Whole of life insurance is a type of life cover that guarantees a tax-free payout whenever you pass away, as long as you keep up with your monthly payments. Unlike other policies that expire after a certain number of years, this cover is designed to last for your entire life, giving your loved ones a permanent financial safety net.

Understanding How Lifelong Cover Works

At its core, whole of life insurance is a simple promise between you and a UK insurance company. You agree to pay a fixed monthly amount (your premium), and in return, the insurer guarantees to pay a lump sum to your family when you die.

Think of it like owning a home versus renting one. Term life insurance is a bit like renting; you’re covered for a specific period, perhaps 20 or 30 years, and once that term ends, so does your cover. If you pass away during the term, your family gets a payout. If you don't, the policy simply expires.

Whole of life insurance, on the other hand, is like owning your financial safety net outright. It becomes a permanent asset that will be there for your family, whether you pass away next year or in fifty years. That certainty is what it’s all about.

The Two Pillars: Certainty and Permanence

The real appeal of this type of policy comes down to two key principles you don't get with temporary cover. Understanding these helps show why it’s the go-to choice for certain long-term financial goals.

- Fixed Premiums: With most whole of life policies, the price you pay each month is locked in from day one. It won’t increase as you get older or if your health changes. This gives you fantastic predictability for your budget over the long term, removing any worry about rising costs down the line.

- Payout: So long as you keep paying your premiums, the policy is absolutely certain to pay out. This makes it a rock-solid tool for financial planning, especially when you want to cover funeral expenses or leave a definite inheritance.

This is a world away from term insurance, where there's always the chance you could outlive your policy, leaving your family with nothing to show for all those payments. For anyone seeking total peace of mind, the permanence of whole of life cover is its greatest strength.

The Main Types of Whole of Life Cover in the UK

When you start looking into your options, you'll find that UK insurers generally offer two main types of whole of life insurance. While both give you lifelong cover, they have a different approach to how premiums work and the level of cover you get for your money.

Balanced Cover (Premiums)

With this option, everything is straightforward. Your premiums are fixed for the life of the policy, and so is the amount of cover. It's designed for predictability, so you and your family know exactly what to expect from start to finish. It’s a popular choice for leaving a fixed financial gift or making sure final expenses are taken care of.

Maximum Cover (Reviewable Premiums)

This type of policy often starts with lower monthly payments for a large amount of cover. However, the insurer will review your premiums at regular intervals, usually every five or ten years. Based on factors like your age and the insurer's investment performance, your premiums are likely to increase over time if you want to keep the same level of cover. It can make things more affordable at the start, but much less predictable down the road.

By understanding these fundamental differences, you can see how whole of life insurance can be used as a strategic tool for legacy planning, rather than just a temporary safeguard.

The Real-World Benefits of Lifelong Financial Cover

Deciding on a life insurance policy that lasts your entire life is a significant decision. It’s usually driven by the desire to give your loved ones a permanent financial safety net. The biggest selling point of whole of life insurance is its guarantee: as long as you keep up with your premiums, your beneficiaries are certain to receive a payout. This removes the guesswork, unlike temporary cover, and gives you a solid foundation for long-term financial planning.

Unlike term insurance, which expires after a set period, a whole of life policy becomes a permanent financial asset. This makes it the perfect tool for goals that don’t have an expiry date, like leaving an inheritance or ensuring funeral costs are handled. The peace of mind that comes from knowing this protection is locked in for good is one of its most powerful draws.

A Cornerstone of Estate Planning

In the UK, one of the smartest ways people use whole of life insurance is for estate planning, especially when it comes to dealing with Inheritance Tax (IHT). When you pass away, your estate—everything you own from property to savings—can be hit with a 40% tax bill on its value above a certain threshold. This can be a huge financial headache for your family, sometimes even forcing them to sell assets like the family home just to pay HMRC.

This is where a whole of life policy truly shines. It can be set up to pay out a lump sum that matches the expected IHT bill. By placing the policy in a trust, the payout stays completely separate from your estate, meaning it isn't taxed itself. Your family can then use this money to pay the tax bill directly, keeping the assets you worked so hard for exactly where you wanted them.

Example: Let's say your estate is valued at £825,000. That could trigger an IHT bill of around £200,000. A whole of life policy with £200,000 of cover, written into a trust, would provide the exact funds needed to clear that debt. Your children could then inherit your home and other assets without any financial pressure.

Providing for Final Expenses and Leaving a Legacy

Beyond the complexities of estate planning, many people choose whole of life insurance for simpler, but equally important, reasons. The fact that it’s competitive to pay out makes it ideal for covering costs that are also competitive to happen.

- Covering Funeral Costs: The average cost of a funeral in the UK can run into thousands of pounds. A whole of life policy gives your family immediate access to funds to cover these costs, so they don't have to find the money themselves during an already difficult time.

- Leaving a Financial Gift: A policy is an excellent way to leave a tax-free lump sum to your children or grandchildren. It could be the deposit for their first house, help with university fees, or just a financial head start in life.

- Supporting a Lifelong Dependent: For parents of a child with additional needs, a whole of life policy can be a lifeline. The payout can fund a specialist trust that provides financial support long after you’re gone, ensuring their care is always secure.

The predictable and permanent nature of this insurance makes it a rock-solid way to make sure these final wishes are fulfilled. Of course, there are plenty more advantages, and you can explore the 5 benefits of life insurance in our other guide to learn more.

The Potential for Surrender Value

One of the unique features of some whole of life policies is the ability to build up a surrender value (sometimes called a cash-in value) over the years. A small portion of each premium you pay is put into an investment pot that grows at a rate set by the insurer.

After the policy has been running for a good number of years, this cash value can be accessed if you decide you no longer need the cover and want to "surrender" it. While you'll likely get back less than you've paid in during the early years, it does offer a bit of financial flexibility later on. It's really important to remember, though, that surrendering your policy means your life cover ends completely. It's a significant decision and one you should discuss with a financial adviser first.

Choosing Your Path: Whole of Life vs Other Policies

Finding the right life insurance can feel like navigating a maze. The good news is, once you understand the key differences between the main types of policies, the path forward becomes much clearer. While whole of life insurance offers a permanent solution, it’s just one of several popular options in the UK, each designed for different life stages and financial goals.

By putting these policies side-by-side, you can quickly see where whole of life fits into the picture. It's not about finding a single "best" policy, but about figuring out which one makes sense for you and your family.

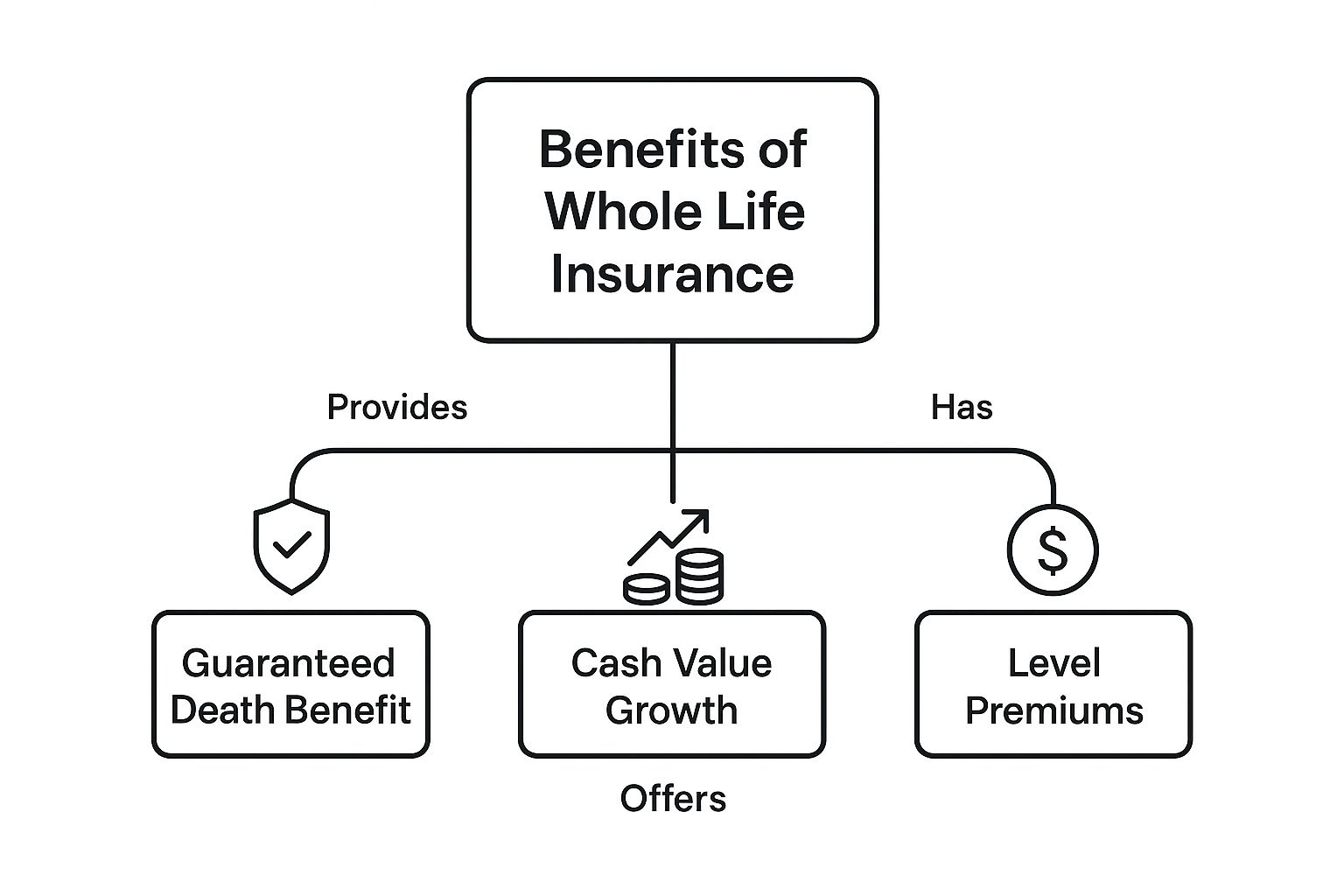

This infographic sums up the core benefits that make whole of life insurance stand out.

As you can see, it's the combination of a competitive payout, fixed premiums, and the potential for cash value growth that makes it such a stable, lifelong financial tool.

Comparing The Core UK Policies

Let’s keep things simple. We'll break down how whole of life cover stacks up against two other major policy types: term life insurance and over-50s plans. Each one has a very different job to do.

Term life insurance is the most straightforward type of cover. It’s designed to protect your loved ones for a fixed period—say, 25 years while you’re paying off the mortgage or while the children are growing up. If you pass away within that "term," your family gets a payout. If you outlive it, the policy simply expires.

Over-50s plans, on the other hand, are a specific type of whole of life cover. They offer competitive acceptance to UK residents aged 50-85 with absolutely no medical questions asked. The trade-off? The payout is usually much smaller, typically just enough to help with funeral costs or leave a small gift.

The crucial difference boils down to purpose and permanence. Term cover is for temporary needs, while whole of life and over-50s plans are for leaving a competitive sum, no matter when you pass away.

For a deeper dive into this key comparison, you can read our detailed guide on whole life vs term insurance to explore all the nuances.

A Head-To-Head Comparison

This table gives you an at-a-glance view of the main differences you’ll find when comparing quotes and policy features from UK insurers like Aviva, Legal & General, or Royal London.

Whole of Life vs Term Life vs Over-50s Plans: A UK Comparison

| Feature | Whole of Life Insurance | Term Life Insurance | Over-50s Life Plan |

|---|---|---|---|

| Cover Duration | Lifelong. | Fixed term (e.g., 10, 20, 30 years). | Lifelong. |

| Payout Certainty | Guaranteed (as long as premiums are paid). | Only pays out if death occurs during the term. | Guaranteed (after an initial waiting period, usually 1-2 years). |

| Typical Purpose | Inheritance tax planning, leaving a legacy, lifelong dependents. | Covering a mortgage, replacing income, family protection. | Covering funeral costs or leaving a small gift. |

| Premiums | Higher, but often fixed for life. | Lower and fixed for the term. | Fixed, but you could pay in more than the payout amount. |

| Medical Info | Full medical underwriting is usually required. | Full medical underwriting is usually required. | No medical questions (competitive acceptance). |

| Surrender Value | Can build a surrender value over many years. | No cash value. | No cash value. |

As you can see, the right choice depends entirely on what you're trying to achieve. One isn't inherently better than the other; they're just different tools for different jobs.

Real-World Scenarios

Let's look at how these differences play out in real life.

For the New Homeowner: A couple in their 30s taking out a 30-year mortgage would likely find decreasing term insurance a perfect fit. The cover amount shrinks over time, roughly in line with their mortgage balance, making it a cost-effective way to ensure their home is safe.

For the Legacy Planner: Someone in their 60s with a significant estate might choose whole of life insurance to cover a future Inheritance Tax bill. The competitive, tax-free payout (when placed in a trust) ensures their beneficiaries can inherit their full legacy without having to sell off assets.

For the Funeral Planner: An individual over 50 who just wants to ensure their funeral expenses are covered without burdening their family could opt for an over-50s plan. The competitive acceptance and smaller, fixed premiums make it an accessible way to lock in a modest lump sum.

While weighing up your insurance needs, it's also a good idea to explore other types of financial protection like Long Term Disability Insurance to get the full picture of what's available to secure your financial future. Each product plays a unique role in building a solid financial plan.

Is Whole of Life Insurance Right for You?

Whole of life insurance is a powerful financial tool, but it isn't the right fit for everyone. The higher premiums mean you need a very specific reason to choose it over something more straightforward like term insurance. The key is knowing when its strengths, particularly the competitive lifelong cover and legacy planning capabilities, perfectly match your financial goals.

To understand this better, let's look at a few real-world situations where whole of life insurance truly shines.

Solving an Inheritance Tax Headache

Picture a successful business owner in her late 60s. Her estate, which includes the family home and her company, is worth significantly more than the UK's Inheritance Tax (IHT) threshold. Her main goal is to pass these assets to her children without them being landed with a massive tax bill from HMRC.

- The Problem: Without a plan, her estate could be hit with a 40% tax on its value above the tax-free allowance. This might force her children to sell off parts of the business or even the family home just to pay the bill.

- The Solution: She takes out a whole of life insurance policy with a payout that matches her estimated IHT liability and places the policy inside a trust.

- The Outcome: When she passes away, the policy pays a tax-free lump sum directly to her children as beneficiaries of the trust. They can use this cash to settle the IHT bill completely, ensuring the assets she worked so hard for are passed down intact.

Securing a Dependent’s Long-Term Future

Now, think about a couple in their 40s with a child who has additional needs. Their biggest worry is what will happen to their child and who will provide for their care when they're no longer around.

- The Problem: Their child will need lifelong financial support for specialised care, housing, and day-to-day living. A standard term policy could expire long before that need for financial protection disappears.

- The Solution: They purchase a joint whole of life insurance policy. The payout is designated to fund a specialist trust that will be managed by a guardian or trustee they've chosen.

- The Outcome: No matter when the parents pass away, the policy guarantees a substantial, tax-free sum will be there to fund the trust. This provides incredible peace of mind, knowing their child's future care is financially secure.

The Over 50s and Peace of Mind

In the UK, these policies are especially popular with the over-50s demographic. At this stage in life, people are often thinking less about covering temporary debts like a mortgage and more about finalising their financial legacy. For many, this simply means covering funeral costs or leaving a small but competitive inheritance.

Market reports consistently show this demographic has a keen interest in lifetime cover. One study found that while 78% of UK individuals over 50 have some reservations about competitive acceptance policies, a significant 62% still recognise the clear benefits of having lifelong cover. You can learn more about these over-50s insurance trends and what consumers are thinking.

For this group, the main draw of whole of life insurance is its reliability. It’s a straightforward, competitive way to leave a financial gift, handle final expenses, and ensure they don't leave a financial burden behind for their loved ones.

How Insurers Calculate Your Premiums

Affordability is a huge factor in any financial decision, and **whole of life insurance** is no different. Insurers in the UK don’t just pick a number out of thin air; they use a detailed process called underwriting to determine the level of risk you present and what your monthly premium should be.

A life insurer assesses your personal circumstances to calculate a fair, personalised price for your lifelong cover.

Key Factors That Influence Your Quote

Several core factors have a big impact on the final cost of your premiums. Understanding these helps you see why getting cover earlier in life can be such a smart financial move.

- Your Age: This is the biggest factor. The younger you are when you take out a policy, the lower your premiums will be. Insurers see younger applicants as lower risk, and with whole of life cover, that lower premium is usually locked in for good.

- Your Health: You’ll be asked detailed questions about your medical history, including any pre-existing conditions like diabetes or heart issues. Insurers need a clear picture of your overall health to assess the risk accurately.

- Your Lifestyle: Habits like smoking or heavy drinking can significantly increase your premiums. A smoker can often expect to pay nearly double what a non-smoker would for the same amount of cover.

- Your Occupation and Hobbies: If your job is considered high-risk (like working at height) or you enjoy adventurous hobbies (like rock climbing), this might also be factored into your premium calculation.

The Amount of Cover You Need

The size of the competitive payout you want for your family directly affects the cost. A policy designed to provide a £50,000 lump sum for funeral costs will be far than one providing £300,000 to clear a hefty Inheritance Tax bill.

The goal is to find a balance between the financial protection your loved ones need and a monthly premium that you can comfortably afford for the long term. This is where getting a clear picture of your finances is vital. You can get an idea of potential costs by using a whole of life insurance calculator to play around with different scenarios.

The UK's life insurance market is a major pillar of the nation's financial services sector, managing assets of around £1.91 trillion. With the market expanding by 7.1% last year alone, insurers are constantly refining how they assess risk to offer competitive pricing in a growing industry.

The real power of whole of life insurance premiums is that they are almost always competitive. While they start higher than term insurance, that fixed cost gives you absolute certainty for your budget. It protects you from future price increases, no matter how your health changes down the line. This predictability is a cornerstone of its value for long-term financial planning.

How Do You Find the Right Whole of Life Policy?

Deciding to get your affairs in order is the first big step. The process of finding whole of life insurance doesn't have to be complicated. It's simply a case of breaking it down into manageable chunks to find a policy that genuinely fits your goals.

First, you need to be clear on your needs. Ask yourself: what's the main purpose of this cover? Are you looking to settle a future Inheritance Tax bill, ensure a dependent is looked after, or just leave a competitive gift? Your answer will shape the amount of cover you need.

Working Out What You Can Afford and Comparing Quotes

Once you have a cover amount in mind, it's time to consider affordability. Whole of life premiums are a long-term commitment, so it's vital to choose a monthly payment that you can manage comfortably. This is precisely where comparing quotes becomes so important.

Different UK insurers will offer different prices for the exact same level of cover, based on their own unique way of assessing risk. By getting quotes from a few different providers, you get a real sense of the market and can quickly spot who is offering the most competitive price for your circumstances.

The UK life insurance market is highly active, which shows how many people are seeking this kind of protection. To give you an idea, the Financial Conduct Authority (FCA) reported that in Q1 2025 alone, roughly 452,799 policies were sold, with premiums adding up to about £13.85 billion. You can discover more insights about these life insurance sales data from the FCA.

Checking the Fine Print and FCA Protection

Before you commit, always read the policy documents carefully. Pay close attention to:

- The type of cover on offer (is it balanced or maximum?).

- Whether the premiums are competitive or reviewable.

- Any rules or exclusions around the surrender value.

It's also worth remembering that all UK insurers are regulated by the Financial Conduct Authority (FCA). This provides peace of mind, knowing that they must treat you fairly and adhere to strict rules.

By taking a sensible, step-by-step approach—figuring out your needs, shopping around for quotes, and then checking the details—you can confidently find the right whole of life insurance policy for you and your family.

Frequently Asked Questions

Stepping into the world of whole of life insurance can bring up a few questions. To help clear things up, here are some straightforward answers to the queries we hear most often.

Can I cash in my whole of life insurance policy early?

Yes, you often can. Most UK whole of life policies build up a 'surrender value' over the years. If your policy has this feature, you can choose to surrender it and take the cash. However, especially in the early years, the amount you get back is often less than what you’ve paid in premiums. Cashing in also means your life cover stops completely.

Are whole of life insurance payouts taxable?

Generally, the lump sum payout from a life insurance policy is paid free of tax. However, that money then becomes part of the deceased's estate and could be subject to Inheritance Tax if the estate's total value is above the UK threshold. The common way to avoid this is to place the policy in a trust, which legally separates it from your estate. We always recommend getting professional financial advice on this.

What happens if I stop paying my premiums?

If you stop paying your premiums, the policy will almost certainly lapse. This means your cover ends, and your loved ones won't get a payout when you pass away. Some insurers offer flexibility, like a 'premium holiday' or the option to reduce your cover for a lower premium. If you're struggling to make payments, your first step should be to call your insurer to see what they can offer.

Is whole of life insurance the same as an over-50s plan?

They are similar as they both offer cover for the rest of your life, but they are very different products. Whole of life insurance usually requires a full medical application and can offer very large amounts of cover, making it ideal for inheritance tax planning. Over-50s plans typically offer competitive acceptance with no medical questions, but the cover amounts are much smaller, usually just enough to help with funeral costs.

Ready to explore your options and find a policy that gives you and your family lasting peace of mind? At Discount Life Cover, our expert advisors are here to help you compare quotes from leading UK insurers.

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply