When most people think of life insurance, they picture a safety net that disappears after a certain number of years. Whole life insurance flips that idea on its head. It’s a permanent type of cover designed to stay with you for your entire life, as long as the premiums are paid.

This isn't temporary cover; it’s a lasting financial asset that guarantees a tax-free lump sum payout to your family when you pass away, giving them real security for the long haul.

So, What Exactly Is a Whole Life Insurance Policy?

Think of it this way: term life insurance is a bit like renting protection. You have it for a set period, say 25 years, and then it's gone. A whole life insurance policy is more like buying a financial home—it's yours for good. It’s built to provide certainty in a world full of unknowns.

At its heart, a whole life policy has two key parts working in tandem:

- A Payout: This is the tax-free lump sum your loved ones will receive. The key word here is competitive. It won’t shrink over time, offering predictable peace of mind.

- A 'Cash Value' Component: With each premium you pay, a portion is channelled into a savings-like account. This pot of money grows over the life of the policy, often at a rate set by the insurer, and that growth is tax-deferred.

This two-in-one structure is what really sets it apart. While its main job is to provide protection, that growing cash value adds a layer of financial flexibility that you just don't get with simpler policies like term insurance.

Predictability and Stability

One of the biggest draws of a whole life policy is its unwavering predictability. From the day you take out the policy, your premiums are typically fixed. They will never increase, no matter how old you get or if your health changes down the line.

This makes budgeting incredibly straightforward and removes the worry that your cover might become unaffordable when you need it most. This stability makes it a solid foundation for specific long-term financial plans, like inheritance tax planning or leaving a meaningful legacy.

For instance, a parent might set up a policy to make sure there are funds ready to cover their children's inheritance tax bill, helping to preserve the full value of their estate. You can get a clearer picture of how it stacks up against temporary cover in our guide comparing whole life vs term insurance.

Whole Life Insurance At a Glance

To bring it all together, let's look at the core features of a typical whole life insurance policy in the UK. The table below gives a quick, clear summary of what you're getting.

Understanding these fundamentals is the best first step in figuring out if this type of cover is the right fit for your financial goals.

| Feature | Description |

|---|---|

| Cover Duration | Lifelong cover that lasts for your entire life and does not expire. |

| Premiums | Fixed payments that are competitive not to rise over the policy's duration. |

| Payout | A competitive tax-free lump sum paid to your beneficiaries upon your death. |

| Cash Value | A built-in savings element that grows at a tax-deferred rate. |

| Primary Use | Often used for inheritance tax planning, leaving a legacy, or covering final expenses. |

Essentially, a whole life policy offers a blend of permanent protection and a disciplined way to build a financial asset over time.

How the Cash Value Component Actually Works

One of the defining features of a whole life insurance policy is its built-in savings element, often called the ‘cash value’ or ‘surrender value’. This isn't just an abstract number on a statement; it's a real pot of money that grows over your lifetime, acting as a disciplined, long-term savings plan that runs alongside your life cover.

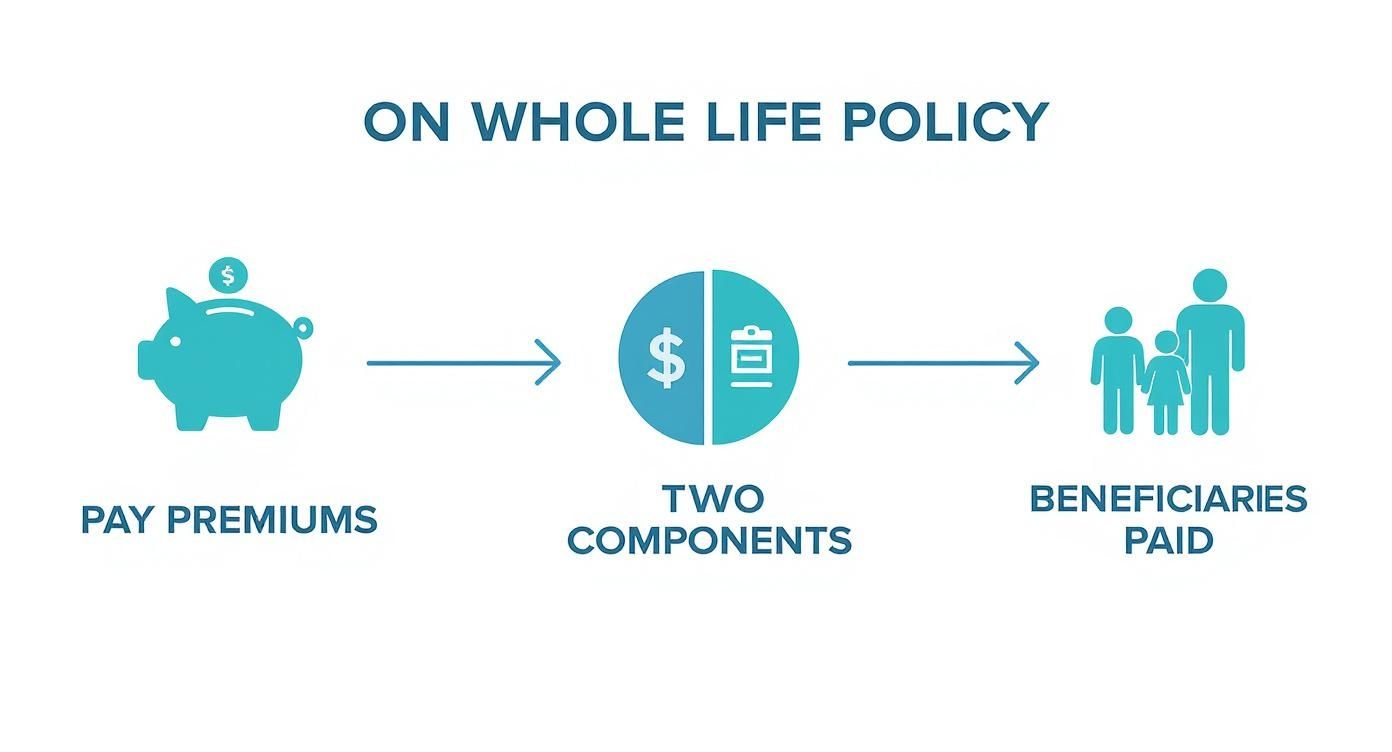

When you pay your premium, whether it's monthly or annually, the insurer splits it into two. One part goes to cover the cost of the life insurance itself—the competitive payout that your family will receive. The other part gets funnelled into a separate pot that builds up your cash value.

This pot grows at a rate set by the insurer, and it does so tax-deferred. Think of it like a savings account where the interest rate is locked in from day one, giving you a predictable and steady way to accumulate wealth over many decades.

This visual guide shows the simple process of how your premiums are split to fund both the payout and the growing cash value.

As you can see, each payment you make feeds both components. They are separate but linked, working together to ensure your beneficiaries receive the final payout when the time comes.

The Slow and Steady Growth

It's really important to realise that building up cash value is a marathon, not a sprint. In the early years of the policy, a bigger chunk of your premium goes towards covering the insurer's setup costs and commissions. This means the cash value grows very slowly at the start.

But as the years roll on, more of your premium gets directed into the cash value component, and the magic of compound growth really starts to kick in. It can often take 10 to 15 years before the cash value becomes a significant sum that you can practically access.

Accessing Your Cash Value

Once you've built up a decent amount of cash value, you have several ways to use it. This flexibility is a key reason why some people choose whole life policies as part of their long-term financial planning.

Typically, you can get to the funds in two main ways:

- Policy Loans: You can borrow against the cash value you've accumulated. The great thing is, this loan isn't subject to credit checks and usually has a pretty favourable interest rate. You're not required to pay it back, but be aware that any outstanding loan amount plus interest will be deducted from the final payout paid to your family.

- Withdrawals or Surrender: You can make a partial withdrawal or just surrender the policy entirely to receive the full cash value. If you surrender the policy, your life cover will end. It's also worth knowing that any gains you receive above the total premiums you've paid might be subject to income tax.

For example, a parent could take out a policy loan to help with university fees, or a retiree might use withdrawals to top up their pension income in their later years. It provides a source of funds for major life events without having to sell other assets. Some policies offer different ways to receive value, and you can explore options like life insurance with cash back to see how various products are structured.

Busting a Common Myth: A frequent misunderstanding is that beneficiaries get both the payout and the accumulated cash value. In reality, the insurer pays out the death benefit, and the cash value is absorbed back by the company. The cash value is a benefit for you, the policyholder, to use while you are alive.

Important Considerations Before Using Your Cash Value

Dipping into your cash value has significant implications that you need to think through carefully. Taking a loan or making a withdrawal will reduce the final payout that your loved ones receive. This could undermine the very reason you took out the policy in the first place—to provide for them financially.

If a loan balance grows too large, it could even cause the policy to lapse, leaving you with no cover at all and potentially a tax bill to deal with. For this reason, it's crucial to treat the cash value as a long-term resource and to fully understand the consequences before accessing it. The Financial Conduct Authority (FCA) requires UK insurers to explain these terms clearly.

Weighing the Pros and Cons of Whole Life Insurance

So, is a whole life insurance policy the right move for you? It's a solid financial tool, no doubt, but it's not a one-size-fits-all solution. To figure out if it fits your long-term plans, you need a clear, balanced view of what it offers and what it asks for in return.

Let's look at both sides of the coin.

There’s a reason these policies are a major player in the UK market. They are especially popular with those planning for the long-term because they offer something incredibly valuable: certainty. You get level premiums that never change and cover that lasts a lifetime.

Even though many people recognise the benefits, it's vital to have a balanced perspective. For a deeper dive into what consumers are thinking, the over-50s life insurance market report is well worth a read.

The Advantages of a Whole Life Policy

The biggest draw of whole life insurance is its permanence and predictability. In a world full of financial uncertainty, it offers a level of assurance that’s hard to find elsewhere.

Here’s a rundown of the key benefits:

- Lifelong Cover That Never Expires: This is the big one. Unlike term insurance that runs out after a set period, a whole life policy protects you for your entire life. As long as the premiums are paid, your beneficiaries are competitive to receive a payout.

- Payout: From day one, you know exactly how much your loved ones will receive. This competitive payout is a game-changer for long-term planning, whether it’s for covering funeral costs or settling an inheritance tax bill.

- Fixed and Predictable Premiums: The price you pay is locked in when you take out the policy and will never go up. This makes budgeting a breeze and protects you from rising costs as you get older or if your health changes.

- Tax-Deferred Cash Value Growth: The cash value pot grows at a competitive rate, and you don’t pay tax on the gains as long as the money stays in the policy. It’s a disciplined, hands-off way to build a financial nest egg over many years.

Real-World Scenario: Picture a family that wants to leave a financial legacy and ensure their estate isn’t hit with a hefty inheritance tax bill. A whole life policy delivers a competitive, tax-free sum exactly when it's needed, allowing their home and other assets to be passed on intact.

The Disadvantages of a Whole Life Policy

Those powerful guarantees don't come for free. The downsides are significant, and it’s crucial to weigh them up before you commit to what is a very long-term financial product.

Here are the main drawbacks to consider:

- Significantly Higher Premiums: The cost is the first thing most people notice. Premiums for whole life are substantially higher than for term insurance—often five to ten times more for the same amount of cover. For many families, that’s simply not affordable.

- Slow Initial Cash Value Growth: Don't expect the cash value to shoot up overnight. It builds very slowly, especially in the first 10 to 15 years. A big chunk of your early premiums goes towards the insurer's costs and commissions, so it takes a long while to build a meaningful pot you can access.

- Lower Returns Than Direct Investing: The competitive growth rate on the cash value is usually quite modest. You could potentially get much better returns by investing the premium difference into the stock market over the long haul. This is the trade-off you make for zero market risk.

- Complexity and Inflexibility: These policies are not simple. Once you're in, making changes can be tricky, and if you decide to surrender the policy early, you'll often walk away with less money than you put in.

Comparing the Advantages and Disadvantages of a Whole Life Policy

Sometimes, the best way to make sense of it all is to see the pros and cons laid out side-by-side. This can help you see clearly whether a whole life policy aligns with your financial goals.

| Advantages | Disadvantages |

|---|---|

| Your cover is permanent and lasts your entire life. | Premiums are much higher than for term life insurance. |

| The payout for your beneficiaries is competitive. | Cash value growth is very slow in the early years. |

| Your premiums are fixed and will never go up. | Returns may be lower than other investment options. |

| It includes a tax-deferred savings component. | Policies can be complex and relatively inflexible. |

Ultimately, it comes down to what you need. If you're looking for temporary cover for a specific debt, like a mortgage, then a more affordable decreasing term life insurance policy is probably a much better fit. But for those with specific estate planning needs, the iron-clad guarantees of a whole life policy can be priceless.

Whole Life Insurance Versus Term Life Insurance

When you start looking into life insurance, it usually boils down to one big question: do you need cover for a set period, or for the rest of your life? This is the fundamental difference between the two main players in the UK life insurance market – term life and whole life. But to really get a feel for which is right for you, we need to go beyond simple definitions.

Here’s an analogy I find helpful: term insurance is a bit like renting a house. It’s affordable, it serves a specific purpose for a fixed amount of time (like when the kids are young or the mortgage is still looming), and once that time is up, you simply walk away. Whole life insurance, on the other hand, is like buying that house. It's a permanent asset that costs more upfront, but it's yours for good and it builds its own value over time.

Let's break down the key differences that really make a difference when it's time to decide.

Duration of Cover

The most straightforward distinction is simply how long the policy lasts.

- Term Life Insurance: This covers you for a specific, pre-agreed period, say 10, 20, or 25 years. If you pass away during that term, your family gets the payout. If you outlive it, the policy expires, and that’s that – no payout.

- Whole Life Insurance: This is permanent. As long as you keep up with your premiums, the policy stays active for your entire life, which means there’s a competitive payout when you die.

A new homeowner might grab a 25-year term policy to match their mortgage, making sure the debt is wiped clean if the worst should happen. Someone thinking about inheritance tax, however, needs a policy that is competitive to pay out eventually, which makes whole life the logical choice.

Premium Costs and Structure

This is often the deal-breaker for many families, and the two policy types are worlds apart on price.

- Term Life Insurance: The premiums are much, much lower. This is because the insurer is only on the hook for a limited time. Statistically, there’s a good chance you’ll outlive the policy, so their risk is lower, and the price reflects that.

- Whole Life Insurance: Brace yourself – premiums are significantly higher. We’re often talking five to ten times more than a term policy for the same amount of cover. That higher cost is funding both the competitive payout and the cash value growth.

It's worth noting that while term premiums can jump up if you renew at the end of a term, whole life premiums are usually fixed for life, giving you predictability for your long-term budget.

The "Buy Term and Invest the Difference" Strategy: A common financial argument is to buy affordable term insurance and invest the money saved on premiums elsewhere. When comparing whole life insurance with term life, a key consideration is often the alternative for the 'invest the difference' component, which leads many to explore various long-term investing strategies that could potentially yield higher returns, albeit with market risk.

Cash Value Component

This is a feature you’ll only find in permanent policies like whole life.

- Term Life Insurance: This is pure and simple protection. There’s no savings or investment element, and the policy has zero value once it expires.

- Whole Life Insurance: A portion of every premium you pay gets funnelled into a cash value pot. This pot grows at a competitive, tax-deferred rate, creating a financial asset you can actually borrow against or withdraw from while you're still alive.

This cash value gives you a flexibility that term insurance just can't match, but it comes at the price of those much higher premiums and pretty slow growth in the early years.

Primary Purpose

Ultimately, the best policy is the one that does the job you need it to do. For a detailed breakdown of these two options, our guide on whole life vs term insurance provides even more clarity.

- Term Life Insurance: Its main job is to act as a safety net for temporary, high-cost financial responsibilities. It’s perfect for covering a mortgage, seeing the kids through university, or just providing for your family until they're on their own two feet.

- Whole Life Insurance: This is a tool for long-term financial strategy. Its main uses are for estate planning (like covering a hefty inheritance tax bill), funding a business succession plan, or simply leaving a competitive legacy for your loved ones.

In short, one is a temporary shield for specific debts, while the other is a permanent financial asset built for legacy and estate goals.

Who Is a Whole Life Insurance Policy Really For?

A whole life insurance policy is a serious financial tool, but let's be clear: it's not the right fit for everyone. Because of its higher cost and long-term commitment, it really shines for people with very specific, long-range financial goals. Its core features—a competitive payout, fixed premiums, and a growing pot of cash value—offer unique answers to some of life's biggest financial questions.

The appetite for this kind of financial protection in the UK is significant. In fact, data from the Financial Conduct Authority (FCA) shows that in Q1 2025, a significant number of life insurance policies were sold, generating substantial premiums. This isn't just a niche product; it’s a cornerstone of long-term financial planning for many families across the country. You can dig into the numbers yourself in the FCA's life insurance sales data.

So, who are the people who genuinely get the most out of this type of permanent cover?

High-Net-Worth Individuals Planning Their Estate

If you have significant assets, inheritance tax (IHT) is likely a major headache. A whole life policy is a classic estate planning move for a simple reason: its payout is competitive, no matter when you pass away.

The real magic happens when you write the policy into a trust. By doing this, the payout usually falls outside your estate for IHT calculations. This means your beneficiaries get a tax-free lump sum precisely when they need it to pay the tax bill, ensuring your home and other assets can be passed on whole, just as you intended.

Parents of Children with Lifelong Dependencies

For parents or guardians of a child with special needs, the biggest worry is often how to provide for them long after you're gone. A whole life insurance policy offers a rock-solid solution.

It guarantees that a fund will be there to support your child's care, housing, and quality of life for the rest of their life. This level of certainty is something other financial products, which can be at the mercy of market swings, simply can't promise.

Business Owners Locking Down a Succession Plan

If you're a partner in a business, a whole life policy can be the linchpin for funding a buy-sell agreement. Think of this as a pre-nuptial agreement for your business, outlining what happens if a partner dies or wants out.

Here’s the breakdown:

- Each business partner takes out a whole life policy on the other partners.

- When one partner passes away, the payout from their policy gives the surviving partners the immediate cash to buy the deceased partner's share from their family.

- This makes for a smooth ownership transition without forcing the business to sell off assets or sink into debt at a difficult time.

A Note on Trusts: When using life insurance for estate planning, it's vital to consider all the tools in the toolbox. As you think about long-term financial planning and protecting your assets, it's worth understanding instruments like revocable living trusts. While they have their place, it's also important to be aware of the disadvantages of revocable living trusts, as they can sometimes complement or be an alternative to a life insurance strategy, depending on your personal situation.

Individuals Wanting to Leave a Legacy

At the end of the day, some people simply want to leave a competitive, tax-free gift to their children, grandchildren, or a charity close to their heart. A whole life policy is one of the most reliable ways to do just that.

Because the payout is fixed and certain, you know exactly what you’ll be leaving behind. It’s a straightforward way to create a lasting legacy, maybe fund a grandchild's education or make a significant charitable donation, all while skipping the usual complexities of probate.

Navigating the UK Market and Its Regulations

Choosing a whole life insurance policy is a major long-term commitment. It's completely natural to want some reassurance that your investment is safe for the long haul.

Fortunately, the UK has one of the world's most solid financial regulatory frameworks. It’s specifically designed to protect consumers like you and make sure insurance companies can keep their promises for decades to come. Understanding this layer of protection is key to feeling confident in your decision.

The Role of the FCA and PRA

Think of the UK's regulatory system as a dual-key lock, giving you multiple layers of security. Two main bodies work together, each with a distinct but complementary role.

- The Financial Conduct Authority (FCA) is all about how firms behave. Its job is to ensure you're treated fairly, products are explained clearly without misleading jargon, and you get the right information to make a solid choice.

- The Prudential Regulation Authority (PRA), which is part of the Bank of England, looks at the financial health of the insurers themselves. It makes certain these companies are financially sound and have enough capital tucked away to pay out all future claims, even if the economy hits a rough patch.

Together, these two create a secure environment where you can trust your policy is being managed responsibly, both in terms of conduct and financial stability.

The Financial Services Compensation Scheme (FSCS)

But what happens if, despite all these checks, an insurance company were to fail? This is where the Financial Services Compensation Scheme (FSCS) comes in. It’s the ultimate safety net for customers of authorised financial services firms.

For long-term insurance products like a whole life policy, the FSCS provides an incredibly high level of protection. If your insurer goes out of business, the scheme protects 100% of your claim with no upper limit. This guarantee provides complete peace of mind, knowing your family’s financial future is secure no matter what.

The UK's regulatory environment is meticulously monitored. The Bank of England reports that rules like Solvency II are critical, compelling insurers to manage substantial assets to guarantee policyholder security. These measures ensure the whole life sector remains resilient against economic shifts, safeguarding product guarantees for the long term. Learn more about insurance aggregate data reports.

These strict capital requirements and constant oversight are precisely why the UK insurance market is considered so stable. It's also useful to know the distinction between different types of lifetime cover; our guide explains the difference between life insurance and life assurance in more detail.

Ultimately, this entire framework is built to ensure the promise made to you today can be kept many, many years from now.

Frequently Asked Questions

When you’re digging into the details of a whole life insurance policy, a few common questions always seem to pop up. Let's get them answered in a clear, straightforward way so you know exactly what to expect from your cover down the line.

Can I Change My Policy After It Starts?

One of the main selling points of a whole life policy is its predictability. Once it's up and running, the core elements—like your premium and the competitive payout for your family—are set in stone.

That said, some modern policies from UK insurers like Aviva or Legal & General have built-in flexibility. You might find you can increase your cover when you hit major life milestones (like getting married or having a baby) without needing another medical check, although your premiums would go up to match. It’s sometimes possible to reduce your cover too, but you’ll want to have a chat with your insurer or an adviser first to see how that would affect your cash value.

What Happens If I Can No Longer Afford the Premiums?

Life throws curveballs, and what feels affordable today might not tomorrow. If you hit a point where paying the premiums is a struggle, you’re not out of options, and you won't automatically lose all the value you've built up.

Typically, here's what you can do:

- Use the Cash Value: You can often dip into the cash value you've accumulated to cover your premiums for a while.

- Take a Premium Holiday: Some policies let you press pause on payments for a bit, though this can have an impact on your cover.

- Convert to a Paid-Up Policy: You can stop paying premiums entirely. In return, you'll get a smaller, but fully paid-up, payout based on the money you've already put in.

- Surrender the Policy: This is usually the last resort. You can cancel the policy and walk away with the cash surrender value, but it does mean your life cover ends.

Is the Payout from a Whole Life Policy Taxable?

In the UK, the lump sum paid out from a life insurance policy is almost always free of income tax and capital gains tax. The one thing to watch out for is Inheritance Tax (IHT).

If the policy payout pushes the total value of your estate over the IHT threshold (currently £325,000 per person), anything above that limit could be taxed at 40%.

This is where a simple bit of planning makes a huge difference. By placing your whole life insurance policy into a trust, the payout usually sits outside of your estate for IHT calculations. It's a powerful and straightforward way to make sure your beneficiaries get the full amount you intended, without the taxman taking a slice.

Ready to explore your options and find a policy that provides lasting security for your family? The team at Discount Life Cover can help. Get a personalised, no-obligation quote today and take the first step towards peace of mind.

Get Your Free Whole Life Insurance Quote Now

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply