When you hear people talk about mortgage insurance vs life insurance, it's easy to get them mixed up, but they solve completely different problems. At its core, the main difference is straightforward: mortgage insurance is designed to cover your monthly mortgage payments for a while if you can't work, whereas life insurance is there to pay off the entire mortgage if you pass away.

One is a temporary safety net for your income; the other is a permanent solution to secure your home for your family.

Protecting Your Home and Family

Getting a mortgage is one of the biggest financial steps you’ll ever take. It's exciting, but that responsibility can feel heavy. It's only natural for homeowners across the UK to start thinking about how to protect that huge asset for their loved ones. This is where the whole mortgage insurance vs life insurance conversation kicks off, but it's crucial to realise they aren’t just different versions of the same thing.

In the UK, what most people call "mortgage insurance" is actually Mortgage Payment Protection Insurance (MPPI). Think of it as a short-term financial backstop. If you’re hit by an unexpected event and can’t work, this policy will cover your mortgage payments for a set period, usually 12 to 24 months.

It typically kicks in for two main reasons:

- An accident or sickness that stops you from being able to do your job.

- Involuntary redundancy, giving you breathing room if you're unexpectedly let go.

On the other hand, the go-to life insurance product for protecting a standard repayment mortgage is decreasing term life insurance. This policy is built to pay out a single, tax-free lump sum if you were to pass away during the policy's term. The amount of cover is designed to shrink over time, staying roughly in line with your outstanding mortgage balance. If you want to dig a bit deeper, it's worth reading up on What is Mortgage Insurance and how it really works.

As you can see, these two policies are designed for completely different scenarios. MPPI is there to help you stay afloat while you get back on your feet. Life insurance is about making sure your family can clear the debt entirely and keep their home without you. Grasping that fundamental difference is the first step in building a solid financial plan. Our own mortgage protection insurance comparison can help you weigh up the specific options available.

Mortgage Insurance vs Life Insurance At a Glance

To make things clearer, here’s a quick side-by-side look at how these two types of cover stack up against each other. It really highlights the different roles they play.

| Feature | Mortgage Payment Protection Insurance (MPPI) | Decreasing Term Life Insurance |

|---|---|---|

| Primary Purpose | Covers monthly mortgage payments if you cannot work. | Pays off the outstanding mortgage balance on death. |

| Payout Trigger | Inability to work due to accident, sickness, or redundancy. | Death or diagnosis of a terminal illness. |

| Payout Type | Monthly instalments paid directly to you. | One-time, tax-free lump sum paid to beneficiaries. |

| Cover Duration | Typically pays out for 12–24 months per claim. | Runs for the full term of your mortgage (e.g., 25 years). |

Ultimately, one helps you through a crisis, while the other protects your family after a crisis. They aren't mutually exclusive; for some people, having both might even be the right call.

How Mortgage Payment Protection Insurance Works

Think of Mortgage Payment Protection Insurance (MPPI) as a temporary financial safety net. It’s built for one specific job: to cover your monthly mortgage payments if something stops you from working. This isn't about paying off the whole mortgage; it's about protecting your income stream from a sudden shock so you don't fall behind on your biggest bill.

The way it works is pretty straightforward. You make a successful claim, and the policy pays a fixed monthly amount directly to you. You then use that money to pay your lender, which keeps your home safe and your credit score intact while you get back on your feet.

Because these policies are so important, they're regulated by the Financial Conduct Authority (FCA). This oversight ensures that insurers are upfront about what's covered—and what isn't—so you can make a properly informed choice.

Triggers and Deferral Periods

Don't expect an MPPI policy to pay out the day you stop working. There's a built-in waiting time, known as a deferral period, before any money comes your way. This is a timeframe you agree on upfront, and it kicks in from your first day off work.

Common deferral periods are usually:

- 30 days

- 60 days

- 90 days

Opting for a longer deferral period often means you'll pay a lower monthly premium. The trade-off is that you'll need to cover a longer initial spell with your own savings or company sick pay. Once this period is over, the insurer's payments start and typically continue for a set term, often 12 or 24 months.

Imagine a self-employed plumber who injures their back and can't work for six months. With a 30-day deferral period, they’d have to find the money for the first month's mortgage themselves. After that, the MPPI policy would kick in and cover the next five months of payments, giving them crucial breathing room during recovery.

Common Exclusions and Eligibility

When weighing up mortgage insurance vs life insurance, understanding the small print is vital. MPPI policies always have specific exclusions you need to know about. Generally, you won't be covered for:

- Pre-existing medical conditions you already knew about when you took out the policy.

- Voluntary redundancy or getting fired for misconduct.

- Illnesses like stress, anxiety, or back pain unless there's clear medical evidence.

To be eligible, you usually need to be a UK resident aged between 18 and 65 and be in work for a minimum number of hours per week. Always read the policy documents from cover to cover to make sure you tick all the boxes. It's easy to get an MPPI quote to find out what's available for your specific situation.

How Decreasing Term Life Insurance Works

While MPPI steps in to cover your monthly mortgage payments, decreasing term life insurance has a much bigger job: it's designed to wipe out your entire mortgage debt if you pass away. It’s the go-to life cover for anyone with a repayment mortgage, and for a very good reason. The policy is cleverly built to mirror your outstanding loan.

As you chip away at your mortgage each month, the amount you owe the bank goes down. At the same time, the potential payout from your insurance policy also reduces. This smart alignment is exactly why it’s called ‘decreasing term’ cover. Its main goal is simple—to make sure your loved ones can pay off the mortgage and stay in their home without any financial stress.

Because the potential payout shrinks over time, the insurer's risk also drops. This makes premiums for decreasing term policies more affordable than level term alternatives, where the payout amount stays the same. You can get the full rundown in our detailed guide on what is decreasing term life insurance.

Aligning Cover with Your Mortgage

The defining feature of this policy is its direct link to your mortgage. The policy's term—say, 25 or 30 years—is set to match the length of your mortgage. If you were to pass away during that time, your family would receive a lump sum that should be enough to clear whatever is left on the loan.

Key Takeaway: The payout from a decreasing term policy is meant to cover the capital you still owe on your mortgage, not any missed payments or arrears. It's vital to get the initial cover amount right so it tracks your loan balance accurately from the start.

Let's look at an example. Imagine a couple takes out a £250,000 mortgage over 30 years. They also arrange a decreasing term life policy for the same amount and term. Fast forward 15 years, and their outstanding mortgage has dropped to around £140,000. If one of them passed away at that point, the policy would pay out roughly £140,000, allowing the surviving partner to clear the debt completely.

Affordability and Financial Security

Here in the UK, having life insurance to back up your mortgage is a cornerstone of responsible financial planning. With economic uncertainty and fluctuating interest rates, its importance is only growing. With mortgage payments taking up a significant portion of a typical household's income, having life insurance in place is an essential part of keeping your finances secure.

This type of cover is especially popular with:

- Young families who need to protect their home but are working to a budget.

- First-time buyers looking for a cost-effective safety net.

- Anyone with a repayment mortgage whose main goal is clearing that debt, rather than leaving a separate inheritance.

When you're weighing up mortgage insurance vs life insurance, the decreasing term option stands out as a targeted, affordable solution built specifically for homeowners. For even more robust protection, many people also add critical illness cover to their policy. This pays out a lump sum if you're diagnosed with a specified serious illness, giving you another layer of financial defence.

Side-By-Side Comparison of Coverage Payouts and Costs

To really get to the heart of the mortgage insurance vs life insurance debate, you have to look closely at what each policy actually does and what it will set you back. While both are designed to protect your home, they work in completely different situations and have very different financial setups. One acts as a short-term safety net for your income, while the other is a long-term solution to clear your biggest debt.

This difference is more important than ever. With the total value of UK home loans reaching staggering figures and the cost of living on the rise, protecting that mortgage has become a top priority for many families.

Trigger Events and Payouts

The biggest and most fundamental difference is what actually has to happen for the policy to pay out, and how that money is delivered.

Mortgage Payment Protection Insurance (MPPI) is your backup plan for temporary setbacks. It kicks in if you can’t work because of an accident, sickness, or if you’re made redundant through no fault of your own. The payout is a monthly sum, paid directly to you, to cover your mortgage payments for a set period, usually 12 to 24 months.

Decreasing Term Life Insurance, on the other hand, is for the worst-case scenario. It pays out a single, tax-free lump sum if you pass away or are diagnosed with a terminal illness during the policy's term. Crucially, this money goes to your family or whoever you nominate, not the bank, giving them the choice to pay off the mortgage or use the funds where they're needed most.

Think of it like this: MPPI is there to protect your income stream and keep the bailiffs from the door. Life insurance is there to secure the home itself for your family’s future. One helps you get through a storm; the other provides a permanent roof over their heads after you're gone.

Comparing Costs and Value

Putting a price on these two is tricky because they offer completely different kinds of value. An MPPI policy might cost you somewhere in the region of £20-£40 per month to cover a standard mortgage payment, but remember, this is for short-term help.

By contrast, a decreasing term life insurance policy for a healthy 30-year-old with a £250,000 mortgage over 25 years could be as little as £8-£12 a month. The lower price reflects the fact that a claim is less likely, but the potential payout is obviously far, far larger. For a proper look at what goes into these prices, our guide on how much life insurance costs in the UK breaks it all down.

To make things clearer, let’s lay out the key differences side-by-side.

Key Differences Between MPPI and Life Insurance

Here’s a feature-by-feature comparison to help you see which policy might be the right fit for your circumstances.

| Criteria | Mortgage Payment Protection Insurance (MPPI) | Life Insurance (Decreasing Term) |

|---|---|---|

| Trigger Event | Inability to work (accident, sickness, redundancy) | Death or terminal illness |

| Payout Type | Monthly instalments to the policyholder | One-off lump sum to beneficiaries |

| Policy Duration | Short-term cover (e.g., 1-2 years per claim) | Long-term (matches the full mortgage term) |

| Beneficiary | You, the policyholder | Your nominated family or estate |

| Primary Goal | To cover monthly payments during a crisis | To pay off the entire outstanding mortgage |

Ultimately, choosing between them—or even deciding you need both—comes down to your own personal circumstances and figuring out what financial risks you need to cover.

Choosing the Right Policy for Your Situation

Figuring out whether to go for mortgage insurance vs life insurance isn't just a tick-box exercise. It's about looking at your life, your family, and what keeps you up at night. Your financial situation plays a huge part, especially when you consider how mortgage rates impact buying power.

Let's walk through a few real-life scenarios to see which cover makes the most sense.

Young Couple with Children

If you're a young couple with children, your main priority is almost always long-term stability. The thought of what would happen if one of you weren't around anymore is terrifying. The surviving partner would be left juggling grief, raising a family, and paying off a massive mortgage on their own.

In this case, decreasing term life insurance is a must-have. A lump-sum payout could wipe the mortgage clean, making sure the family home is safe and sound. While MPPI might help if someone loses their job, it's a sticking plaster for a much bigger potential problem. A smart approach could even be combining both for a truly solid safety net.

Single Homeowner

For a single person who owns their home, the worries are different. You might not have dependants to leave the property to, but you do have yourself to think about. What happens if you can't work due to illness or redundancy?

This is where Mortgage Payment Protection Insurance (MPPI) really shines. It's designed for exactly this situation, stepping in to cover your monthly payments so you don't fall behind. Life insurance is less of a priority here unless you have other people relying on you or you specifically want to leave your home to someone as an inheritance.

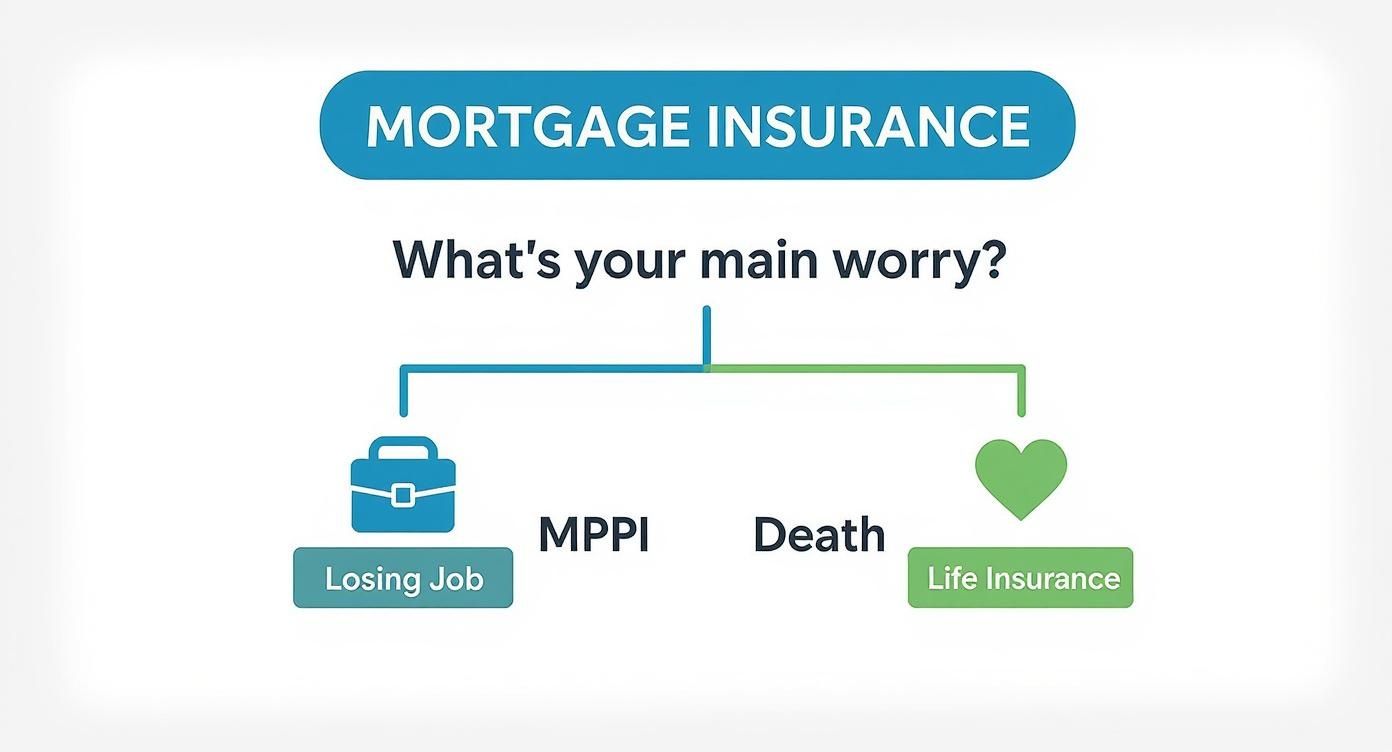

This decision tree breaks down the core choice. It all comes down to what you're most concerned about: losing your income or leaving your loved ones with a debt.

As you can see, MPPI is your income shield, while life insurance is about securing the property itself for others.

Self-Employed Individual

Being self-employed means you're the master of your own destiny, but it also means you don't have an employer's sick pay to fall back on. An illness or injury can quickly turn into a financial crisis.

For anyone self-employed, MPPI is a vital piece of the puzzle. Think of it as your personal sick pay policy, making sure your biggest monthly bill is handled while you get back on your feet. Life insurance is still important if you have a family, but protecting your immediate income is the most urgent need.

Key Consideration: The government's Support for Mortgage Interest (SMI) scheme highlights the fragility of relying on state aid. The scheme provides loans, not grants, which must be repaid with interest when you sell your home. It’s a stark reminder of how quickly a mortgage can become a burden without a private safety net like insurance.

Ultimately, there's no single right answer—only what's right for you. Ready to see what that looks like? Request a personalised quote from DiscountLifeCover and let's find the protection that fits your life.

Frequently Asked Questions

When you're weighing up mortgage insurance and life insurance, a few common questions always seem to pop up. Let's tackle them head-on.

Do I have to take the mortgage insurance offered by my lender?

Absolutely not. It's a common misconception, but you are never forced to buy the insurance policy your mortgage lender offers.

In fact, the Financial Conduct Authority (FCA) has strict rules against this. Lenders cannot make their mortgage offer dependent on you taking out their in-house insurance. This practice, known as 'tied selling,' is banned for a good reason – it limits your choice. You have every right to shop around and find a policy that gives you better value and the right level of cover for your circumstances.

Can I have both mortgage insurance and life insurance?

Yes, and for many homeowners, it's actually a very smart move. Having both Mortgage Payment Protection Insurance (MPPI) and a separate life insurance policy gives you a much stronger financial safety net.

They're designed to cover completely different scenarios:

- MPPI is your short-term shield. It covers your monthly mortgage payments if you can't work due to illness, an accident, or being made redundant.

- Life insurance is the long-term guardian. It provides a big lump sum to clear the entire mortgage if you pass away, securing the home for your family's future.

Think of it this way: one protects your income, the other protects your legacy. Together, they offer real peace of mind.

Is critical illness cover the same as mortgage protection insurance?

No, they're two different types of policy, although they both can help during a health crisis.

Critical illness cover pays out a single, tax-free lump sum if you're diagnosed with a serious condition defined in your policy – think heart attack, stroke, or certain cancers. You can use that money for anything you need, whether it's adapting your home, paying for private treatment, or clearing a chunk of the mortgage.

Mortgage Payment Protection Insurance (MPPI), on the other hand, pays a monthly income that's specifically meant to cover your mortgage payments. The trigger isn't a specific diagnosis, but simply being unable to work because of sickness or an injury.

The crucial difference is how and when they pay out. Critical illness cover provides a one-off lump sum based on a specific diagnosis. MPPI provides a monthly income based on your ability to work.

What happens to my life insurance policy once my mortgage is paid off?

This all comes down to the type of life insurance policy you chose in the first place.

If you have a decreasing term life insurance policy, it was likely set up to mirror your mortgage balance. As you paid down the mortgage, the cover amount dropped alongside it. Once the mortgage is cleared, the policy's job is done, and it simply ends. There’s no payout because there’s no debt left to cover.

But if you have a level term life insurance policy, the story is different. The amount of cover stays the same for the entire length of the policy, no matter what your mortgage balance is. Even after you've paid off the house, the policy is still active. If you were to pass away before the term ends, your family would still receive the full payout. At this point, many people keep the cover in place to help with inheritance tax or just to leave a financial gift for their loved ones.

Ready to secure your home and protect your family? The expert team at Discount Life Cover can help you compare quotes from leading UK insurers to find the right cover at the right price. Get your free, no-obligation quote today.

Find your personalised quote at https://discountlifecover.co.uk.

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply