Everyone wants to know the bottom line: how much does life insurance actually cost? The headline figure floating around is about £32 per month for a standard term life policy in the UK. But honestly, that number is just a signpost, not the destination. Your final premium will be as unique as you are, shaped by your age, health, and how much cover you actually need.

What Is the Average Cost of Life Insurance in the UK?

Looking at the average cost is a sensible first step. It gives you a ballpark figure and helps set your expectations before you dive into getting quotes. The key thing to remember, though, is that averages can be a bit deceiving. Your own circumstances are what truly drive the price.

Think of that average figure as a rough guide. It gives you a general idea, but your personal journey—your age, medical history, lifestyle, and the type of policy you choose—will determine the final cost. These factors have a huge impact on the premium you'll be offered.

A Snapshot of Average Monthly Life Insurance Premiums

To give you a clearer picture, recent data from 2024 shows the average monthly premium for a term life insurance policy in the UK was £32.64. This figure is based on a massive pool of policies with a typical payout amount (or 'sum assured') of £160,871.

Of course, this average lumps everyone together—the young and healthy with older individuals or those with health conditions. A younger, non-smoking applicant will almost certainly pay less than this. You can get a much more detailed breakdown in our complete guide on how much life insurance costs per month.

To make this even clearer, here’s a quick overview of what you might expect to pay for different types of cover.

This table gives a rough idea of the monthly costs for some of the most common types of term life insurance policies available in the UK.

| Policy Type | Average Monthly Premium | Typical Use Case |

|---|---|---|

| Level Term Insurance | £25 – £40 | Covering an interest-only mortgage or providing a fixed lump sum for your family. |

| Decreasing Term Insurance | £15 – £30 | Covering a repayment mortgage, as the payout decreases alongside your loan. |

| Over 50s Life Insurance | £20 – £50+ | Providing a smaller, competitive lump sum for funeral costs or leaving a gift. |

As you can see, the type of policy has a direct impact on the price, with decreasing term cover often being the most budget-friendly option.

Key Takeaway: While national averages provide useful context, they are not a substitute for a personalised quote. The only way to find out your true life insurance cost is to get a quote based on your specific details.

At the end of the day, your premium is simply a reflection of the risk the insurer is taking on. In the next sections, we'll break down exactly what factors insurers look at and explain how each one contributes to the final price you're quoted.

The Key Factors That Shape Your Premium

Ever wonder what goes on behind the curtain when an insurer calculates your premium? It’s not a random number plucked from the air; it’s a careful, calculated assessment of risk based on a handful of well-established factors. Each piece of information gives the insurer a clearer picture of your health and life expectancy, which directly influences your final life insurance cost.

Think of it like this: each factor is a dial that an underwriter turns to figure out your risk profile. Some of these dials are fixed, like your age. But others, like your lifestyle choices, are very much in your control. Getting to grips with how these dials work is the first step towards finding the most affordable cover out there.

Your Age and Health Status

Your age is one of the biggest drivers of cost, simply because it's a primary indicator of life expectancy. The younger and healthier you are when you , the lower your statistical risk of passing away during the policy term. This is why insurers can offer much premiums to people in their 20s and 30s than to those in their 50s or 60s.

Your current health and medical history are just as vital. When you , you’ll be asked some fairly detailed questions about your health, including any pre-existing conditions like diabetes, high blood pressure, or heart disease. They'll also want to know about your family's medical history to get an idea of any potential hereditary risks.

A clean bill of health almost always translates to a lower premium. Insurers reward lower-risk applicants with more competitive rates, as they are statistically less likely to make a claim.

The COVID-19 pandemic also had a profound impact on UK life insurance. While the number of new policies taken out dipped at first, the value of payouts rose sharply, with insurers paying out £204 million in 2021 just for COVID-related claims. This surge in claims understandably led some insurers to tweak their pricing in the following years to cover the increased costs. You can read more about the pandemic's effect on insurance rates for a deeper analysis.

Lifestyle Choices and Habits

Insurers are very interested in your day-to-day habits because these choices have a huge impact on your long-term health. The big one, of course, is smoking.

Being a smoker or even a recent ex-smoker can dramatically increase your premiums—we're often talking double the price, or even more. This is purely down to the well-documented health risks that come with tobacco and nicotine use. Most insurers will class you as a non-smoker if you’ve been completely nicotine-free for at least 12 months.

Beyond smoking, a few other lifestyle factors come into play:

- Alcohol Consumption: Your weekly alcohol intake will be reviewed. Drinking heavily can lead to higher premiums because of the associated health risks.

- Body Mass Index (BMI): Your height and weight are used to calculate your BMI. A BMI that falls outside the healthy range can result in higher costs.

- Dangerous Hobbies: If you're into high-risk activities like rock climbing, scuba diving, or private aviation, you might face an increased premium or even specific exclusions on your policy.

Occupation and Financial Details

Your job also plays a part. If you work in a high-risk profession—think construction, offshore oil and gas, or the armed forces—insurers may see you as a higher risk. This doesn't mean you can't get cover, but it might just come at a higher price.

Finally, the policy details you choose are fundamental to the cost. These are the elements you have direct control over when you’re building your quote. Getting these right is essential, as small adjustments can make a big difference. Our guide to term life insurance rates explores how these choices affect your final price in much more detail.

The three main policy choices that shape your cost are:

- The Sum Assured: This is the total payout amount. A larger sum assured, like £500,000, will naturally cost more than a smaller one of £100,000.

- The Policy Term: This is how long your cover lasts. A 30-year term will be more expensive than a 15-year term for the same person.

- The Policy Type: As we saw earlier, a decreasing term policy is usually than a level term policy because the payout amount reduces over time.

By understanding these key factors, you move from being a passive buyer to an informed consumer, ready to find a policy that truly fits your needs and your budget.

Comparing the Main Types of Life Insurance Policies

Not all life insurance is created equal. Understanding the different types available in the UK is a must, as the structure of your policy has the biggest impact on both your cover and your long-term life insurance cost. Think of it like picking a vehicle for a specific journey; one might be perfect for a short trip, while another is built for the long haul.

This section will walk you through the main policy types, putting them side-by-side to help you see which one fits your family's needs. We'll break down the most common options—Level Term, Decreasing Term, and Whole of Life insurance—explaining how they work and who they're really for. We'll also touch on some popular add-ons that can beef up your protection.

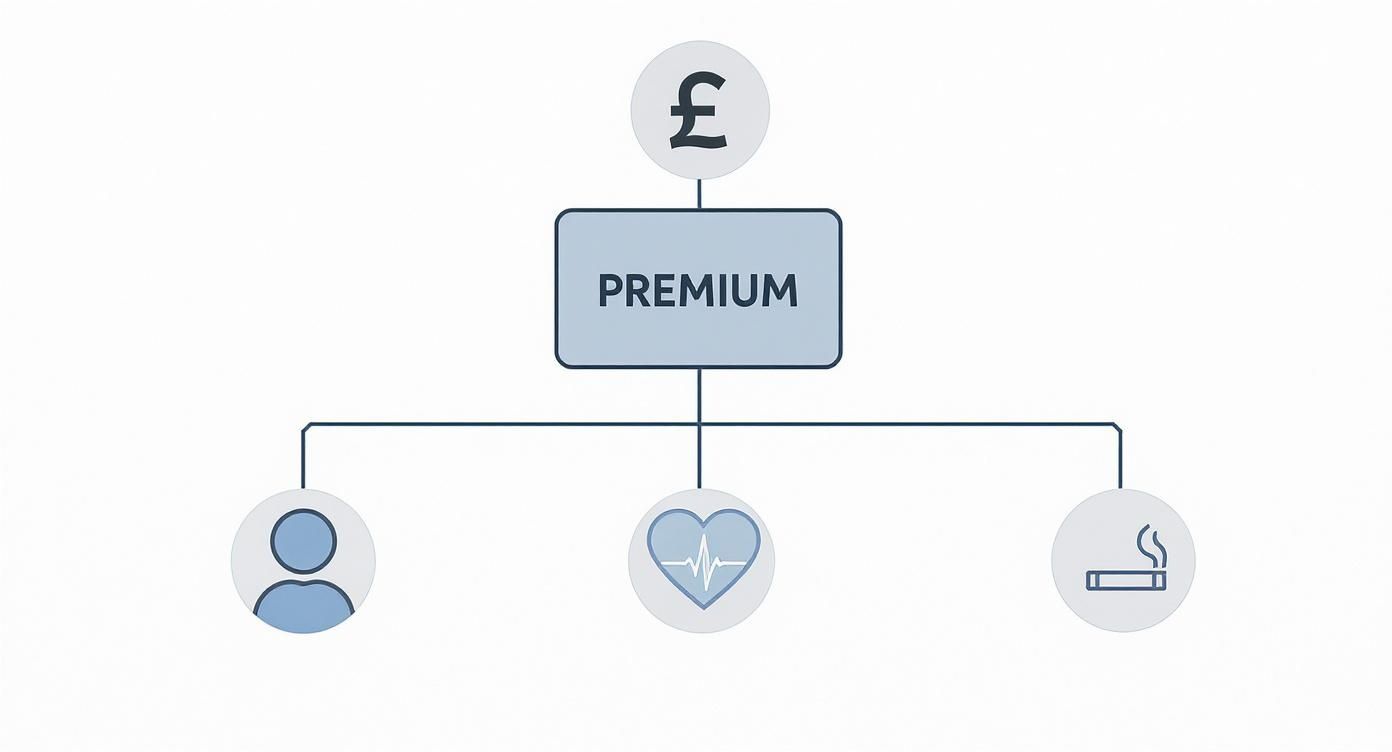

This infographic gives a great visual breakdown of what goes into your premium. As you can see, your age, health, and lifestyle are the big three.

These are the core ingredients insurers use to cook up your final quote, and each one carries a different weight in the final calculation.

Level Term Life Insurance

Level term insurance is probably the most straightforward type of life cover out there. You choose a set payout amount (the sum assured) and a policy length (the term). If you pass away within that term, your loved ones get that fixed lump sum. Simple. Both your monthly premium and your payout amount stay the same—or "level"—for the entire policy.

It's this predictability that makes it such a popular choice for families looking for reliable financial protection.

- Best For: Covering an interest-only mortgage, replacing a lost salary to cover living costs, or leaving a specific inheritance for your children.

- Cost: Generally more expensive than decreasing term cover but than a whole of life policy, because the cover is for a fixed period.

For example, a parent might take out a £250,000 level term policy for 25 years. This ensures their children are looked after financially until they're old enough to stand on their own two feet. The payout stays at £250,000 whether a claim is made in year five or year twenty-four.

Decreasing Term Life Insurance

Often called mortgage life insurance, decreasing term cover is built specifically to cover large repayment debts that shrink over time. Just like a repayment mortgage, the payout amount goes down each year, eventually hitting zero when the policy ends.

Because the potential payout gets smaller over the years, the risk for the insurer also drops. This means decreasing term policies are typically the most affordable form of life insurance you can get.

- Best For: Primarily used to cover a repayment mortgage. It ensures your family can pay off the outstanding loan and stay in the family home if the worst happens.

- Cost: This is usually the cheapest option going, making it a brilliant choice for homeowners on a budget.

Imagine you have a £200,000 mortgage over 30 years. A decreasing term policy would start with a £200,000 payout, but after 15 years, the payout might have dropped to around £100,000, tracking the reduction in your mortgage balance.

Whole of Life Insurance

Unlike term policies that only cover you for a set number of years, a whole of life policy provides cover for the rest of your life. As long as you keep up with the premiums, a payout is competitive when you pass away, whenever that might be.

Of course, this lifelong guarantee comes at a price. Premiums for whole of life policies are significantly more expensive than term insurance because a claim is certain to happen eventually.

- Best For: Covering funeral costs, settling an inheritance tax bill, or leaving a competitive legacy for loved ones.

- Cost: This is the most expensive type of life insurance due to the competitive payout.

Important Note: Due to the higher costs and the investment elements that can be involved, it's often a very good idea to get financial advice before taking out a whole of life policy. It’s a major financial commitment designed for very specific long-term planning.

To make things clearer, let's compare these three side-by-side.

Comparing Level Term, Decreasing Term, and Whole of Life Insurance

| Feature | Level Term Insurance | Decreasing Term Insurance | Whole of Life Insurance |

|---|---|---|---|

| Payout Amount | Stays the same for the whole term. | Reduces over the policy term. | Stays the same and is competitive. |

| Policy Length | A fixed term (e.g., 20, 25 years). | A fixed term (e.g., 25, 30 years). | Lasts for your entire life. |

| Premiums | Remain fixed for the term. | The cheapest option, also fixed. | Significantly higher, can be fixed or reviewable. |

| Best For | Family protection, interest-only mortgages. | Repayment mortgages. | Inheritance tax planning, funeral costs, legacy. |

| Main Benefit | Predictable, fixed cover amount. | Most affordable type of cover. | payout, no matter when you pass away. |

As you can see, the "best" policy really comes down to what you need to protect and how much you're prepared to budget for it.

Enhancing Your Cover with Add-Ons

Many policies let you add extra layers of protection for an additional cost. The most common add-on in the UK is Critical Illness Cover. This pays out a lump sum if you are diagnosed with a specific serious illness listed in the policy, such as some types of cancer, a heart attack, or a stroke.

Adding this will increase your premium, but it provides a financial safety net during your lifetime, helping you cover medical bills or lost income while you recover. It’s a valuable addition that can turn your life insurance into a much more robust financial shield for you and your family.

How Life Insurance Costs Play Out in the Real World

It’s one thing to talk about the different factors that shape the life insurance cost, but it’s another thing entirely to see how it all comes together for real people. To put some real meat on the bones, let’s walk through a few common scenarios for UK families at different stages of life.

These examples are designed to feel familiar, showing you exactly how your personal situation connects to what you’ll pay each month. They aren't set in stone, of course, but they should give you a solid idea of what to expect when you get your own quote.

Example One: First-Time Homebuyers

Let's meet Sarah and Tom. They're both 32, non-smokers, and in good health. They’ve just taken the plunge and bought their first home with a £250,000 repayment mortgage that runs for 30 years. Their biggest worry? Making sure that if one of them passed away, the other wouldn't be left struggling with the mortgage payments.

- Their Goal: To cover their mortgage debt, which shrinks over time.

- Their Best Policy: A joint Decreasing Term Insurance policy for £250,000 over a 30-year term.

- Estimated Monthly Cost: For a healthy, non-smoking couple in their early 30s, a joint policy like this would likely come in between £15 and £25 per month.

This is a textbook case of matching the most cost-effective policy to a specific debt. Because the amount of cover drops in line with their mortgage, the premium stays incredibly low. It’s a cheap and cheerful safety net for new homeowners.

Beyond just the premiums, it's also worth understanding how policies are treated as assets, especially when a property is involved. You can explore the ins and outs of life insurance and its role in property division to learn more about the complexities.

Example Two: Parents Planning for the Future

Now, let's picture David and Chloe, aged 38 and 36. They have two young children, aged 5 and 7. The mortgage is still there, but their main concern is providing for the kids' upbringing and education if the unthinkable were to happen.

They want a policy that pays out a fixed lump sum, something big enough to cover daily living costs, school fees, and maybe even university until their youngest is at least 21.

- Their Goal: To create a financial cushion that replaces lost income and supports the children until they're independent.

- Their Best Policy: A joint Level Term Insurance policy with £300,000 of cover over a 20-year term.

- Estimated Monthly Cost: As non-smokers in good health, their joint premium would probably fall somewhere between £30 and £45 per month.

Why Level Term? The fixed payout is key here. A level term policy guarantees the family gets the full £300,000, no matter when a claim is made. This provides a consistent and reliable financial backstop during those crucial years when the kids are growing up.

Example Three: Securing a Legacy Over 50

Finally, we have Michael. He's a 58-year-old professional, divorced, with grown-up children. His mortgage is paid off, but he wants to leave a competitive sum to his kids. This money would help with any inheritance tax and cover his funeral costs, so his children don't have to find the cash themselves.

He'd rather not go through a medical exam and just wants a simple, competitive acceptance policy.

- His Goal: Leave a fixed lump sum for funeral expenses and a small inheritance.

- His Best Policy: An Over 50s Life Insurance plan.

- Estimated Monthly Cost: For a £10,000 payout, Michael can expect to pay between £40 and £60 per month.

These plans are brilliantly straightforward. However, they tend to offer lower cover for a higher premium compared to term insurance, simply because acceptance is competitive for UK residents aged 50-85, with no health questions asked.

As you can see from these real-world examples, the final life insurance cost is a direct reflection of your personal needs, your health, and the kind of protection you choose.

Actionable Strategies to Reduce Your Life Insurance Cost

Knowing what factors drive up your premiums is half the battle. Now it's time to use that knowledge to actually save some money. The good news is there are several practical, tried-and-tested ways to lower your life insurance cost without having to settle for less cover.

Securing a great policy at a fair price isn't about finding some secret trick. It's simply about making smart, informed choices at the right moments. If you take a proactive approach to your health, your lifestyle, and how you shop around, you can make a real dent in what you pay each month.

Act Early and Prioritise Your Health

Honestly, the single most powerful way to lock in a low premium is to get life insurance while you're young and healthy. Insurers see younger applicants as a much lower risk, and that translates directly into monthly payments. A policy you take out in your late 20s can be dramatically more affordable than the exact same one bought in your 40s.

Getting healthier before you can also make a huge difference. If your BMI is on the high side or your blood pressure is a little elevated, working on those numbers could lead to a much better offer from insurers. Even small, positive tweaks to your diet and exercise regime can pay off big time.

Quit Smoking for Big Savings

If you smoke or use any nicotine products, quitting is the biggest financial win you can possibly get on your life insurance. Smokers can easily expect to pay at least double what non-smokers do for the same amount of cover. It's a massive difference.

Insurers will typically re-classify you as a non-smoker once you’ve been completely nicotine-free for at least 12 months. That includes vaping and nicotine replacement therapies. Hitting that one-year milestone can literally slice your premium in half.

Choose the Right Policy and Cover Amount

There's no point paying for more cover than you actually need. One of the most common mistakes we see is people buying a level term policy to protect a repayment mortgage, when a much decreasing term policy would do the job perfectly well. Take the time to accurately calculate how much cover your family really needs to avoid over-insuring and overpaying. You can explore our guides to find the cheapest term life insurance options for your specific situation.

Compare Quotes from Multiple Insurers

Whatever you do, never just accept the first quote you're given. Premiums can vary wildly between insurance providers, even for the same person needing the same level of cover. This is just a reflection of how large and competitive the UK's insurance market is.

Using a comparison service or an independent broker is hands-down the most efficient way to see what's on offer from a wide range of insurers. It ensures you find the absolute best deal out there for you. This one simple step could save you hundreds, if not thousands, of pounds over the life of your policy.

So, What Are Your Next Steps?

Trying to understand life insurance costs can feel a bit like guesswork, but it all comes down to one simple truth: the price is completely personal to you. While average costs give you a rough idea, it’s the details—your age, health, lifestyle, and the type of policy you choose—that really determine what you’ll pay.

The most important thing to remember is that getting affordable, effective cover is genuinely within reach for most of us. With a bit of know-how, you can find a policy that protects the people you care about without blowing your budget. The trick is to stop thinking about it and start doing something. The only way to find out your actual cost is to get a quote based on your specific situation.

Get Your Personalised Quote Today

Now you know what shapes the price, you can take the next step with confidence. Comparing quotes is easily the best way to make sure you’re not paying over the odds for your cover. At Discount Life Cover, we've made the whole process quick and painless.

Using our free comparison tools, you can:

- See prices from the UK's top insurers side-by-side in just a few minutes.

- Play around with cover amounts and policy types to see how they change your monthly premium.

- Chat with an expert adviser if you get stuck or need a bit of guidance on your options.

Don’t leave your family’s financial future up to chance. Take a couple of minutes today to compare quotes and find a policy that’s a perfect fit for you and your budget.

Frequently Asked Questions About Life Insurance Cost

We've covered a lot of ground, but you might still have a few lingering questions about how life insurance cost works in the real world. Let's tackle some of the most common queries we hear from people all across the UK.

Can My Life Insurance Premiums Go Up Over Time?

This is a great question, and the answer comes down to the specific type of policy you've picked.

- Premiums: Most term life policies, whether they're level or decreasing, come with competitive premiums. This means the price you're quoted is the price you'll pay every single month for the entire life of the policy. It's locked in and will never change.

- Reviewable Premiums: On the other hand, some policies have reviewable premiums. You'll often find these with certain whole of life or over 50s plans. The insurer has the right to take another look at your payments after a set period, usually every five or ten years, and potentially increase them.

It's absolutely vital to know whether your premiums are competitive or reviewable before you sign on the dotted line.

What Happens If I Can't Pay My Premiums Anymore?

If you stop making your monthly payments, your life insurance policy will eventually lapse. In simple terms, this means your cover stops, and your loved ones won't get a payout if you were to pass away.

Insurers usually give you a grace period, often around 30 days, to catch up on a missed payment. But if you don't, the policy is cancelled for good. It's also worth remembering you won't get any of your previous payments back, as that money was used to keep you covered during that time.

Is a Medical Exam Always Needed for Life Insurance?

Not at all. In fact, many UK insurers can make a decision just from the health and lifestyle questions on your application, especially if you're young and in good shape. It's also useful to understand the process after a claim, so it's worth exploring life insurance proceeds and probate considerations.

However, an insurer might ask for a medical check-up if:

- You're ing for a particularly large amount of cover.

- You're older.

- You've mentioned a significant pre-existing medical condition.

Even if they do ask for one, don't worry. The insurer sorts it all out and covers the cost. It's usually just a quick and simple check-up with a nurse.

The best way to get a real feel for your personal life insurance cost is to see the numbers with your own eyes. At Discount Life Cover, you can compare quotes from the UK's top insurers in minutes to find the right protection at the competitive.

Get Your Free, No-Obligation Quote Today

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply