Figuring out what you'll pay for term life insurance isn't a simple case of picking a number off a shelf. It’s entirely personal, with your final monthly premium being shaped by your own circumstances and exactly how much cover you need.

It’s a bit like getting a suit tailored – the final price depends on the fabric, the cut, and your measurements. There's no single price tag, but to give you a rough idea, a healthy, non-smoking 30-year-old could be looking at a premium of just £8-£12 per month for a decent amount of protection.

How Your Premium Gets Personalised

The price you're quoted isn't just plucked out of thin air. It's the result of a careful calculation based on risk, a process known in the industry as underwriting. UK insurers like Aviva, Legal & General, and LV= look at a whole range of factors to work out the likelihood of a claim being made during the policy's term.

The logic is simple: the lower they see the risk, the lower your monthly payments will be. We'll get into the nitty-gritty later, but the main things they'll look at are:

- Your age and health: It's no surprise that younger, healthier people nearly always get the best rates.

- Your lifestyle: Things like smoking or heavy drinking can push your premiums up significantly.

- The policy itself: How much cover you want and for how long are two of the biggest factors in the final price.

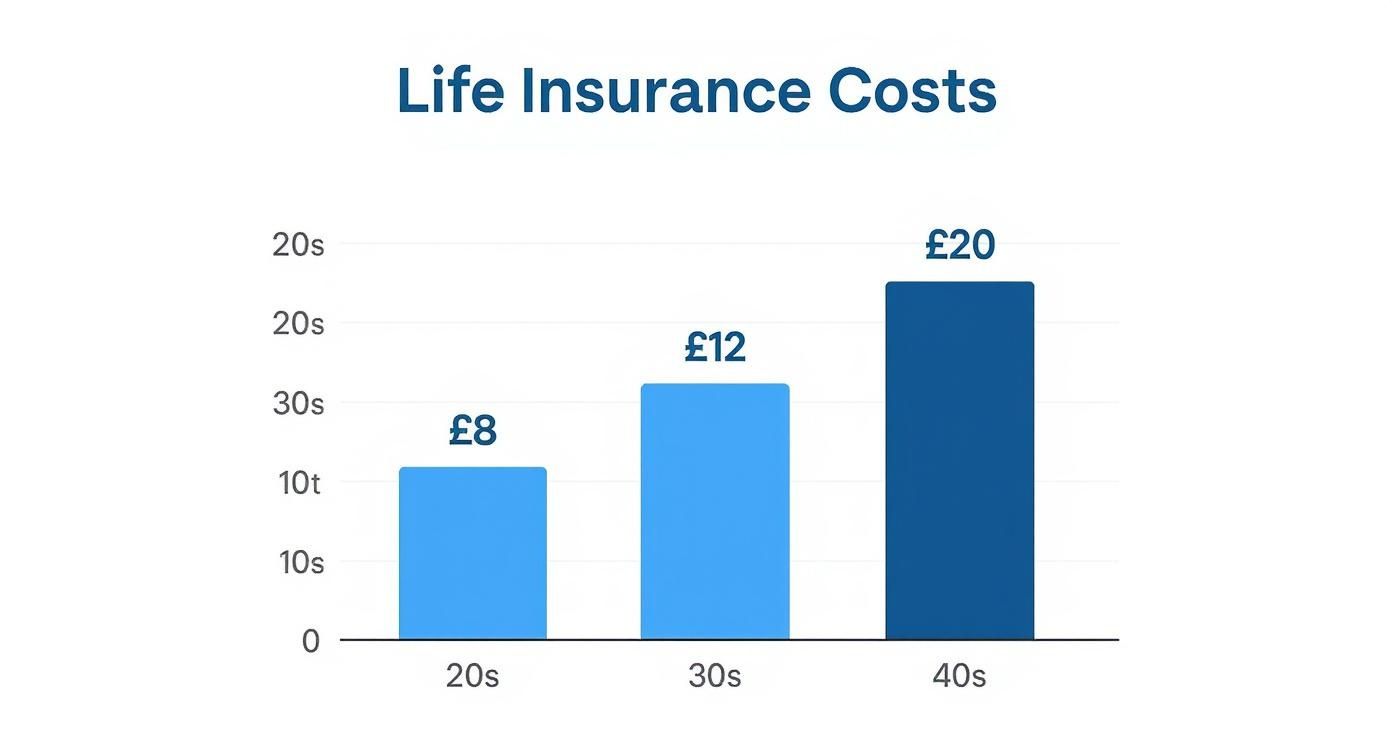

This chart really brings home how age plays a part, showing how monthly premiums for a non-smoker tend to climb over the years.

It’s clear to see that getting cover sorted in your 20s or 30s can mean locking in a much more affordable rate for the entire life of the policy.

Average Term Life Insurance Costs by Age

To give you a clearer picture, here’s a table showing some sample monthly premiums. These are just illustrations for a non-smoker looking for £150,000 of level term cover over 25 years, but they show the general trend.

| Age Range | Average Monthly Premium |

|---|---|

| 20-29 | £8 – £12 |

| 30-39 | £12 – £20 |

| 40-49 | £25 – £45 |

| 50-59 | £60 – £100+ |

Remember, these are just ballpark figures. Your actual quote will depend on your specific health and lifestyle details, but it's a useful starting point.

What’s the UK Average?

Looking at the bigger picture, recent industry-wide data gives us a handy benchmark. In 2024, research covering over 120,000 policies found that the average cost of life insurance in the UK was £32.64 per month. This was for an average payout (or 'sum assured') of £160,871.36.

That average figure is useful for context, but it’s crucial to remember your individual premium could be much lower or higher. It all comes down to your personal profile.

For a more detailed look at what you might expect to pay, our guide on how much life insurance costs breaks it down even further. By getting to grips with what influences your quote, you can start taking steps to find the right protection for your family at the best possible price.

The Personal Factors That Shape Your Premiums

When you for term life insurance, insurers don't just pluck a number out of thin air. They carry out a detailed assessment called underwriting. Think of it as a financial MOT for your life and circumstances; they're simply trying to understand the level of risk they're taking on.

Several key personal factors come under the microscope, and each one plays a role in what you’ll end up paying. Getting to grips with what insurers are looking for gives you a much clearer picture of your potential term life insurance costs. It helps you see what you can influence and what’s set in stone, putting you in the driver's seat when it comes to finding affordable cover.

The whole process really boils down to four main areas.

Age and Overall Health

This one’s a biggie. Your age is one of the most significant factors because, statistically speaking, younger people are less likely to fall ill. Nailing down a policy when you're young and in good nick often means locking in a much lower premium for the entire term.

Beyond just the number of candles on your cake, your current health is critical. Insurers will want to know your height and weight (to calculate your BMI) and ask about any pre-existing medical conditions. They need the full story to accurately price your policy.

Lifestyle Choices

What you do day-to-day has a direct impact on your premiums. It’s no surprise that insurers view certain habits as a red flag, which unfortunately leads to higher costs.

The main lifestyle factors they look at include:

- Smoking or Vaping: This is the single biggest lifestyle factor, hands down. Smokers can expect to pay significantly more—often double—than non-smokers. Most insurers will want you to be totally nicotine-free for at least 12 months before they'll class you as a non-smoker.

- Alcohol Consumption: They'll ask about your weekly alcohol intake. A glass of wine here and there usually has little impact, but consistently high consumption can definitely push up your premiums.

- Hobbies and Activities: If you’re a bit of a thrill-seeker, this could affect your price. Hobbies considered high-risk, like motorsports, mountaineering, or scuba diving, might mean your insurer will add a bit extra to your premium to reflect the added danger.

Making positive changes, especially quitting smoking, can have a massive effect on what you pay. It’s one of the most powerful ways to slash your costs.

Your Occupation

What you do for a living matters, too. An office-based job is seen as pretty low-risk, but if your profession involves manual labour, working at heights, or handling hazardous materials, insurers will naturally see it as a higher risk.

It's common sense, really. A construction worker or a deep-sea fisherman will likely face higher premiums than a graphic designer or an accountant because of the dangers that are part and parcel of their work.

Family Medical History

Finally, insurers will have a look at the medical history of your immediate family (your parents and siblings). They’re particularly interested in any hereditary conditions that showed up at an early age, such as certain cancers, heart disease, or genetic disorders like Huntington's disease.

A significant family history of a serious condition might suggest a higher statistical risk for you, even if you are currently in perfect health. It’s absolutely crucial to be honest here; withholding information could give the insurer grounds to invalidate your policy down the line, a requirement under Financial Conduct Authority (FCA) rules.

By understanding these personal factors, you can see exactly how term life insurance costs are put together. This knowledge empowers you to take control where you can and tackle your application with confidence.

How Your Policy Choices Impact the Final Price

So far, we’ve looked at how your personal circumstances – your age, health, and lifestyle – affect your premium. But that’s only half the story. The other crucial part is the policy itself. The decisions you make about the structure of your insurance, like how much it pays out and for how long, are massive drivers of your final term life insurance costs.

Getting these choices right is the key to finding cover that not only protects your family but also fits comfortably within your budget. Two of the biggest decisions you’ll face are the type of policy and the length of the term. Let's dig into what they mean for your wallet.

Level Term vs Decreasing Term Cover

Here in the UK, term life insurance generally comes in two main flavours. They both pay out if you pass away during the policy term, but the way that payout is structured is completely different.

Level Term Insurance: With this type of policy, the payout amount (often called the 'sum assured') stays fixed for the whole term. If you get a £200,000 policy for 25 years, your family would receive that full £200,000 whether a claim is made in the first year or the 24th. This makes it a really popular choice for covering an interest-only mortgage or, more commonly, leaving a lump sum to handle day-to-day living costs, school fees, and other ongoing expenses. A new parent wanting to make sure their children are provided for is a typical example.

Decreasing Term Insurance: As the name suggests, the potential payout on this policy reduces over time. It’s designed to run alongside a large debt that’s also shrinking, like a repayment mortgage. The logic is simple: as you pay off more of your mortgage, the amount of cover needed to clear it also falls. Because the insurer's potential liability drops each year, these policies are almost always than level term cover. A homeowner who just wants peace of mind that their mortgage will be paid off would likely opt for this more affordable option.

Choosing between them really comes down to what you’re trying to protect.

The policy type you select is one of the most significant factors in determining your premium. Decreasing term is almost always the more budget-friendly option, but level term provides a consistent safety net for your loved ones.

The Amount of Cover and Term Length

This is where the rubber really hits the road. How much cover do you need, and for how long? Your answers to these two questions will have a direct and very significant impact on your monthly premium.

The sum assured is the total amount your policy will pay out. It’s pretty straightforward – a policy for £500,000 will naturally cost more than one for £150,000, assuming all other factors are the same. For the insurer, it's a simple calculation of risk.

Likewise, the term length—the number of years the policy is active—is a major cost driver. A 35-year term for a new parent will be quite a bit more expensive than a 10-year term for someone protecting the final years of their mortgage. The longer the term, the higher the statistical chance of a claim being made. The difference can be stark; recent UK data shows monthly premiums can be as low as £3.53 for a 20-year-old but can jump to around £23.73 for a 50-year-old, showing just how much age and policy length interact. You can learn more about the average cost of life insurance at Insurance Hero.

Adding Optional Extras

Many insurers, including big names like Aviva and Legal & General, let you bolt on optional extras to your term life policy for more comprehensive protection. One of the most common additions is Critical Illness Cover.

This is a really valuable add-on that provides a tax-free lump sum if you're diagnosed with a specific, serious illness like cancer, a heart attack, or a stroke. It’s designed to help you financially while you recover.

Of course, adding Critical Illness Cover provides another layer of security, but it will also increase your monthly premium. You're essentially covering yourself against two different risks—death and serious illness—so the cost naturally reflects that enhanced protection.

Practical Ways to Lower Your Insurance Costs

Knowing what pushes your premium up is one thing, but taking control is what really matters. While you can't turn back the clock on your age, there are plenty of practical steps you can take to bring down your term life insurance costs.

Think of it like getting your car ready for its MOT; a few smart adjustments can make a huge difference to the final bill. These are the things you can do to get the cover you need without breaking the bank.

Act Sooner Rather Than Later

This is probably the simplest, most powerful trick in the book: buy life insurance when you’re young and healthy. As we’ve seen, age is a massive factor for insurers. By getting a policy sorted in your 20s or 30s, you can lock in a much lower rate for the entire term, potentially saving thousands over the years.

Improve Your Lifestyle Habits

Insurers love to see healthy habits, and they reward them with lower premiums. Making a few positive changes to your lifestyle can have a direct, and often significant, impact on the quotes you get.

Here are the big ones:

- Quitting Smoking and Vaping: This is the single biggest money-saver. Insurers typically need you to be completely nicotine-free for at least 12 months before they'll class you as a non-smoker, a move that could easily slash your premiums in half.

- Reducing Alcohol Intake: Keeping your weekly alcohol consumption within the recommended guidelines signals a lower-risk lifestyle to insurers, which they'll reflect in your price.

- Maintaining a Healthy Weight: A healthy Body Mass Index (BMI) often leads to better rates. It reduces the statistical risk of developing various health problems down the line, making you a more attractive applicant.

Choose the Right Policy and Consider a Joint Policy

It's crucial to pick the right tool for the job. If your main reason for getting cover is to protect a repayment mortgage, a decreasing term policy will almost always be than a level term one. There's no point paying for more cover than you actually need.

For couples, a joint life, first death policy can be a good way to save money. It’s a single policy covering two people that pays out when the first person passes away, at which point the cover stops. They're often than two separate policies, but it's important to remember that the surviving partner would then be left without any cover.

The UK term life insurance market is incredibly competitive, with insurers always tweaking their products. In fact, the wider life insurance sector is expected to grow by 2.4% each year until 2027, largely thanks to simpler, more direct policies becoming available. You can read more about UK insurance market trends at the Bank of England.

Shop Around and Compare Quotes

Finally, the most powerful strategy of all is simply to compare the market. You should never, ever accept the first quote you're given.

Every insurer calculates risk differently, and prices can vary wildly between them for the exact same amount of cover. Using an independent broker like Discount Life Cover is the easiest way to see quotes from a huge range of UK insurers all in one go. Our guide on finding the cheapest term life insurance has more on this. It's the only way to be sure you're getting the best possible price for your circumstances.

Navigating Life Insurance with Health Conditions

For a lot of us, the biggest question mark when looking into life insurance is a pre-existing health condition. How will it affect the application? And, more importantly, what will it do to the term life insurance costs? It's a completely valid concern, but the good news is that having a health condition doesn't automatically shut the door on getting cover.

Whether it’s diabetes, high blood pressure, or a history of mental health challenges, UK insurers tend to look at your individual situation rather than just issuing a blanket 'no'. Their main goal is to understand how well you're managing the condition and what its potential impact is on your long-term health. For example, people over 50 with medical conditions might find that a specialist over-50s policy is a suitable option, as these often guarantee acceptance without a medical exam, although the cover amount is typically lower.

The Importance of Full Disclosure

When you , you’ll face a detailed set of questions about your health, both past and present. It is absolutely crucial that you answer every single one openly and honestly. This isn't just about being a good sport; it's a firm requirement under the rules set out by the Financial Conduct Authority (FCA).

Tempting as it might be to leave something out to get a premium, it can backfire badly. If an insurer later finds out you weren't truthful, they could refuse to pay out a claim. That would leave your family without the very protection you were trying to put in place for them.

An insurer's decision is based on a principle called 'utmost good faith'. In simple terms, they trust you to give them all the relevant facts so they can fairly assess the risk. If that trust is broken, it can invalidate your entire policy.

How Different Health Conditions Are Viewed

Insurers don't have a one-size-fits-all approach. They assess each condition on a case-by-case basis, wanting to know when you were diagnosed, what treatment you're on, and how stable things are.

Here’s a rough idea of what they look for with some common conditions:

- High Blood Pressure: They'll be keen to see your recent readings and find out if your condition is well-managed with medication. Keeping on top of things is key, as this directly influences your eligibility and costs. You can find a helpful guide to managing blood pressure that offers some great information.

- Diabetes: Insurers will distinguish between Type 1 and Type 2. They will almost certainly ask for your latest HbA1c reading to get a clear picture of how well your blood sugar is controlled.

- Mental Health: For conditions like anxiety or depression, they’ll consider the severity, how often symptoms occur, and any treatment you've had. A condition that's clearly being managed well is always viewed more positively.

For a deeper dive into how a whole range of different conditions are assessed, you can explore our guide on securing life insurance with medical conditions.

The Role of a Specialist Broker

If you have a pre-existing medical condition, trying to find the right policy on your own can feel like navigating a maze. This is exactly where a specialist broker proves their worth.

A good broker has inside knowledge of the market. They know which insurers are more understanding about certain conditions. For instance, one provider might offer great terms for well-managed diabetes, while another might be the go-to for someone with a past mental health issue. A broker can point you to the right insurer, help you fill out the application accurately, and massively boost your chances of getting affordable cover. They do the legwork for you, making sure you find the best policy for your specific circumstances.

Finding the Right Cover for Your Budget

So, let's pull all of this together. You've now got a solid grasp of what really drives term life insurance costs and, more importantly, what you can do about it to find a policy that fits your life and your wallet.

The next step is simple: see what's actually out there for you. Getting a real look at your options is the single best way to make sure you're getting the right protection at a fair price.

It’s amazing how much premiums can vary for the exact same level of cover. Every insurer has its own way of calculating risk, and by comparing quotes, you can be certain you aren't paying more than you need to for that essential protection.

We set up DiscountLifeCover for this very reason – to give you a clear, no-nonsense comparison of quotes from the UK's leading insurers, saving you time and hassle.

Ultimately, this is about finding a policy that gives you genuine peace of mind without putting a strain on your budget. Take the first step today to protect your family's future and see what's possible. The right cover for the people who matter most could be just a few clicks away.

Frequently Asked Questions

Got a few lingering questions? It's completely normal. Let's tackle some of the most common queries we hear about term life insurance in the UK.

Is Joint Life Insurance Cheaper for Couples?

On the face of it, yes. A joint life policy is almost always than buying two separate, single policies for a couple. It’s designed to cover both of you but only pays out once – usually when the first person passes away.

But here's the crucial thing to think about: once it pays out, the cover is gone. This leaves the surviving partner without any life insurance. For total peace of mind and long-term protection for both of you, two single policies are often the smarter choice, even if they cost a bit more upfront.

Can I Change My Cover Later On?

Generally speaking, once your policy is up and running, you can't just ring up and ask to increase the cover amount or make the term longer. The price was calculated based on your health and age at that specific moment.

However, most UK insurers build in something called a ‘Insurability Option’ (or GIO). This is a really valuable feature that gives you some flexibility. It lets you increase your cover, without needing a new medical assessment, after major life events like:

- Getting married or entering a civil partnership

- Having a baby or adopting a child

- Taking on a much bigger mortgage for a new home

It’s a great little safety net that allows your policy to adapt as your life evolves.

What Happens if I’m Not Honest on My Application?

Being anything less than 100% truthful on your application is a massive risk, and one that can have heartbreaking consequences for your family. The Financial Conduct Authority (FCA) has strict rules, and insurers calculate your premium based entirely on the information you provide.

If you don't disclose a medical condition or a lifestyle choice (like smoking), and the insurer finds out later, they have the right to void your policy. That means they can cancel it completely. The worst part? Any claim would be rejected, leaving your loved ones with absolutely nothing when they need it most. Honesty is non-negotiable here.

Does Life Insurance Pay Out for Suicide?

Yes, most life insurance policies in the UK do cover death by suicide. However, there's nearly always an exclusion clause for the first 12 to 24 months of the policy.

This means if the policyholder were to take their own life within that initial period, the insurer typically wouldn't pay the full claim. They might refund the premiums that have been paid, but the main payout would be denied. This clause is a standard industry practice to prevent the awful situation where someone might take out a policy with suicide in mind.

Ready to see just how affordable protecting your family could be? Discount Life Cover simplifies the whole process. You can compare quotes from the UK's top insurers in just a few minutes.

Get your free, no-obligation quote today and take that first, vital step.

Get Your Free Life Insurance Quote Now

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply