Facing a cancer diagnosis makes you think about the future and how to protect your loved ones. It’s a natural worry that often leads to a crucial question: can I still get life insurance?

For many people in the UK, the answer is a resounding yes. Securing life insurance for cancer survivors might seem like an uphill battle, but it's far from impossible.

Securing Life Insurance After Cancer: Is It Possible?

Navigating the world of life insurance after a cancer diagnosis can feel overwhelming. But understanding the basics is the first step towards regaining control. The good news is that UK insurers have become far more experienced in assessing applications from cancer survivors. A past diagnosis is no longer an automatic rejection.

Instead, providers regulated by the Financial Conduct Authority (FCA) will take the time to understand your individual health journey to make a fair and informed decision.

This guide is designed to cut through the jargon and explain how insurers assess your medical history and what this means for your application. While getting cover involves a detailed look at your specific circumstances, having the right information will give you the confidence to navigate the process.

What Insurers Consider

When you for a policy, the insurer’s main job is to build a clear picture of your long-term health. They don’t just look at the diagnosis itself; they piece together a much larger puzzle.

Here are the key factors they will focus on:

- Type and Stage of Cancer: Every cancer is different, and insurers know this. An early-stage, localised cancer is viewed very differently from one that was more advanced or had spread.

- Treatment History: What kind of treatment did you have? Was it surgery, chemotherapy, radiotherapy, or another therapy? And, most importantly, how successful was it? These details are vital.

- Time in Remission: This is perhaps the most significant factor. The longer you’ve been cancer-free and finished with treatment, the more favourably an insurer will view your application. It’s a powerful indicator of stability.

- Overall Health and Lifestyle: Insurers will also consider you as a whole person. Your current health, your age, and lifestyle choices like whether you smoke all play a part in their assessment.

Think of it like this: your application is your health story. The more complete and clear that story is—supported by medical records and the passage of time—the easier it is for an insurer to understand your risk and offer you the right cover.

By understanding these core elements, you can be better prepared for the questions they’ll ask and begin gathering the information you’ll need. Our goal is to empower you with the knowledge to find a policy that provides peace of mind and secures your family’s financial future.

How Insurers Assess Your Application

To understand your options for life insurance for cancer survivors, it helps to see things from an insurer's perspective. When you , they begin a process called underwriting, which is essentially a detailed risk assessment. Their goal is to build a complete picture of your health to determine the likelihood of a future claim.

An underwriter reviews your medical history to understand your long-term health outlook. A history of cancer is a significant event, so they will examine it very closely. This isn’t about making a judgement; it's about making a fair, calculated decision based on medical evidence and statistical data. Knowing what they’re looking for will help you provide the right information and set realistic expectations.

Key Factors in the Underwriting Process

Insurers will focus on several specific details about your cancer journey to make their assessment. Being ready with clear, accurate information on these points can make the application process much smoother.

Here’s what they will be most interested in:

- The Type and Grade of Cancer: Different cancers have vastly different outlooks. A low-grade, non-invasive cancer is viewed much more favourably than a high-grade, aggressive one.

- The Stage at Diagnosis: This tells them how far the cancer had progressed when it was discovered. An early-stage diagnosis (like Stage 1) represents a much lower long-term risk than a late-stage one (like Stage 4).

- Your Treatment History: Details about your treatment are vital. They’ll want to know if you had surgery, chemotherapy, radiotherapy, or other therapies, and crucially, whether the treatment was successful.

- Time Since Treatment Ended: This is a major factor. The longer you have been in remission and clear of treatment, the lower the statistical risk of recurrence. This makes you a more attractive applicant.

By pulling all these factors together, underwriters create a risk profile. This profile helps them decide whether they can offer you cover, what the premium will be, and if any specific conditions or exclusions need to be included in the policy.

Why Your Medical History Is So Important

Insurers rely heavily on medical evidence because, unfortunately, cancer remains a leading cause of critical illness claims in the UK. A detailed medical history helps an insurer see you as an individual, not just a statistic. For instance, our guide on getting life insurance with medical conditions explains how underwriters look at all sorts of health issues, and a past cancer diagnosis is treated with the same careful approach.

They will almost certainly request a report from your GP or specialist to confirm the details you’ve provided. This is standard practice for anyone with a significant medical history. It is crucial to be honest and accurate on your application form, as any inaccuracies could cause problems and even invalidate your policy later on.

What to Prepare for Your Application

Knowing what insurers need means you can get organised beforehand, making the application as smooth as possible. It’s a good idea to have key dates and documents ready.

Try to have this information to hand:

- Date of Diagnosis: The exact date your cancer was first diagnosed.

- Cancer Details: The specific type, grade, and stage of the cancer.

- Treatment Summary: A list of all treatments you had, including the start and end dates.

- Remission Date: The date you were officially told you were in remission or received the "all-clear."

- Follow-Up Care: Details on any ongoing check-ups, scans, or medication you still take.

Having this information organised not only helps the underwriter process your application more efficiently but also demonstrates that you are prepared.

Types of Life Insurance Policies in the UK

Once you feel ready to explore your options, it’s helpful to understand the main types of life insurance policies available in the UK. They are all designed for different purposes, and your medical history will influence which one is most suitable for you.

Let's review the most common policies to give you a clear idea of what's available.

Term Life Insurance

This is the most popular type of cover in the UK. It's very straightforward: you choose a cash lump sum (the 'sum assured') and a length of time (the 'term'). If you pass away during that period, your family receives the payout. People often use it to cover large debts like a mortgage or to ensure their children are financially supported.

It usually comes in two forms:

- Level Term Insurance: The payout amount stays the same for the entire policy. If you take out a £200,000 policy for 25 years, it pays out £200,000 whether you pass away in year two or year twenty-four. It’s ideal for families needing a reliable financial safety net, for example, to cover rent and living costs.

- Decreasing Term Insurance: With this policy, the payout amount reduces over time, typically in line with a repayment mortgage. As your mortgage balance decreases, so does the amount of cover you need. This makes it a more affordable way to protect your home loan specifically.

For cancer survivors, term insurance is often the most realistic option once you've been in remission for a few years. Insurers will review your medical history thoroughly, but obtaining a policy is certainly possible.

Whole of Life Insurance

As the name suggests, Whole of Life insurance covers you for your entire life. It guarantees a payout whenever you pass away, as long as you've kept up with the monthly premiums.

Because the payout is competitive, the premiums are considerably higher than for term insurance. This type of policy is typically used for two main reasons:

- Covering Funeral Costs: To ensure final expenses are taken care of without leaving a financial burden for the family.

- Inheritance Tax Planning: To provide a lump sum that helps your beneficiaries settle a potential inheritance tax bill.

Given the competitive payout, the underwriting for Whole of Life policies is extremely strict. For cancer survivors, securing this type of cover can be more difficult and expensive, but it is not impossible, especially if you've been in remission for many years.

Over 50s Life Insurance Plans

For anyone aged 50 and over, there’s another option: a competitive acceptance Over 50s plan. These are a type of Whole of Life cover, but they have one significant advantage: you are competitive to be accepted with no medical questions asked.

This makes them a vital option for people who might be declined for standard life insurance due to their medical history, including a past cancer diagnosis. You can explore your options further in our guide to no medical exam life insurance.

However, there are a couple of important points to be aware of:

- Waiting Period: Most plans have a 'waiting' or 'deferment' period, usually for the first 12 or 24 months. If you pass away from natural causes during this time, the insurer will typically refund the premiums you've paid rather than the full cash sum.

- Lower Payouts: The maximum payout is generally smaller than with standard policies, often capped at around £20,000 to £25,000.

These plans are primarily designed to cover funeral expenses or to leave a small cash gift. They offer a valuable safety net when other options may not be available.

Comparing Life Insurance Policies for Cancer Survivors

To make things clearer, here's a quick comparison of the main policy types. Seeing them side-by-side can help you decide which route might be best for your situation.

| Policy Type | How It Works | Best For… | Considerations for Cancer Survivors |

|---|---|---|---|

| Term Life Insurance | Pays out a lump sum if you pass away within a set term (e.g., 25 years). | Covering large debts like mortgages or providing for young families. | Generally the most accessible option after a few years of remission. Underwriting is detailed. |

| Whole of Life Insurance | Guarantees a payout whenever you pass away, as long as premiums are paid. | Covering funeral costs or helping with inheritance tax planning. | Can be difficult and expensive to secure due to strict underwriting. More likely to be an option after a long period of remission. |

| Over 50s Plan | A competitive acceptance whole of life policy with no medical questions. | People over 50 who want to cover funeral costs or leave a small gift. | A vital option if you've been declined for other policies. Be aware of the 12-24 month waiting period. |

| Critical Illness Cover | Pays out a lump sum if you're diagnosed with a specific serious illness. | Providing a financial buffer to cope with the impact of a serious illness. | Will almost certainly have an exclusion for cancer. Can be complex to arrange; expert advice is key. |

Ultimately, the 'best' policy is the one that fits your personal and financial needs while being realistic about what insurers are likely to offer.

Understanding Critical Illness Cover

Critical Illness Cover is often sold as an add-on to a life insurance policy. It's designed to pay out a tax-free lump sum if you're diagnosed with one of the specific serious illnesses listed in the policy, such as a heart attack, a stroke, or cancer.

For a cancer survivor, adding critical illness cover can be complicated. Insurers will almost certainly place an 'exclusion' on the policy for any cancer-related claims. This means the policy would still pay out for other conditions like a stroke, but it would not pay out if you were diagnosed with cancer again.

The UK insurance market has adapted to the growing number of survivors, but this often means policies come with specific limitations. As research from leading British insurer Legal & General points out, many providers require a waiting period of 2 to 5 years post-remission before they will consider standard terms, and a cancer diagnosis will usually lead to exclusions on related critical illness claims. You can discover more insights about their approach on Legal & General's website.

It is essential to speak with a qualified adviser to get complete clarity on what would and would not be covered before committing to a policy.

Why Your Remission Timeline Matters

When you're ing for life insurance after cancer, one of the first questions an underwriter will ask relates to time. How long has it been since you finished treatment? How long have you been in remission?

This timeline is absolutely critical. Statistically, the longer you are cancer-free, the lower the chances of recurrence. For an insurer, a longer remission period indicates a more stable and predictable health outlook.

While it can feel like a frustrating waiting game, timing your application is one of the most powerful tools you have. Applying too soon could result in a decline or extremely high premiums. Waiting a bit longer may open up more options with better rates.

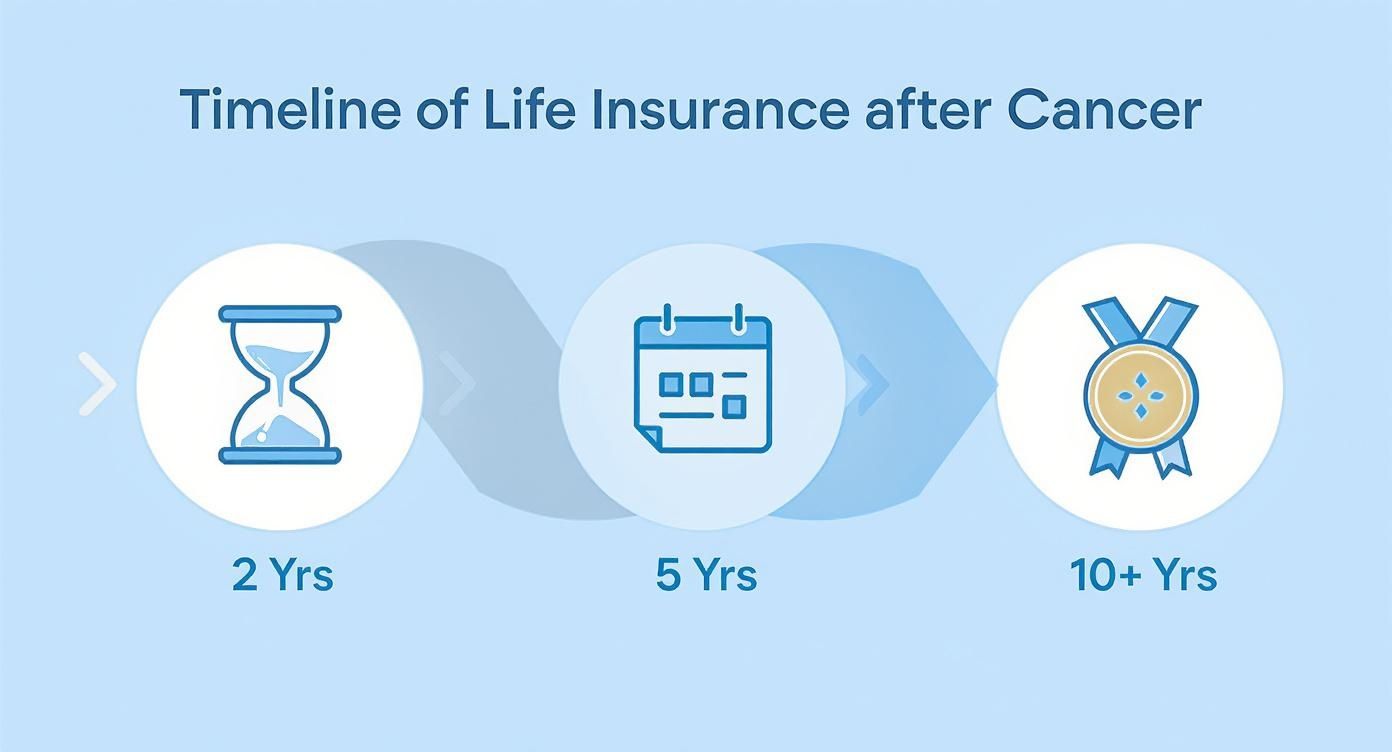

Key Milestones Insurers Look For

Most insurers use internal guidelines tied to specific post-remission timeframes. Although the exact rules vary between companies, they tend to follow a predictable pattern. Reaching these milestones can make a significant difference to your application.

- Under 2 Years Post-Remission: This is generally considered the highest-risk period. Getting a standard term life insurance policy is very difficult. acceptance plans like an Over 50s policy may be your main option, provided you meet the age criteria.

- 2 to 5 Years Post-Remission: Once you pass the two-year mark, your prospects improve. Many insurers will start to consider offering you cover. Your premiums will likely be 'loaded' (increased) to reflect the remaining risk, but obtaining a policy becomes a real possibility.

- 5 to 10 Years Post-Remission: The five-year all-clear is a major turning point. Insurers view your application much more favourably, and you are far more likely to be offered competitive terms.

- 10+ Years Post-Remission: A decade after treatment, you have the best chance of getting cover at or very close to standard rates. This is especially true for less aggressive types of cancer.

This timeline gives you a clearer picture of how these milestones can shape your life insurance journey.

As you can see, the further you move away from your diagnosis and treatment, the better your options become, shifting from restricted plans towards standard policies.

A Tale of Two Applications

Let's look at a real-world example.

Imagine Sarah, a 40-year-old homeowner, applies for life insurance just 18 months after finishing her breast cancer treatment. Because the remission period is so short, insurers will likely view her as a high risk and may decline her for a standard policy.

Now, consider David. He is also 40 and had a similar diagnosis, but he waits seven years after his treatment before ing. With a long, stable history of remission, his application is seen in a completely different light. He is much more likely to be approved with far more affordable premiums. The only difference? Timing.

Waiting allows you to build a stronger case for your long-term health. Each year that passes without recurrence provides concrete evidence to an underwriter that your prognosis is positive, which can directly impact your term life insurance rates.

The good news is that the insurance world is slowly catching up with medical reality. Cancer survival rates in the UK have doubled in the last 50 years, and it is now expected that 1 in 2 people will survive their diagnosis for at least 10 years.

This growing population of survivors means insurers must adapt. While a waiting period of two or more years is still common, the industry is gradually evolving to better serve the UK's 3 million cancer survivors. It’s a slow process, but it is happening.

Understanding how your remission timeline fits into this picture helps you manage expectations and plan your next steps. It’s not about being penalised; it's about insurers using the data they have to make a fair assessment of risk. By waiting for the right moment, you give yourself the best possible chance at securing the financial protection your family deserves.

A Practical Checklist for Your Application

Tackling a life insurance application can feel daunting, especially after cancer. But a little preparation can make all the difference, turning a stressful task into a straightforward one. A strong application is about being accurate, transparent, and organised. When you gather the right information beforehand, you provide underwriters with a clear and credible picture, which often leads to a smoother process and a better outcome.

This checklist will guide you through everything you need to build the strongest possible application.

Get Your Medical Documents in Order

Your medical history is the foundation of your application. Insurers need specific details to make a fair assessment, so having everything ready is crucial.

Before you start an application form, try to collect these details:

- Diagnosis Details: Note down the exact date you were first diagnosed, along with the specific type, grade, and stage of the cancer.

- Treatment Summaries: Create a timeline of every treatment you received, such as surgery, chemotherapy, or radiotherapy. Include start and end dates for each.

- Remission Confirmation: Have the exact date you were officially told you were in remission or received the "all-clear" from your specialist.

- Follow-Up Reports: Gather details of any ongoing check-ups, scans (like MRIs or CT scans), and any medication you're still taking.

- Consultant Details: Keep the names and contact information for your GP and any oncologists or other specialists who treated you to hand.

Be Completely Open and Honest

It might be tempting to omit certain details of your health history, but this would be a serious mistake. Being upfront on your application is not just good practice; it's a legal requirement in the UK.

Under the principle of 'utmost good faith', you must disclose all relevant facts. Failing to mention your cancer history, or providing incorrect dates, is known as non-disclosure. If the insurer discovers this later, they could cancel your policy or refuse a future claim, leaving your family without the protection you arranged.

Insurers will almost certainly request a medical report from your GP to verify the information you have provided. This is standard procedure for anyone with a significant medical history. Ensuring your application matches your medical records from the start avoids potential delays and complications.

Work with a Specialist Broker

Navigating the life insurance market after cancer can be overwhelming. Not all insurers assess risk in the same way; some are more understanding of cancer survivors than others. Trying to find the right one on your own can be like searching for a needle in a haystack.

This is where a specialist broker, like the experts at DiscountLifeCover, can be invaluable. A good broker:

- Knows the Market: They know exactly which insurers are most likely to offer favourable terms to cancer survivors.

- Presents Your Case: They can help frame your application in the best possible light, ensuring all positive factors are highlighted.

- Saves You Time and Stress: They do the legwork, speaking to different insurers and comparing quotes for you, so you don't have to complete numerous forms.

Highlight Your Healthy Lifestyle

While your cancer history is a major part of the picture, underwriters also consider your current and future health. Demonstrating a commitment to a healthy lifestyle can make a positive difference.

Be sure to include details about positive lifestyle choices, such as:

- Being a non-smoker (or having quit a long time ago)

- Maintaining a healthy weight and BMI

- Regular exercise and an active lifestyle

- Moderate alcohol consumption

These details help paint a more complete picture of who you are today, showing the underwriter that you are actively managing your health. This proactive approach can sometimes lead to better terms or smaller premium 'loadings', making your cover more affordable.

Your Questions Answered (FAQ)

Sorting out life insurance after a cancer diagnosis can bring up many questions. Here are clear, straightforward answers to some of the most common ones we hear from cancer survivors in the UK.

Will my premiums always be higher?

Initially, it's very likely, but not necessarily forever. An insurer may a premium 'loading', which is an extra charge added to the standard price to reflect the higher perceived risk due to your medical history. The size of this loading depends on your cancer type, its stage, and how long you've been in remission. The good news is that as more time passes and you remain healthy, you may be able to have your policy reviewed or find a new one with more favourable terms.

What happens if I don't disclose my cancer history?

You must never do this. Hiding your cancer diagnosis or any part of your medical history is called non-disclosure, and the consequences are severe. If the insurance company finds out later (which is highly likely when processing a claim), they have the legal right to void your policy. This means they will not pay out, leaving your loved ones unprotected. Under UK law, honesty is a fundamental part of the insurance contract.

Can I get life cover if my cancer is terminal?

If you have recently received a terminal diagnosis, you will not be able to take out a new life insurance policy. However, if you already have a policy in place, it will almost certainly include a Terminal Illness Benefit. This feature allows the policy to pay out early if you are diagnosed with a terminal illness and doctors expect you have less than 12 months to live. This can provide essential financial support for you and your family.

Are there policies that don't ask medical questions?

Yes. If you are aged between 50 and 85, a Acceptance Over 50s Plan could be an excellent alternative, particularly if you have been declined for standard cover. These policies guarantee acceptance for UK residents in that age bracket with no medical questions. Just be aware that they usually have a waiting period of 12 or 24 months, during which they will not pay out for death by natural causes (though premiums are typically refunded). They are a valuable option for securing a smaller lump sum to cover funeral costs or leave a small gift.

Take Control of Your Financial Future

Getting life insurance after cancer is not an impossible hurdle; it is a realistic and achievable goal. The key is to understand the process, be patient, and be completely honest about your situation. It's a significant step towards taking back control and ensuring your family's financial security.

It all comes down to knowing how insurers view your application, understanding the importance of your remission timeline, and choosing the right policy for your needs. When you get your medical details in order and are transparent from the beginning, you build the strongest possible case.

Taking the Next Steps

Let’s quickly recap the most important points:

- Knowledge is Power: Understanding the underwriting process makes it far less daunting.

- Timing is Key: The longer you've been in remission, the better your options and premiums will generally be.

- Honesty is Essential: Full disclosure is non-negotiable. It ensures your policy is valid when your family needs it most.

- Expert Guidance Helps: A specialist broker knows the market and can connect you with insurers who are more likely to offer you cover.

Beyond life cover, considering things like how to write a will is another crucial part of protecting your financial future and making sure your wishes are respected. Taking care of these matters brings incredible peace of mind.

Getting life insurance for cancer survivors is more than just a financial decision. It's about drawing a line under the past and building a secure future for the people you love. With the right information and support, you can find a policy that gives your family the protection they deserve.

You've read the guide, now it's time to take the next step and explore your options.

Feeling ready to see what's out there? The expert advisers at Discount Life Cover are here to help you navigate your choices, with no pressure or obligation.

Get your free, personalised quote today and take the first step towards peace of mind.

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply