Value Estates: If your estate is likely to be valued above the IHT threshold, a policy can provide a tax-free lump sum specifically to cover the tax bill. This is a game-changer, as it means your family won’t be forced to sell assets, like the family home, just to pay HMRC.

- For Business Owners: If you're a business owner, this type of policy can be crucial for succession planning. The payout provides the cash needed for a smooth handover, allowing your family or business partners to buy out your shares without causing financial chaos.

And the smartest move? Placing the policy in a trust. This ensures the money is paid out quickly and, crucially, it stays outside of your estate for tax purposes, making it a cornerstone of good legacy planning.

You Want to Leave a Legacy

Maybe your goal is a bit more straightforward: you simply want to leave a competitive financial gift to your children or grandchildren. While term insurance is great for covering temporary debts like a mortgage, it comes with no guarantee of a payout if you outlive the policy.

A whole of life policy, on the other hand, guarantees a sum of money will be there for them, no matter when you pass away. Think about what a head start in life that could provide.

This competitive inheritance can make a world of difference. It could be a deposit on a first home, funding for a university education without the shadow of student debt, or just a solid financial cushion for whatever the future holds. It's a final, powerful way to show you care.

This certainty makes it a popular choice for parents and grandparents who want to know for sure that their financial gift will be received. It’s less about protection and more about providing a lasting legacy.

You Have Lifelong Dependents

Some family situations involve financial support that doesn’t just stop after 20 or 30 years. If you're the main carer for a child with a disability or another loved one who will always rely on you financially, you need protection that lasts a lifetime.

In these circumstances, term insurance just doesn't cut it. The cover could run out long before the need for financial support does, which is a risk most people aren’t willing to take.

A whole of life policy offers the ultimate peace of mind. It ensures a dedicated fund will always be there to provide for your dependent's care and quality of life, long after you’re gone. Often, this is set up by placing the policy in a specialised trust, making sure the funds are managed properly for the beneficiary's welfare. For many, this is one of the single most compelling reasons to choose permanent life insurance.

Understanding the Cost of Your Premiums

When you for any kind of life insurance, insurers have a process they call 'underwriting'. It sounds a bit technical, but all it really means is that they're figuring out the level of risk involved in offering you cover, which in turn helps them set a fair price for your monthly premiums.

A few key factors come into play here, each one helping to build a complete picture of your personal circumstances. Getting your head around these is genuinely useful because it explains why quotes can look so different from one person to the next. It also shows you exactly how your personal details connect to the long-term cost of your whole of life cover.

Key Factors That Influence Your Premiums

At its heart, underwriting is all about an insurer trying to understand your life expectancy. Because a whole of life policy is competitive to pay out one day, this is the main driver of cost.

Here are the main things they'll look at:

- Your Age: This is probably the biggest one. The younger you are when you take out a policy, the your premiums will be. Simple as that. By getting cover sooner rather than later, you lock in a lower rate for life.

- Your Health: You’ll be asked some fairly detailed questions about your health, covering things like your height, weight, and any existing medical conditions. Insurers just need a clear, honest picture to assess the risk properly.

- Your Lifestyle: Habits such as smoking or regular heavy drinking will have a significant impact, pushing your premiums up. From an insurer's point of view, these are high-risk activities that can affect your long-term health.

- Your Family’s Medical History: You might also be asked about the health of your immediate family, like your parents or siblings. If there's a history of serious hereditary conditions, like certain cancers or heart disease, it can sometimes influence your premium.

vs Reviewable Premiums Revisited

As we mentioned earlier, the type of premium you choose makes a massive difference to how affordable the policy will be down the line. Reviewable premiums might look like a bargain to start with, but they can get much more expensive over time, potentially becoming unaffordable just when you need the cover most.

premiums offer complete peace of mind when it comes to budgeting. Your monthly payment is set in stone from day one and will never go up. This predictability is one of the standout benefits of a properly set-up whole of life policy.

The demand for this kind of permanent protection remains strong in the UK. The latest data from the Financial Conduct Authority shows that 452,799 pure protection contracts were sold in Q1 2025, with premiums for the quarter reaching a total of £13.85 billion. This confirms that while the average premium for whole of life cover is higher than for term insurance, many people clearly see the value in its lifelong guarantee.

Ultimately, by understanding what drives the cost, you can go into your application with a much clearer picture. If you want a better idea of what you might pay based on your own circumstances, our whole of life insurance calculator can give you a helpful estimate in just a couple of minutes.

Your Whole of Life Cover Questions Answered

Even after getting to grips with the basics, you might still have a few practical questions knocking around. It's completely normal. This quick FAQ section tackles some of the most common queries we hear day-in, day-out, giving you the straightforward answers you need.

Can I Cash in My Whole of Life Policy?

Yes, in many cases, you can. Lots of whole of life cover policies are designed to build up a ‘surrender value’ or ‘cash-in value’ over the years. Think of it as a pot of money you can access if you decide to cancel the policy before you pass away.

But—and this is a big but—it’s crucial to understand that cashing in a policy, especially in the early days, will almost certainly give you back far less than you’ve paid in premiums. It also means your life cover stops dead in its tracks, leaving your loved ones without that financial safety net you set up for them.

What Happens if I Miss a Premium Payment?

Life happens, and sometimes a payment gets missed. Your cover doesn't just vanish overnight. Insurers in the UK are regulated by the FCA and have to give you a bit of breathing room—typically a grace period of 30 days to get things sorted.

If you don't manage to pay within that window, your policy could ‘lapse’, which is the industry term for your cover ending. If you're finding the premiums a struggle, the best thing you can do is talk to your insurer directly. They’d much rather find a solution than see your policy end.

Can I Make Changes to My Policy?

Some policies do come with a degree of flexibility baked in. For example, you might have the option to increase your cover after a big life event, like getting married or having another baby. This will usually mean going through some more health questions and paying higher premiums.

On the other side of the coin, you might be able to decrease your cover to make your premiums more manageable. For more articles and solid advice on planning your family's finances, including life cover, the Dontforgetdad Blog for family financial insights is a fantastic resource.

Ready to explore your options and lock in that lifelong protection for your family? The team here at Discount Life Cover is on hand to help you find the right policy without breaking the bank.

Get Your Free, No-Obligation Quote Today

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply