It’s a difficult subject, but one of the most common questions people ask is: does life insurance pay for suicide?

The short answer is yes, it usually does. However, there is a crucial condition you must be aware of. Almost every policy in the UK includes a 'suicide clause', which sets a waiting period – typically the first 12 months – during which a claim for suicide would be declined.

This guide explains in plain English how this works for UK policyholders, why the clause exists, and what it means for your family's financial security.

How UK Life Insurance Handles Suicide Claims

It's a sensitive question, but getting a clear, factual answer is essential when planning for your family's future. The main reason for this waiting period, sometimes called an exclusion period, is to protect the insurer from fraud. It helps ensure policies are taken out in good faith for the long-term security of loved ones, not with the immediate intention of making a claim.

Think of this initial period as a safeguard. If a death by suicide occurs within this window, the insurer won't pay the full claim amount. However, they will almost always refund all the premiums paid up to that point, so the money isn't lost.

Once that initial period is over, a claim for suicide is generally treated just like any other claim, provided all other policy conditions have been met.

The Suicide Clause Explained

The suicide clause is a standard feature you'll find in the vast majority of UK life insurance policies. Its purpose is straightforward: to manage risk for the insurance company.

Here’s a simple breakdown of what it means for you:

- The Waiting Period: Almost every standard life insurance policy has a 'suicide clause'. This means if the policyholder dies by suicide within the first 12 months of the policy starting, the claim will be rejected. You can find more details on how these clauses work at iaminsured.co.uk.

- After the Period Ends: Once you're past that initial 12-month mark, the clause effectively expires. A claim for suicide would then be valid and payable to your beneficiaries.

- Premium Refunds: If a claim is denied because it falls within this 12-month window, the insurer will return all the premiums that were paid into the policy.

For a quick overview, this table breaks down how it all works in practice.

How the UK Suicide Clause Works at a Glance

| Time Since Policy Start | Typical Payout Status for Suicide | What This Means for You |

|---|---|---|

| Within 12 months | Claim Denied | The full cover amount will not be paid out, but all premiums you've paid will be refunded. |

| After 12 months | Claim Approved | The full cover amount is paid to your beneficiaries, just like any other valid claim. |

This setup is designed to be a fair balance. It protects insurers from misuse while still allowing you to secure your family’s financial future. Understanding this simple rule provides a clear foundation as we explore how this can vary with different policies and personal circumstances.

Navigating the Suicide Clause in UK Life Insurance

It’s a difficult topic, but one we must be clear about. When people look into life insurance, they often wonder how it handles claims related to suicide. The key is to think of the ‘suicide clause’ not as a total block, but as a temporary waiting period.

It’s a standard feature you’ll find in almost every UK life insurance policy. Insurers include it to prevent what they call ‘moral hazard’—which is a technical way of saying they need to guard against the risk of someone taking out a policy with the immediate intention of claiming on it. At its heart, the clause is there to make sure policies are bought in good faith, for genuine long-term family protection.

This initial period is the most critical part to understand. In the UK, it almost always lasts for 12 months from the day your policy begins. If the person insured dies by suicide during these first 12 months, the insurer won’t pay out the full cover amount.

But that doesn't mean the family gets nothing. In these tragic circumstances, UK insurers like Aviva and Legal & General will typically refund all the premiums paid up to that point. So, while it's not the outcome anyone wanted, your loved ones get back every penny you've invested.

How the Clause Works in Practice

Once you're past that initial 12-month mark, the suicide clause effectively expires. From then on, a death by suicide is generally covered just like any other cause of death. The insurer would be expected to pay out the full life insurance benefit to the beneficiaries.

The whole point of the clause is to remove any financial incentive for taking one's own life shortly after getting covered. After that one-year window, life insurers will typically pay out, as long as there wasn't any misrepresentation or failure to disclose important information on the original application. You can find more detail on how UK insurers approach this on iaminsured.co.uk.

It’s a crucial distinction. The clause is a balancing act—it allows the insurer to manage their risk while still fulfilling the ultimate goal of protecting a family’s financial future.

When the Clock Can Restart on Your Policy

Here’s a detail that many people miss: the 12-month clock on the suicide clause can sometimes restart. This won’t happen for small administrative changes, but it can be triggered if you make significant alterations to your policy.

The most common triggers that could restart the exclusion period include:

- Increasing Your Cover Amount: If you decide you need more protection and your insurer agrees to increase the sum assured, the 12-month clause may again, but usually only to the new, increased portion of your cover.

- Reinstating a Lapsed Policy: If you fall behind on payments and your policy lapses, getting it reinstated will often start a fresh 12-month suicide exclusion period for the entire policy.

Real-world example: Let’s say a parent takes out a £200,000 policy to protect their family. Two years later, they have another child and increase their cover to £300,000. The original £200,000 is well past the exclusion period. However, the new £100,000 of cover might be subject to a new 12-month waiting period.

It is absolutely vital to read the new terms or speak to your adviser whenever you make major changes to your life insurance. This is the only way to be sure you understand exactly how those adjustments affect your family's protection and avoid any devastating surprises down the line.

Why Honesty About Mental Health is Non-Negotiable

When you take out a life insurance policy, you’re making an agreement that’s built entirely on trust. Think of your application as the foundation of a house; if it has cracks or weaknesses from the start, the whole structure is at risk of crumbling. This is why being completely honest about your mental health history isn’t just good practice—it's absolutely essential for securing your family’s future.

At the heart of this is a legal principle known as the duty of disclosure. In simple terms, this means you’re required to give the insurer the full and honest picture of your health and lifestyle. Holding back details, even if you think they’re minor or happened a long time ago, can have devastating consequences.

If an insurer later finds out that information about your mental health was left out or wasn't accurate, they could declare the policy void due to non-disclosure. This means they could refuse to pay out a claim for any reason, not just suicide. The very protection you put in place for your loved ones could completely fall apart.

Understanding the Underwriting Process

Insurers need a clear view of your health to work out the risk fairly, and that includes your mental wellbeing just as much as your physical health. When you , you should expect to be asked some direct questions about your mental health history.

Common questions you might see include:

- Have you ever been diagnosed with a mental health condition like depression, anxiety, or bipolar disorder?

- Have you received any treatment, counselling, or medication for your mental health?

- Have you ever been admitted to hospital because of your mental wellbeing?

- Have you ever had suicidal thoughts or attempted suicide in the past?

Answering these questions truthfully is critical. Insurers are thorough, and if they find out something was hidden, it can lead to a claim being denied, regardless of how the person passed away. While the suicide clause deals with exclusions based on timing, your honesty on the application is the bedrock of whether your beneficiaries will actually receive a payout.

Does a Mental Health Condition Mean No Cover?

It’s a common myth that having a mental health condition automatically means you can't get life insurance. That’s simply not true. Millions of people in the UK with well-managed conditions like anxiety or depression successfully get life insurance every year.

The key is transparency. An insurer’s decision is based on the full context of your situation—your diagnosis, how stable your condition is, and the treatments you've had. Being upfront allows them to offer you a policy that truly reflects your circumstances.

In some cases, a history of mental health issues might mean you pay a bit more in premiums, or have specific exclusions, but it rarely leads to an outright "no." The absolute worst thing you can do is hide the information, because that jeopardises the very financial safety net you're trying to build. To learn more about how insurers view different health issues, have a look at our guide on getting life insurance with medical conditions.

Ultimately, being straight with the insurer on your application is the single most important step you can take. It ensures that when your family needs it most, the cover you’ve been paying for will actually be there for them, without any complications or disputes.

How Different UK Life Policies Handle Suicide Claims

It’s a common misconception that all life insurance policies are the same, but when it comes to suicide claims, the differences really matter. While the 12-month exclusion period is an industry standard, the finer details depend on the specific product you choose. Understanding these variations is the key to making sure your family has the right protection in place.

Take standard term life insurance, for instance. Whether it’s a level term policy designed to protect your family or a decreasing term plan to clear a mortgage, you can bet it will include the 12-month suicide clause. These policies are fully medically underwritten, which just means your health and lifestyle are thoroughly assessed at the start.

It's the same story for a Whole of Life policy. Because it’s designed to cover you for your entire life and serve as long-term financial planning, that initial exclusion period is a fundamental part of the contract, preventing immediate claims right after the policy begins.

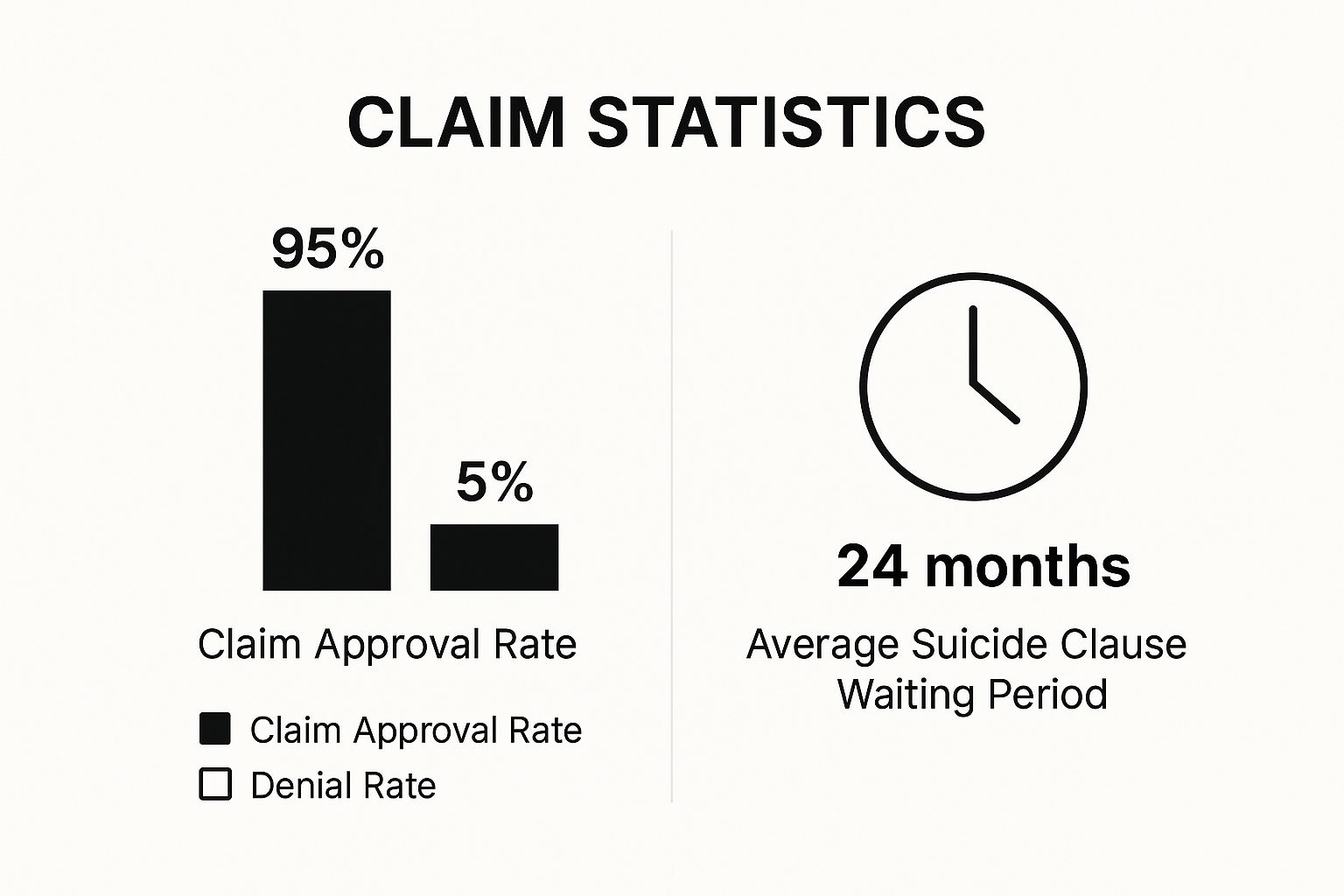

This data from the Association of British Insurers (ABI) underscores the reliability of life insurance. Although the suicide clause is standard practice, the overwhelming majority of claims are paid, giving families the support they need.

Over-50s Policies

Over-50s plans operate slightly differently. Their main selling point is competitive acceptance with no medical questions asked, which makes them an excellent option for many. But this accessibility comes with a different kind of waiting period.

Instead of a specific suicide clause, most over-50s plans have an initial waiting period of 12 or 24 months where they won't pay out for death by any cause, unless it's an accident. If the policyholder dies from natural causes or suicide during this window, the insurer refunds all the premiums paid, sometimes with a small amount of interest. Once you’re past that initial period, the policy pays out for any cause of death, suicide included.

Group Life Insurance Through an Employer

This is where things are often very different. Group life insurance, often included in workplace benefits as a ‘death in service’ scheme, is a valuable perk. One of the most significant differences is that many of these schemes do not have a suicide clause at all.

Why? Because the risk is spread across the entire company workforce, not just one individual. Insurers are often willing to waive the exclusion in this context. This means if an employee were to tragically die by suicide, their family would typically receive the payout without any waiting period. It's one of the most powerful benefits of life insurance that can come with a job.

Comparing Suicide Clause Terms by Policy Type

To make it easier to see how these policies stack up, here's a quick overview of how different UK life insurance products typically handle suicide claims.

| Policy Type | Typical Suicide Clause Period | Important Considerations |

|---|---|---|

| Term Life Insurance | 12 months | This applies to both level and decreasing term policies. The clause is standard due to full medical underwriting. |

| Whole of Life Insurance | 12 months | As a long-term financial planning tool, this waiting period is a core feature to prevent immediate claims. |

| Over-50s Policies | 12-24 months (for most causes of death) | This is a general waiting period, not just for suicide. Death by accident is usually covered from day one. |

| Group Life Insurance | Often None | Employer-provided schemes frequently waive the suicide clause, offering immediate cover for employees. |

As you can see, the type of policy you hold makes a huge difference.

Comparing these policies side-by-side shows exactly why reading the policy documents is so vital. Whether you're a homeowner with a mortgage, a parent planning for your children's future, or someone looking for a simple, competitive plan in later life, the answer to does life insurance pay for suicide really comes down to two things: the type of policy you have and how long it's been in force.

What to Expect During the Claims Investigation

For a family grieving a recent loss, the idea of a life insurance investigation can sound incredibly intrusive and overwhelming. However, understanding what the process actually involves can help ease some of that anxiety.

It’s not designed to be difficult or to cause distress. Think of it as a standard, necessary step the insurer must take to do its job properly and fulfil its obligations under FCA regulations. It's a formal procedure to make sure all the policy's terms have been met.

When a claim is filed after a suspected suicide, the insurer will need to gather a few key documents. This part of the process is handled as sensitively as possible, but it's essential for them to verify the details of the policy and the circumstances surrounding the death.

Key Documents Insurers Request

You can generally expect the insurer to request the following information:

- The Original Death Certificate: This is the official document that confirms the death.

- The Claimant’s Statement: A form the beneficiary will need to complete to provide details for the claim.

- A Coroner’s Report: If an inquest was held, this report provides the official findings on the cause of death.

- Medical Records: The insurer might request access to the deceased’s medical records from their GP. This is mainly to cross-reference the information given on the original application.

This collection of documents allows the insurer to build a complete picture. They need to confirm the death happened outside the initial exclusion period and double-check for any significant non-disclosure from when the policy was first taken out.

The primary goal of the investigation is simple: verification. Insurers need to ensure that the information provided on the application—particularly concerning mental and physical health—was accurate. It’s a standard check to uphold the integrity of the insurance agreement.

Why the Investigation Is Necessary

A thorough investigation is simply part of the framework of how UK life insurers manage risks, while still providing vital protection to families once the initial waiting period is over. They need to confirm the claim's validity and rule out any non-disclosure of critical information, like past mental health struggles or substance misuse issues. For a deeper dive on this, you can discover insights on how insurers handle suicide claims at iaminsured.co.uk.

Ultimately, this process ensures that genuine claims are paid correctly and without undue delay. While it might feel like a tough hurdle during a time of grief, it’s a structured and necessary part of confirming that the policy can and will pay out as intended, providing the financial support your loved one wanted for you.

Where to Find Support for Your Mental Health

This article touches on a very difficult subject. It's so important to remember that if you're struggling, help is always available. Reaching out is one of the bravest things you can do, whether for yourself or for someone you care about.

The UK has several incredible organisations that offer confidential, non-judgemental support. Your wellbeing is what matters most, and these free services are here to listen and help you find a way forward.

- Samaritans: You can talk to someone anytime, 24/7. Just call 116 123 for a confidential chat.

- Mind: A fantastic resource for advice and support. Their Infoline number is 0300 123 3393.

- CALM (Campaign Against Living Miserably): They run a helpline and webchat from 5pm to midnight every day. The number is 0800 58 58 58.

Alongside getting professional support, simple self-care practices can make a world of difference to your mental wellbeing. If you're feeling overwhelmed, you can find some practical and actionable steps for self-care for burnout in guides like this one.

Frequently Asked Questions

We've covered some difficult topics, so it's only natural if you still have questions. Here are some quick, straight-to-the-point answers to the questions we hear most often about life insurance and suicide in the UK.

What Happens if a Coroner's Verdict Is Open?

This is a common scenario. If a coroner cannot definitively determine the cause of death and records an 'open verdict', the insurer will conduct its own investigation. They'll look at all the available evidence and make a decision based on the 'balance of probabilities'.

If their investigation points to suicide within the policy's initial exclusion period (usually the first 12 months), they will likely decline the full claim. However, they will refund the premiums paid. Once that initial period has passed, an open verdict usually won't prevent a successful claim.

Are Premiums Refunded if a Claim Is Denied?

Yes, absolutely. If a life insurance claim is turned down because the death occurred during the suicide clause period, UK insurers will almost always refund 100% of the premiums that have been paid. This means the family gets that money back, even though the full policy payout isn't made.

Does a History of Depression Stop Me Getting Cover?

No, not at all. Having a history of depression or any other mental health condition does not automatically disqualify you from getting life insurance. Insurers will simply ask more detailed questions to get a clear picture of your situation—things like your diagnosis, treatment, and how stable your condition is now.

It might affect the price of your premiums, but in most cases, cover is definitely still available. For a broader look at the basics, you can read our complete guide on how life insurance works. And for specific insights on supporting young people, it's worth exploring resources on the crucial role of mentorship in teen mental health.

Ready to secure your family's future? At Discount Life Cover, our expert advisers can help you compare quotes from leading UK insurers to find the right policy for your needs and budget.

Get Your Free, No-Obligation Quote Today

This article is for information purposes only and does not constitute financial advice. Discount Life Cover is not providing personalised recommendations. Insurance policies vary depending on individual circumstances. For advice tailored to your situation, please speak with a qualified financial adviser or request a personalised quote.

Leave a Reply