"So, how much is life insurance UK?" It's a question many of us ask when thinking about protecting our families. The simple answer is that costs vary, but you might be surprised at how affordable cover can be.

For a healthy 30-year-old, a policy can often be secured for less than the price of a couple of takeaway coffees a month. In fact, for many people in the UK, premiums can start from as little as £5 to £8 a month.

This guide explains what determines the cost of life insurance in the UK, how different policies compare, and how you can find the right cover for your budget.

What Is the Average Cost of Life Insurance in the UK?

Understanding the average cost of life insurance gives you a helpful benchmark. While the final price tag will always depend on your personal circumstances, looking at typical premiums helps demystify the process and shows how accessible financial protection can be.

At its core, the price you pay is based on how an insurer assesses risk. A younger, healthier person is statistically less likely to pass away during the policy term, which means a lower premium. Conversely, factors that increase risk—like being older, smoking, or having certain health conditions—will push the cost up.

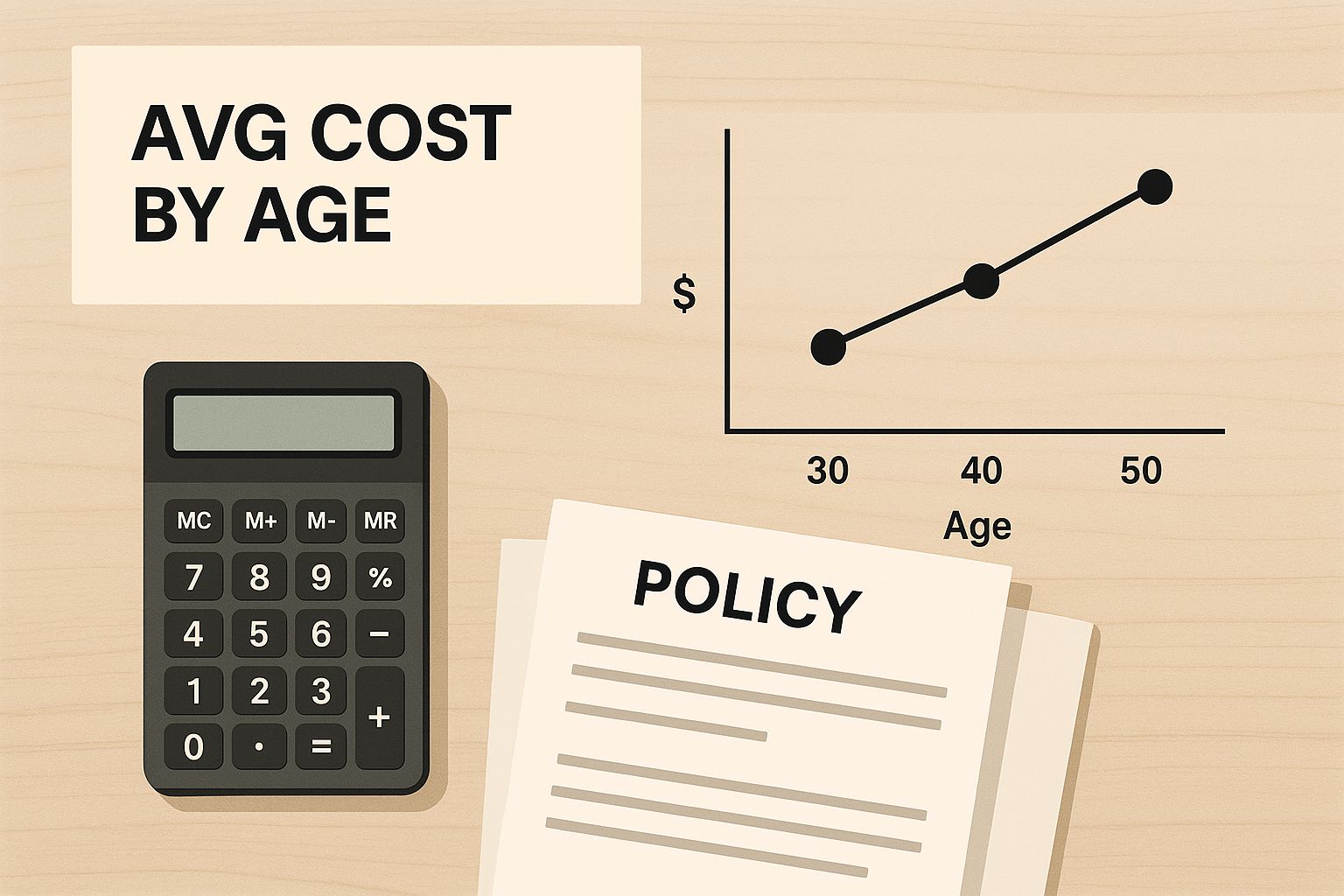

A Quick Look at Average Premiums

To give you a clearer idea of what to expect, let's look at some real-world numbers.

Example Monthly Life Insurance Premiums for Non-Smokers

This table shows estimated monthly costs for a non-smoker in good health. These examples are for a level term life insurance policy with £150,000 of cover over a 25-year term.

| Age | Average Monthly Premium |

|---|---|

| 30 | £8 – £12 |

| 40 | £14 – £20 |

| 50 | £35 – £50 |

Premiums are indicative and will vary based on individual circumstances and the insurer.

These figures drive home a crucial point: the earlier you get cover, the it is. You can lock in a lower rate for the entire term of the policy. If you want to dig deeper, you can explore more detailed breakdowns of term life insurance rates to see how different factors come into play.

The demand for this kind of financial security is growing. In 2023, the UK life insurance market saw a notable growth of 7.1%, as more households recognised the importance of having a safety net. This reflects a wider trend towards securing financial stability for the future.

In the next sections, we'll break down exactly what influences these prices and explain how different types of policies are priced.

The Key Factors That Shape Your Premium

Think of your life insurance premium like a bespoke suit – the final price depends entirely on the measurements. Insurers in the UK use a process called underwriting to assess the level of risk they are taking on by covering you. This involves looking at a range of personal factors to build a picture of your health and life expectancy.

The lower the insurer perceives the risk, the lower your monthly premium will be. Understanding these key factors gives you the power to see exactly what’s driving the cost.

Your Age and Health

Age is the biggest piece of the puzzle. As shown above, a 30-year-old will pay significantly less than a 50-year-old for the same amount of cover. Statistically, younger people are less likely to pass away during the policy's term, making them a lower risk for the insurer.

Your current health and medical history are also critical. Insurers will need to know about:

- Your height and weight: This is used to calculate your Body Mass Index (BMI).

- Pre-existing medical conditions: Such as diabetes, heart conditions, or a history of cancer.

- Your family's medical history: This helps identify potential hereditary conditions.

- Recent medical tests or treatments: Providing an up-to-date snapshot of your health.

Key health indicators, such as those from liver function tests, can influence your premium. Getting a handle on these markers by understanding liver function test results can help you stay on top of your health.

Lifestyle Choices Matter

Your day-to-day habits provide insurers with clues about your long-term health. It’s crucial to be honest when answering these questions, as providing false information could invalidate your policy.

Important Note: Hiding or failing to mention a key health or lifestyle factor is known as 'non-disclosure'. Under the Consumer Insurance (Disclosure and Representations) Act 2012, you are legally required to take reasonable care to answer an insurer's questions fully and accurately.

Key lifestyle factors include:

- Smoking or Vaping: This is the single biggest lifestyle factor. Smokers can expect to pay at least double what a non-smoker pays for the same cover.

- Alcohol Consumption: Insurers will ask about your weekly unit intake to assess potential health risks.

- Occupation and Hobbies: A desk job is seen as less risky than working on an oil rig. Similarly, high-risk hobbies like rock climbing or skydiving might also increase your premium.

Your Policy Details

Finally, the specifics of the policy you choose will have a direct impact on the price. These are the main elements you can adjust:

- The Cover Amount: This is the total payout your policy provides, also known as the sum assured. A £500,000 policy will cost more than one for £150,000.

- The Policy Length: This is the term of the policy. A 30-year term covers you for a longer period of risk than a 15-year term, and the price will reflect that.

- The Policy Type: Different kinds of cover, such as level term versus decreasing term, have different price points. We'll explore this next.

How Your Choice of Policy Impacts the Price

Not all life insurance is the same, and the type of cover you pick plays a huge role in your monthly premium. The first and biggest decision for most people is choosing between term life insurance and a whole of life policy.

For the vast majority of people in the UK, term insurance is the most common choice. It’s affordable, straightforward, and covers you for a set period (the 'term'), such as 25 years. If you pass away during that time, your family gets the payout.

The infographic below gives you a quick visual guide on how different factors like your age can push costs up or down.

As you can see, age is a huge driver of premiums. This is why it pays to arrange cover sooner rather than later – it can genuinely save you a small fortune over the life of the policy.

Level Term vs Decreasing Term Insurance

Within term insurance, there are two main types, each designed for a specific purpose.

- Level Term Insurance: With this policy, the payout amount (the sum assured) and your monthly premium stay the same throughout the term. It's a popular choice for leaving a fixed lump sum for your family or covering an interest-only mortgage.

- Decreasing Term Insurance: With this policy, the amount of cover reduces over time, usually designed to mirror the outstanding balance on a repayment mortgage. Because the insurer's potential payout gets smaller each year, the premiums are almost always than level term cover. Its main purpose is to ensure a mortgage is paid off.

Deciding which is right for you is a crucial step. You can explore the pros and cons in our guide on whether you should choose level term or decreasing term life insurance.

Whole of Life and Other Policy Types

For those seeking lifelong protection, other policies are available, but they come with a higher price tag.

- Whole of Life Insurance: This policy covers you for your entire life and guarantees a payout whenever you pass away, provided you’ve kept up with the premiums. Because of this guarantee, it’s significantly more expensive than term insurance.

- Over 50s Plans: These are a specific type of whole of life policy with competitive acceptance for UK residents aged 50-85. There are no medical questions, which makes them easy to arrange. The trade-off is that the cover amounts are smaller, typically intended to help with funeral costs.

The Impact of Add-Ons

You can also add extra benefits to your policy, but each one will increase your premium. The most common is Critical Illness Cover, which pays a lump sum if you're diagnosed with a serious illness specified in the policy. It provides an excellent extra layer of financial security but can increase your premium substantially.

Putting It All Together with Real-World Examples

Theory is a great start, but nothing brings life insurance to life like seeing how it works for real people. Let's walk through a few common scenarios in the UK.

Example 1: The Young Family with a Mortgage

Meet Sarah and Tom, both 32-year-old non-smokers in good health. They have just bought their first home with a £250,000 repayment mortgage over 30 years and have a young child.

Their main concern is ensuring the mortgage is paid off if one of them were to pass away, so the surviving partner and child wouldn't lose their home.

- Policy Choice: They opt for a joint decreasing term policy for £250,000 over 30 years. The cover amount drops over time, roughly in line with their shrinking mortgage balance.

- Estimated Premium: They are likely to be quoted around £12-£18 per month.

This is an affordable way to cover their single biggest debt, providing invaluable peace of mind.

Example 2: The Over 50s Planner

Now meet David, who is 58 and divorced. His mortgage is paid off and his children are financially independent. His main goal is to leave enough money to cover his funeral costs and a small gift for his grandchildren, without needing a medical examination.

- Policy Choice: An Over 50s Life Insurance plan is a perfect fit. He chooses a policy that guarantees a fixed payout of £7,000.

- Estimated Premium: For this competitive acceptance cover, David can expect to pay around £25-£35 per month.

This is a straightforward, no-fuss solution designed for final expenses planning.

Example 3: Cover with a Health Condition

Finally, let's look at Maria, a 45-year-old office manager. She was diagnosed with Type 2 diabetes five years ago, which she manages well with diet and medication. She wants a policy to leave her partner a financial cushion, separate from their mortgage.

- Policy Choice: Maria applies for a level term policy with £150,000 of cover over a 20-year term. She is upfront about her diabetes and provides details from her GP.

- Estimated Premium: Because her condition is well-managed, the insurer offers her a policy for around £40-£55 per month.

Maria's story shows that having a pre-existing medical condition doesn't automatically prevent you from getting affordable cover. Insurers are more interested in how well a condition is managed.

These examples show that the answer to "how much is life insurance UK?" depends on shaping a policy to fit different budgets, life stages, and personal needs.

Practical Steps to Find Cheaper Life Insurance

Knowing what affects your premiums is one thing; using that knowledge to reduce the cost is another. The good news is there are several effective ways to get the cover you need without breaking your budget.

Act Sooner Rather Than Later

The golden rule of life insurance is simple: the younger you are, the it is. With every birthday, insurers see a slight increase in risk, which translates into higher premiums.

By getting a policy when you're young and in good health, you lock in that lower rate for the entire term. Over the decades, this simple timing could save you thousands of pounds.

Improve Your Health and Lifestyle

Your lifestyle choices have a significant impact on your premiums. The single biggest financial win you can score is quitting smoking.

Insurers typically classify you as a non-smoker once you have been completely nicotine-free (including vaping and patches) for at least 12 months. Reaching this milestone can reduce your premiums by 50% or even more.

Other positive steps that can make a difference include:

- Maintaining a healthy weight: Insurers use your BMI as a key health indicator.

- Reducing alcohol intake: Sticking within recommended weekly alcohol limits signals a lower health risk.

Consider a Joint Policy

For couples, a joint life insurance policy is often than two separate single policies. It covers both individuals but usually pays out only once—on the first death—at which point the policy ends.

While it saves money upfront, it's vital to consider the downside. If the surviving partner still needs cover after a claim, they would have to for a new policy at an older age, which would be more expensive.

Always Compare the Market

This is the most important step. Never accept the first quote you receive. Different insurers have different underwriting criteria, meaning prices can vary significantly between providers for the exact same cover.

Taking a moment to explore options for budget life insurance through a comparison service is crucial. It’s the only way to see what a wide range of UK insurers are offering, giving you the best chance of finding a competitive deal.

A Quick Look at the UK Life Insurance Market

When you start looking for life insurance, it helps to understand the landscape. You are entering a large, competitive, and well-regulated industry designed to provide protection.

Big UK insurers like Aviva, Legal & General, and Royal London are all competing for your business. This competition benefits consumers by keeping prices competitive and encouraging product innovation.

Overseeing this market is the Financial Conduct Authority (FCA). The FCA sets the rules for UK financial services, ensuring that insurance is sold fairly, products are transparent, and insurers are financially robust enough to pay claims. This regulation provides an essential layer of consumer protection.

How Technology and Rules Shape Your Policy

The industry is constantly evolving, driven by technology and regulation. Insurers are using data and analytics to make the application process quicker and more accurate, leading to more personalised pricing.

At the same time, regulators continually push insurers to be more financially resilient, ensuring they can meet their long-term promises to policyholders. If you're interested in the details of how the market is evolving, XPS Group has a great breakdown.

Knowing this helps you understand that when you ask how much is life insurance UK, the final price is the product of this dynamic and highly regulated market.

Frequently Asked Questions (FAQ)

Life insurance can seem complex. To help, here are clear answers to some of the most common questions.

How much life insurance cover do I actually need?

A common rule of thumb is to aim for cover worth around 10 times your annual salary. While this is a good starting point, a more accurate figure comes from calculating your specific needs. Add up your mortgage, any other debts, and the future living costs for your family. Then, subtract any existing savings or investments. The remaining figure is the financial gap your life insurance should fill.

Will I have to do a medical exam?

Not always. Many UK life insurance policies are approved without one, especially if you're younger and ing for a standard amount of cover. A detailed health and lifestyle questionnaire is often sufficient. However, an insurer may request a medical exam or a report from your GP if you are older, ing for a large sum assured, or have declared a significant pre-existing health condition.

Can I get insured if I have a medical condition?

Yes, in most cases. It's a common misconception that having a health issue automatically disqualifies you from getting life insurance. While some high-street insurers might increase your premiums or decline cover, many specialist insurers and brokers have experience finding appropriate policies. The key is to be completely honest about your condition and how it is managed.

Is life insurance worth the money?

Ultimately, life insurance is about buying peace of mind. For a relatively modest monthly payment, you secure a substantial, tax-free payout for your loved ones. This financial safety net can prevent them from having to sell the family home, struggle with bills, or abandon their future plans during an incredibly difficult time. For most people, that protection is priceless.

Ready to see just how affordable your cover could be? Here at Discount Life Cover, we make it simple to compare quotes from the UK’s top insurers in minutes.

Get Your Free, No-Obligation Quote Today

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply