As a police officer, you accept a certain level of risk every day. But when it comes to getting affordable police officer life insurance, it’s often far more straightforward than you might imagine. A personal policy works alongside your existing pension benefits, giving you and your family total peace of mind.

This guide explains how UK life insurance works for police officers, helping you bridge any financial gaps and secure your family's future.

Why Police Officers Need a Personal Life Insurance Policy

It’s a common belief among officers that the Police Pension Scheme's 'death in service' benefit is all the financial protection their family will ever need. While this is an absolutely vital part of your benefits package, it’s best to see it as a safety net, not the whole solution.

Think of it this way: your pension benefit is the solid foundation of your family's financial house. It's essential, but it might not be big enough on its own to shelter them from every financial storm, particularly long-term commitments like a mortgage or covering decades of future living expenses.

Bridging the Financial Gap

A personal life insurance policy is specifically designed to bridge the gap between what your pension provides and what your family would actually need to continue without your income. It puts a level of certainty and control in your hands that an employer-provided scheme just can't match.

Consider these common financial realities a personal policy can cover:

- Mortgage Repayment: A death in service payout might not be enough to clear a large mortgage, leaving your loved ones to deal with a significant debt.

- Daily Living Costs: The lump sum needs to replace your salary for years to come, covering everything from council tax and groceries to school shoes and car repairs.

- Future Goals: It can provide the funds for your children's university education or help your partner prepare for their own retirement.

A personal life insurance policy gives you control. You choose the cover amount, how long it lasts, and who receives the payout, making sure the protection is perfectly aligned with your family's specific situation.

Insurers Look Beyond the Uniform

One of the biggest myths is that being a police officer automatically means sky-high premiums. In reality, UK insurers are a lot more nuanced than that. They will assess your specific day-to-day duties, knowing there's a world of difference between a desk-based analyst and a specialist firearms officer.

More often than not, your personal health and lifestyle choices play a much bigger role in determining the final cost.

This detailed approach means that affordable police officer life insurance is well within reach for most. The good news is that officers are often more proactive about getting cover. By understanding the many benefits of life insurance, you can make an informed choice to secure your family's financial future.

Understanding Your Police Pension Benefits

Before you consider how much extra life cover you might need, it’s vital to get a handle on the protection you already have through your service. Every serving UK police officer is automatically part of the Police Pension Scheme 2015, which includes a valuable package of death and injury benefits.

A key part of this is a competitive 'death in service' lump sum payout. Think of it as the solid foundation for your family's financial protection. It's an excellent starting point, but the big question is whether that foundation is strong enough to support everything your family needs if you're not there. You can dig into the official details on the scheme in the Home Office evidence to the Police Remuneration Review Body here.

Calculating Your Existing Cover

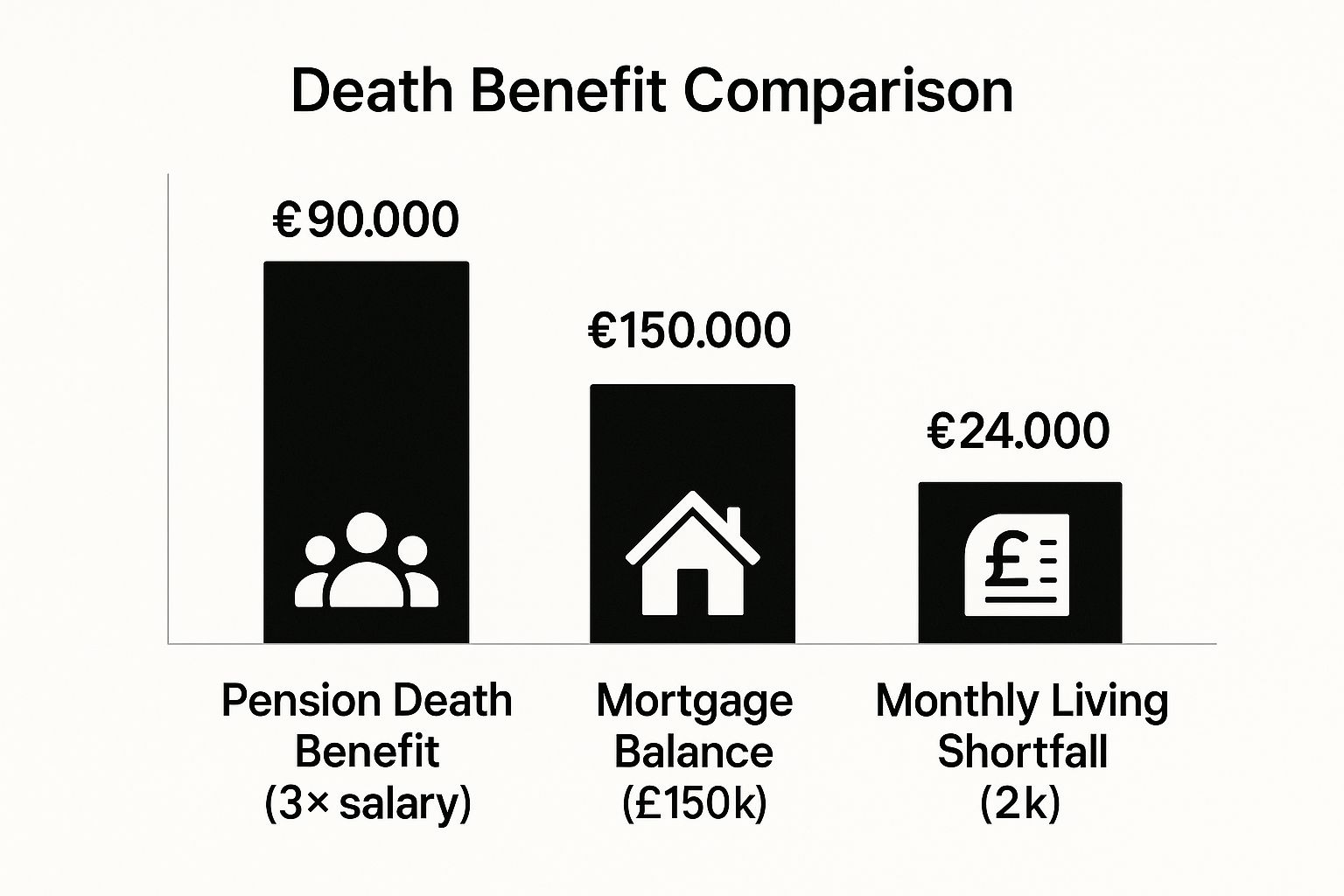

So, how much is this 'death in service' benefit actually worth? It’s usually calculated as a multiple of your annual pensionable salary – in most cases, this is three times your salary. If you’re earning £45,000 a year, your family would receive a tax-free lump sum of £135,000.

That’s a significant amount of money, no doubt about it. But when you start pitting it against big, long-term debts and the sudden loss of your monthly income, you realise it might not stretch as far as you’d hope.

To really see where you stand, you need to compare this payout against your family's biggest financial commitments. The image below gives you a clear picture of how a typical death benefit holds up against the most common household debts and expenses.

As you can see, while the pension payout makes a good dent, a hefty mortgage can swallow most of it, leaving very little to cover all the ongoing costs of running a home and raising a family.

Identifying the Protection Gap

Once you have the figure for your existing cover, the next step is to work out what your family would actually need. This difference between what they'd have and what they'd require is what we call the "protection gap".

Just think about some of these major responsibilities:

- Mortgage or Rent: For most families, clearing the mortgage is the number one priority.

- Household Bills: Council tax, gas, electricity, food… these costs don’t stop.

- Childcare and Education: The costs here can be substantial, from school uniforms and clubs right through to university fees.

- Debts: Any outstanding car finance, credit cards, or personal loans will still need to be paid off.

By subtracting your pension benefit from the total amount your family would need to be secure, you can see the exact size of your financial shortfall. This is precisely the gap that a personal police officer life insurance policy is designed to fill.

To find out the specific details of your scheme, your best bet is to check your annual pension statement or get in touch with your force's HR or pensions administrator. Knowing your numbers is the first and most crucial step towards building a truly secure financial future for the people you care about most.

Choosing the Right Type of Life Insurance

Navigating the world of life insurance can feel a bit daunting at first, but it really boils down to a few straightforward choices. For a police officer, picking the right policy is all about matching the cover to your specific financial duties—whether that's paying off the mortgage for your family or making sure they have a steady income if you're not around.

The most common and cost-effective policies fall under the umbrella of 'term' insurance. In plain language, this means the policy runs for a fixed period you decide on, perhaps 25 years to align with your mortgage. If you were to pass away during that time, your family gets a tax-free lump sum. Let's break down the main types you’ll come across.

Level Term Life Insurance

Level Term insurance is as simple as it sounds: the payout amount (known as the 'sum assured') stays the same from day one until the policy ends. If you get a £200,000 policy for 25 years, it pays out £200,000 whether a claim is made in the first year or the twenty-fourth. No confusion, no surprises.

This consistency makes it a brilliant choice for:

- Covering an interest-only mortgage: Where the capital debt doesn’t shrink over time.

- Replacing your income: It provides a solid, predictable sum for your family to live on, helping them handle bills and keep their lifestyle stable for years.

- Leaving a legacy: You can guarantee a specific amount is left behind for your children’s future, maybe for university fees or a deposit on their first home.

With Level Term, you know exactly what you’re leaving behind. It's clear, predictable protection.

Decreasing Term Life Insurance

As the name suggests, a Decreasing Term policy is one where the potential payout gets smaller over time. It’s tailor-made to protect a repayment mortgage, where the amount you owe the bank also reduces with every payment you make.

The policy is designed so that the cover amount closely tracks your outstanding mortgage balance. Because the insurer's potential payout shrinks each year, these policies are usually the most affordable type of life cover you can get. It's a perfect fit if your main goal is to make sure your family's biggest debt is wiped clean, freeing them from that massive financial weight.

Still weighing your options? Our guide can help you decide between level term or decreasing term life insurance.

Think of Decreasing Term cover as a financial shadow for your mortgage. As your mortgage debt shrinks, so does the cover, ensuring it’s always just enough to pay off the balance without you paying for more protection than you actually need.

Comparing Life Insurance Policy Types for Police Officers

To help you see the options side-by-side, we've put together a quick comparison of the policies we've just discussed. This should give you a clearer picture of which one might be the best fit for your family's needs.

| Policy Type | Best For | Payout Amount | Typical Cost |

|---|---|---|---|

| Level Term | Providing a fixed income for your family, covering an interest-only mortgage, or leaving a set inheritance. | Stays the same throughout the policy term. | More expensive than decreasing term but offers predictable protection. |

| Decreasing Term | Specifically covering a repayment mortgage, ensuring the debt is cleared. | Reduces over time, roughly in line with your mortgage balance. | The most affordable type of life insurance, as the risk to the insurer decreases. |

| With Critical Illness | Protecting against loss of income if you're diagnosed with a serious illness and can't work. | A lump sum paid on diagnosis of a specified illness. | An add-on that increases the premium, but provides crucial financial support during recovery. |

Ultimately, the 'best' policy is the one that gives you peace of mind, knowing your loved ones are protected against your biggest financial commitments.

Adding Critical Illness Cover

Beyond life insurance, it's wise to think about what would happen if you became seriously ill and couldn't work. That’s where Critical Illness Cover steps in. It's an optional extra you can add to most term life policies, and it's well worth considering.

This cover pays out a tax-free lump sum if you are diagnosed with a specific, serious medical condition listed in the policy—things like a heart attack, stroke, or certain types of cancer. For a police officer, this can be a lifeline. A serious diagnosis could easily stop you from returning to active duty, causing a major drop in your household income.

A critical illness payout acts as a financial cushion, giving you the space to focus on getting better without the added stress of worrying about the mortgage or monthly bills.

How Do UK Insurers View Your Police Role?

It’s a common assumption, and a perfectly understandable one: because being a police officer involves risk, life insurance must be a nightmare to get, or at least incredibly expensive. This is one of the biggest myths we come across. The reality of how UK insurers look at your application is far more balanced and, frankly, reassuring.

When an underwriter at an insurance company reviews your application, they don’t just see a generic “police officer” job title and stamp it ‘high risk’. Their job is to get a proper understanding of what you actually do day-to-day. They know that the UK police service is made up of thousands of different roles, and each one has its own unique risk profile.

It’s All About the Detail

The most important part of your application is the section where you break down your duties. The insurer’s goal here is to build a clear picture of what a typical shift looks like for you.

Think about it – the risks faced by officers in different roles are worlds apart:

- A Desk-Based Analyst: An officer working in intelligence, poring over data and writing reports, faces minimal physical risk. To an insurer, they look very much like any other office-based professional.

- A Neighbourhood Constable: An officer on the beat has a different level of risk, which involves engaging with the community and responding to all sorts of routine incidents.

- A Specialist Firearms Officer (SFO): An SFO is, of course, considered a higher-risk role because of the very nature of their assignments.

Insurers weigh up these differences carefully. For the vast majority of officers in non-specialist or administrative roles, their job has very little, if any, negative impact on the final premium. In fact, many standard insurers are perfectly happy to offer competitive terms without adding a single penny to the price because of your occupation.

Your specific duties, not just your job title, are what truly matter to an underwriter. Honesty and detail on your application form are key to getting a fair assessment and the right price.

The Bigger Picture: Your Health and Lifestyle

While your role is a factor, it’s only one piece of the puzzle. For most officers, other standard underwriting factors have a much greater impact on the cost of their policy. These are the usual suspects:

- Your age and health: It's a simple fact that younger, healthier applicants will always secure lower premiums.

- Medical history: Any pre-existing conditions are going to be a significant factor in the calculation.

- Lifestyle choices: Things like whether you smoke or how much alcohol you drink regularly play a huge part in the final price.

Despite the perceived dangers of the job, most serving police officers in the UK can get life insurance at really competitive rates, often no different from people in non-hazardous jobs. Specialist insurers and brokers will always assess an officer's specific duties, but it’s the standard things like your age and health that remain the main drivers of cost. You can find more insights into how police roles are viewed on insurancehero.org.uk. This focus on you as a whole person ensures that your profession doesn't automatically put affordable cover out of reach.

Key Factors That Influence Your Premium

When an insurer works out the price of your life insurance, they're really just trying to measure risk. And while your role as a police officer is definitely part of that conversation, it’s often a smaller piece of the puzzle than you might expect. In reality, a handful of personal and policy-related factors have a much bigger say in the final figure you'll pay each month.

Getting your head around these elements gives you a much clearer picture of how your premium is put together. It’s not some mysterious black box; it's a logical process based on your unique situation, and understanding it puts you back in control.

Your Personal Profile

This is the bedrock of any life insurance application. Insurers need to know who they're covering, and a few key details always form the foundation of their assessment.

- Your Age: This is one of the biggest ones. Younger applicants are simply less likely to have health issues, which means they nearly always get the competitive premiums.

- Your Medical History: Insurers will ask about your current health, any pre-existing conditions like diabetes or heart trouble, and your family's medical background. It's crucial to be completely honest here, as it ensures your policy is valid when your family needs it most.

- Your Lifestyle Choices: Habits like smoking or heavy drinking will push your premium up. In fact, being a non-smoker is one of the single easiest ways to get cover right from the start.

Your Policy Choices

It stands to reason that the type and amount of protection you choose will directly affect the cost. The more cover you need and the longer you need it for, the more it's going to cost.

Think of it like buying petrol for your car. The amount you put in (your cover amount) and how far you plan to drive (your policy term) will determine the total cost. You control these variables to fit your budget and protection needs.

The main decisions you'll make are:

- The Amount of Cover: A policy for £100,000 will naturally cost a lot less than one for £300,000.

- The Policy Term: A 25-year term designed to cover your mortgage will be more expensive than a shorter 10-year policy.

- The Type of Policy: As we've already touched on, a decreasing term policy is usually the most budget-friendly option.

Each of these factors combines to create your personal risk profile, which the insurer then uses to calculate your premium. To get a feel for how these things come together in the real world, you can explore some typical term life insurance rates here. The demands of police work also mean it's wise to understand all aspects of personal wellbeing; for a wider perspective, some find it helpful to read up on things like navigating insurance coverage for addiction treatment.

A Step-by-Step Guide to Applying for Cover

Feeling ready to get your family’s future properly secured? Applying for life insurance is a lot more straightforward than you might think. We’ll break it down into three clear steps to make sure the whole process is as smooth as possible.

1. Calculate How Much Cover You Really Need

First things first, let's figure out the right amount of protection. This isn’t a guessing game. It’s about looking at your financial commitments and asking a simple question: what would my family actually need to stay on their feet if I wasn't here anymore?

Take a look at:

- Your Mortgage: What’s the outstanding balance? The goal here is to make sure your policy could wipe it out completely.

- Family Living Costs: Think about the monthly outgoings – bills, food, petrol, childcare, the lot. Then, multiply that by the number of years you reckon your family would need that support.

- Other Debts: Add up any car loans, credit cards, or other personal loans that would need clearing.

- Future Expenses: Don’t forget the big stuff on the horizon, like university fees for the kids.

Once you have that total, subtract your death in service benefit. That figure right there? That’s your protection gap. That’s the number we need to focus on.

2. Get Your Information Together

With your cover amount sorted, the next job is to get your paperwork lined up. Insurers need a clear picture of who you are to give you an accurate quote and assess your application properly.

You'll need to have these details handy:

- Personal Details: Simple enough – your full name, date of birth, and address.

- Health Information: Be prepared for questions about your medical history, your height and weight, and any pre-existing conditions.

- Lifestyle Habits: Insurers will always ask about your smoking status and how much you drink.

- Your Police Role: This is key. You'll need to give a clear description of what you do day-to-day, especially if you work in a specialist or high-risk unit like firearms or public order.

It's absolutely crucial to be completely honest here. Disclosing everything accurately from the start means your policy will be valid and, most importantly, will pay out without any hassle when it’s needed most. That’s what real peace of mind is all about.

3. Work with a Specialist

Finally, don't try to go it alone. Your best bet is to work with a specialist broker who genuinely understands the market for what insurers call ‘hazardous occupations’.

These brokers know which insurers are best for police officers and have built relationships with them over years. They can cut through the noise, navigate the options for you, and find the most suitable and affordable cover for your specific role and circumstances. It takes the guesswork out of the entire process.

Frequently Asked Questions (FAQ)

We get a lot of the same questions from officers looking into life insurance, so let's tackle the big ones head-on. Here are some clear, straightforward answers to help you get the right protection sorted for your family.

Will my policy pay out if I die in the line of duty?

Yes, absolutely. A standard UK personal life insurance policy is set up to pay out for death from any cause. That includes incidents that happen while you are on duty. The insurer assesses all risks based on your role when you , so as long as you were truthful, your cover is valid.

Do I need to tell my insurer if my police role changes?

Generally, no. Your life insurance contract and premium are based on your circumstances when you take out the policy. You are not typically required to update your insurer if your duties change later on, for example, if you move to a specialist firearms unit. However, if you for a new or additional policy in the future, you must provide up-to-date details of your current role.

Is it better to use a specialist insurance broker?

For police officers, using a specialist broker can make a massive difference. A broker who deals with 'hazardous occupations' knows the market inside out. They understand which insurers (like Aviva, Legal & General, or Zurich) are most favourable for various police roles, helping you find the most competitive price without the hassle of shopping around yourself.

Ready to get your family’s financial future secured? The team at Discount Life Cover can help you compare quotes from the UK's leading insurers to find the right policy for you and your role. Get your free, no-obligation quote today and take the first step towards proper peace of mind.

Get Your Free Police Life Insurance Quote Now

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply