When people ask, "How much is life insurance monthly?" they're often bracing themselves for a big number. There's a common belief that it's a major expense, but the reality is usually a pleasant surprise. For a healthy person, basic cover can start from just a few pounds a month.

A Quick Look at Monthly Life Insurance Costs

It’s easy to think that protecting your family's future will take a huge bite out of your budget. Honestly, though, that’s rarely the case. For most people in the UK, life insurance is a perfectly manageable and sensible part of their financial planning.

The cost isn't a one-size-fits-all figure; it really comes down to your personal circumstances. We'll get into all the nitty-gritty details later, but for now, let's establish a rough baseline. This will give you a general idea of what to expect before we dive into what makes your quote unique.

What Is a Typical Monthly Cost?

Time and again, research shows that life insurance is much than people think. A healthy, non-smoking 30-year-old could get £100,000 of cover for around £5 a month. It’s often less than the cost of a couple of coffees from a high-street chain.

To give you a clearer picture, we've put together a simple table. It shows what a healthy, non-smoking individual in the UK might expect to pay for a standard policy.

Average Monthly Life Insurance Costs for a Healthy Non-Smoker

The table below gives you a ballpark idea of costs for a £150,000 level term policy running for 25 years. These estimates are for someone who is in good health, doesn't smoke, and works in a low-risk job.

| Age | Average Monthly Premium |

|---|---|

| 30 | £8 – £12 |

| 40 | £13 – £18 |

| 50 | £25 – £35 |

These figures are a great starting point, but remember, the premium you're offered will be tailored specifically to you by UK insurers like Aviva, Legal & General, or LV=.

The best way to get a solid number? For a precise figure based on your own situation, jump over to our life insurance cost calculator and get a personalised estimate in minutes.

What Really Shapes Your Life Insurance Premium?

Ever wondered how insurers actually land on your monthly price? It’s not just a number plucked from thin air. It’s a careful calculation based on who you are and the life you lead. Think of it like a puzzle, where each piece – from your age to your hobbies – helps build the final picture of your premium.

This whole process is called underwriting. In plain language, insurers are weighing up the risk they're taking on by offering you cover. The higher they think that risk is, the higher your monthly premium will be. This process is regulated by the Financial Conduct Authority (FCA) to ensure fairness.

Getting your head around these factors is powerful. It means you can see exactly what’s driving the cost, giving you a much better handle on finding a quote that feels fair and affordable.

Your Age and Health Are Top of the List

It's the most straightforward fact in life insurance: the younger and healthier you are, the your premiums will be. An insurer’s main calculation is based on life expectancy. Statistically, a younger person is far less likely to pass away during the policy term, which is why a 30-year-old will pay a lot less than a 50-year-old for the exact same amount of cover.

Your current health and medical history are just as vital. Insurers will need to know about:

- Pre-existing medical conditions: Things like diabetes, heart conditions, or a history of cancer will influence your premium.

- Your height and weight: Your Body Mass Index (BMI) is used as a quick indicator of your general health.

- Family medical history: If serious hereditary conditions like heart disease run in your immediate family, that can also be a factor.

Certain health conditions, like high blood pressure, are a big focus for insurers. For a bit more background, understanding what causes high blood pressure and how to manage it offers a good insight into how insurers view these kinds of risks.

Lifestyle Choices That Make a Difference

Your day-to-day habits give insurers some of the strongest signals about your personal risk profile. The single biggest lifestyle factor? Smoking or vaping.

Being a smoker can easily double the cost of your life insurance. Insurers see nicotine use, in any form, as a major red flag for your health. The good news is if you've been totally nicotine-free for at least 12 months, you can be classed as a non-smoker and get access to much lower premiums.

Other lifestyle factors they'll look at include:

- Alcohol consumption: They’ll ask about your average weekly unit intake.

- Dangerous hobbies: A passion for things like mountaineering, scuba diving, or private piloting means more risk, and therefore, a higher cost.

- Occupation: A job with more physical risk, like a scaffolder or construction worker, is likely to come with higher premiums than an office-based role.

How Your Policy Details Impact the Cost

Finally, the nuts and bolts of the policy you choose are a massive driver of the final cost. The decisions you make here have a direct and immediate impact on what you'll pay each month.

The larger the potential payout (sum assured) and the longer the policy runs (term), the higher your monthly premium will be. A £500,000 policy will naturally cost more than a £150,000 one.

Keep these key policy levers in mind:

- Amount of Cover: How much cash would your loved ones actually receive?

- Length of Term: For how many years will the policy be active?

- Type of Policy: A level term policy (where the payout stays the same) usually costs more than a decreasing one (where it reduces over time).

Each of these is a piece of the pricing puzzle. By understanding them, you can start to see how tweaking different options will affect your quote. For a more detailed look, you can explore our guide on current term life insurance rates to see exactly how these variables play out in the real world.

Choosing a Policy That Fits Your Life and Budget

Not all life insurance is created equal. The type of policy you go for will have a big impact on your monthly cost, so getting your head around the main options is the first step to finding cover that actually works for you and your bank balance.

For most families in the UK, the go-to choice is term life insurance. Think of it as straightforward, no-frills protection. It covers you for a specific amount of time – the ‘term’ – say, 25 years while the children are growing up and the mortgage is being paid. If you were to pass away during that term, your family gets a tax-free lump sum. It’s simple, it's affordable, and it’s designed to protect you when you need it most.

Level Term vs Decreasing Term Cover

Even within term insurance, you’ve got a couple of choices to make. The one you pick will directly change how much your life insurance is per month.

Level Term Insurance: With this type of policy, the payout amount – what insurers call the sum assured – stays the same from day one to the end of the term. If you take out a £200,000 policy, it will pay out £200,000 whether you pass away in year one or year twenty-four. This makes it a great fit for covering general family living costs or an interest-only mortgage.

Decreasing Term Insurance: As the name suggests, the payout amount on this policy gradually drops over time. It’s designed to run alongside a repayment mortgage, so as your mortgage balance shrinks, so does your level of cover. Because the risk to the insurer goes down every year, this is almost always the option of the two.

To give you an idea of the numbers, recent market research shows the average monthly premium for a single level term policy in the UK is £9.71. A joint policy averages £16.84. You can find more detail on life insurance averages to see how decreasing term cover consistently comes in at an even lower price point.

Whole of Life Policies

Unlike term insurance which has an expiry date, a Whole of Life policy does exactly what it says on the tin—it covers you for your entire life. As long as you keep up with the premiums, a payout is competitive when you eventually pass away.

That guarantee comes at a price, though. These policies are quite a bit more expensive than term cover. They’re typically used for more specific financial planning, like leaving a legacy for your children or covering a hefty inheritance tax bill.

Popular Add-Ons like Critical Illness Cover

Many UK insurers will give you the option to bolt on Critical Illness Cover to your life insurance policy. This is a valuable extra that pays out a tax-free lump sum if you’re diagnosed with a serious, specified illness like cancer, a heart attack, or a stroke.

Of course, adding this will bump up your monthly premium. But it provides a crucial financial cushion at a time when you might be too ill to work. It’s a classic trade-off: a slightly higher monthly cost in exchange for much broader peace of mind for you and your family.

See How Costs Change for Different People

To really get a feel for how much life insurance is each month, it's best to move past the averages and look at real-life scenarios. When you can see the numbers laid out for different people, it all starts to make a lot more sense.

The premium you're quoted is completely personal to you, shaped by your age, health, lifestyle, and how much cover you actually need. A young parent will naturally have a different premium to a homeowner in their 40s or someone over 50 sorting out their final affairs.

Let's walk through a few common examples to see exactly how these factors come into play. We'll also compare costs for non-smokers and smokers, which really highlights just how much of an impact a single lifestyle choice can have.

Example 1: The Young Parent

Meet Sarah. She's 30, a non-smoker, and has two young children. Her priority is making sure there's a financial safety net to cover day-to-day living costs, childcare, and future education if she were no longer around.

She opts for a £250,000 level term policy that runs for 25 years. This will see her through until her youngest is well into adulthood. Because she's young and healthy, her premium is incredibly affordable.

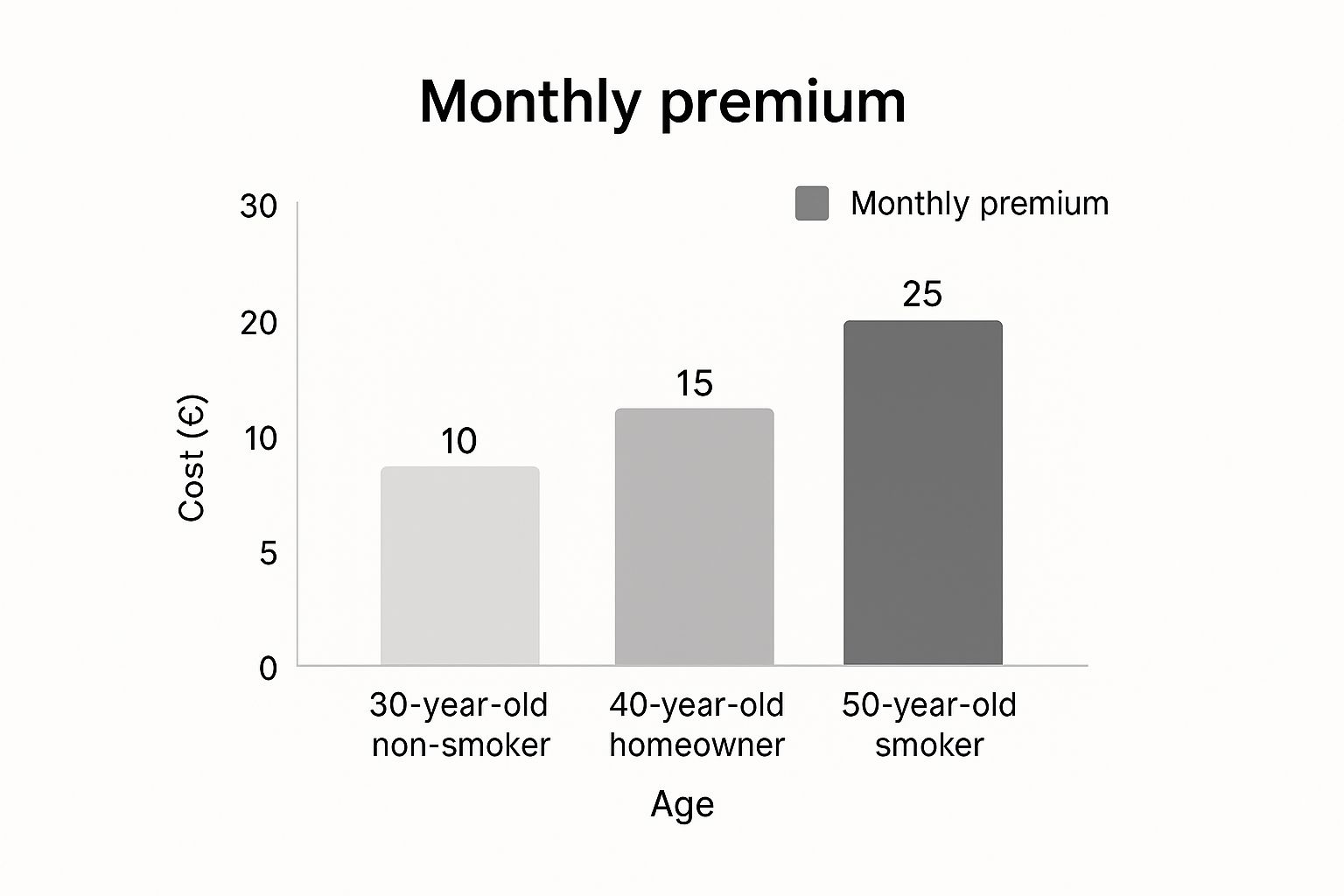

- As a non-smoker, Sarah’s monthly premium is around £10.

- If Sarah were a smoker, that same cover would jump to roughly £18 per month—almost double the cost.

Example 2: The Homeowner

Now let’s look at David, a 42-year-old non-smoker who has just bought a new house with his partner. They have a £200,000 repayment mortgage and need a policy that will clear the debt if one of them were to pass away.

For them, a decreasing term policy is the perfect fit. The amount of cover goes down over time, mirroring their shrinking mortgage balance. This makes it a much option than level term cover.

- As a non-smoker, David’s monthly premium is around £15.

- If David were a smoker, that premium would climb to a much steeper £28 per month.

The infographic below gives a quick visual summary of how these monthly premiums can differ based on age and lifestyle.

As you can clearly see, both getting older and being a smoker will push your premiums up. It's a stark reminder of the financial benefit of sorting out your cover earlier in life and looking after your health.

Example 3: The Over 50s Planner

Finally, let's consider Linda. She is 55, a smoker, and her health isn't perfect. She wants to leave a small lump sum for her grandchildren and make sure her funeral costs are taken care of.

She looks into an Over 50s Life Insurance plan, which offers competitive acceptance without any medical questions. For a competitive payout of £10,000, her premiums are fixed for the rest of her life.

- As a 55-year-old smoker, Linda’s premium for this specialised cover is around £35 per month.

These snapshots show that while the costs can vary quite a bit, there are affordable options out there for almost everyone. The real key is finding the right policy that matches your specific needs and circumstances.

Actionable Ways to Lower Your Monthly Premium

Finding affordable cover doesn't have to be a massive headache. There are some practical, common-sense steps you can take to bring down your monthly life insurance costs, often without having to compromise on the quality of your protection.

Thinking about how much is life insurance monthly can be a bit daunting, but you actually have more control over that final number than you might realise. By making a few smart decisions and maybe tweaking some lifestyle habits, you can lock in the peace of mind you're after at a price that won't break the bank.

Act Early and Improve Your Health

The golden rule of life insurance is simple: buy it when you are young and healthy. Age is the biggest single factor that insurers look at, so locking in a rate in your 20s or 30s will always be than holding off until your 40s or 50s.

Quitting smoking is another absolute game-changer for your premiums. Insurers will typically class anyone who has been completely nicotine-free for at least 12 months as a non-smoker, which can slash your costs by as much as half. If you're a smoker looking to cut back, it’s worth exploring the potential savings from switching to e-cigarettes as a first step.

Choose the Right Policy Structure

The type of policy you go for has a direct impact on what you'll pay each month. As we've mentioned, decreasing term insurance is usually than level term because the payout shrinks over time. This makes it a smart, cost-effective choice if your main goal is to protect a repayment mortgage.

Another thing to weigh up is joint vs single policies. A joint 'first death' policy covers two people but only pays out once. While it's often a bit than two separate single policies, it does leave the surviving partner without any cover. In many cases, two single policies can offer far more flexibility for a very similar price.

Compare Quotes to Find the Best Deal

Shopping around is, without a doubt, the most effective way to make sure you aren't overpaying. An independent broker like us here at Discount Life Cover can compare quotes from a huge range of leading UK insurers in minutes. We'll instantly show you who's offering the most competitive price for your specific situation.

Using a specialist also means you get expert guidance on how to structure your policy to meet your needs without paying for things you don't. For more insights, our guide on finding the cheapest term life insurance is packed with even more practical tips.

Frequently Asked Questions

It’s only natural to have a few questions rattling around when you're looking into something as important as life insurance. Let's tackle some of the most common ones we hear, giving you clear, straightforward answers to help you move forward with confidence.

How Much Life Insurance Do I Actually Need?

While there’s no magic number that fits everyone, a good rule of thumb is to aim for a policy that pays out roughly 10 times your annual salary. Think of that figure as a starting point. For a more tailored amount, you need to do a bit of simple maths: calculate what your family would need, then subtract what they already have.

- Financial Obligations: Add up your mortgage, any outstanding loans or credit card debts, and future costs like childcare or university fees. Then, multiply your yearly salary by the number of years your family would need it to get by.

- Existing Assets: Subtract anything you've already got, such as savings, investments, and any death-in-service benefit you might have through work.

The number you're left with is a much better reflection of the cover you probably need.

Is Life Insurance Really Worth It in the UK?

If you have anyone who depends on you financially – a partner, children, even elderly parents – life insurance is one of the most vital safety nets you can put in place. It’s all about peace of mind. Knowing your loved ones wouldn't be left in a financial hole if the worst happened is priceless. The monthly cost is often a pleasant surprise, far lower than most people imagine, especially when you weigh it against the enormous relief it could provide at an incredibly difficult time.

Can I Get Cover with a Pre-Existing Medical Condition?

Yes, in most cases, you absolutely can. It’s a huge misconception that having a health issue automatically means you can't get life insurance. UK insurers deal with applications every day from people with a wide range of conditions, such as diabetes, high blood pressure, or a history of cancer. Having a condition might mean your monthly premiums are a bit higher, but it very rarely means you can't get any cover at all. The golden rule is to be completely upfront on your application.

Get Your Personalised Quote Today

Understanding the factors that influence your life insurance premium is the first step towards securing affordable, effective cover for your family. The next step is to see what a policy would actually cost for you.

At Discount Life Cover, we make it easy to compare quotes from the UK's top insurers, helping you find the right protection at the competitive. Get your free, no-obligation quote today and take a positive step towards protecting your loved ones' future.

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply